Ever since the 1960s, the capital asset pricing model (CAPM) has been something like a bible for most investors…

It was an unquestionable “North Star” that tied everything in the belief system together.

And CAPM spent decades upholding its status as finance’s most sacrosanct law … before, of course, being completely disproven.

See, CAPM essentially says there is a positive linear relationship between a stock’s volatility and its expected future return.

The more volatile the stock … the higher its expected future return.

Many investors have taken this to mean: “If you want to earn a higher return, you should invest in stocks with higher volatility.”

Put simply: “You’ve got to risk it to get the biscuit.”

Of course, shareholders of countless failed risky investments haven’t a crumb to show for all the risk they took on.

Today, we’re going to look at the truth about volatility — starting with the “higher risk = higher return” fallacy.

On the Contrary…

Dozens of academic research studies demonstrate the market-beating premium investors can earn by investing in low-volatility — not high-volatility — stocks.

This directly contradicts CAPM. And the evidence for this stretches back more than 90 years, so it’s no fleeting anomaly.

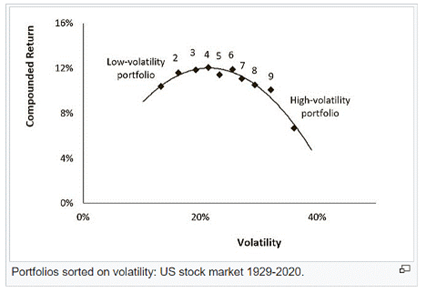

The chart below shows the compound return of low- and high-volatility portfolios from 1929 to 2020.

A Counterintuitive Relationship

The existence of this counterintuitive relationship between volatility and expected returns has a number of explanations…

For one, most investors have an aversion to using leverage — which is when you borrow money to invest in a position larger than the cash you have on hand.

In the absence of that aversion, it would be rational for an investor to build a portfolio of low-volatility stocks and then lever it up conservatively so that it matches the return of a higher-volatility portfolio.

But “leverage” is a dirty word to most folks. So, instead, investors who seek higher returns forego that option and simply invest in stocks with higher volatility.

This phenomenon dovetails with another behavioral bias: the “lottery ticket” effect.

Human nature urges us to seek “moonshot” returns in highly volatile stocks, even if the odds of earning such returns are minuscule and lower than we estimate.

This bias works toward unjustly inflating the prices and valuations of high-volatility stocks while leaving low-volatility stocks underpriced.

Taken together, investors show a preference for high-volatility stocks … even though low-volatility stocks have delivered superior returns for those who are wise enough to pursue them.

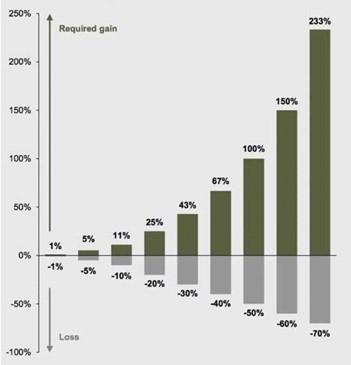

Lastly, there’s a significant hurdle that high-volatility stocks must overcome to a far greater degree than low-volatility stocks — the outsized rally a stock must mount after a drawdown to get back to breakeven.

Maybe you’ve seen this chart before…

Recovering From a Crash Isn’t Easy

As you can see, when downside volatility hits a highly volatile stock … it requires a herculean rally to get back to breakeven.

Low-volatility stocks tend to hold up better in down cycles, which sets them up for an easier road to recovery and, over time, allows for more efficient compounding of capital.

Longtime members of my Green Zone Fortunes newsletter know that my team and I consider a stock’s volatility before we recommend it. “Volatility” is one of the six factors on which my Green Zone Power Ratings model is built.

We don’t always seek stocks with the absolute lowest volatility, but we most certainly avoid stocks with the highest volatilities … because that’s where this factor is most effective at boosting overall returns.

In many market environments, it pays to take on some additional volatility. A stock that ranks in the middle of the pack on volatility may actually be worth the risk and outperform some of the lowest-volatility stocks in the market.

But what you most definitely want to do is avoid the top 10% of most volatile stocks.

Countless academic papers, as well as my own research and stock rating model, show that this is where you find the stocks that lag the market the most and even generate negative returns.

We’re likely to see elevated levels of volatility throughout 2025 linked to numerous breakout investments. So, now more than ever, it’s going to be crucial to stay focused on the best possible investments to meet your long-term goals.

To good profits,

Adam O’Dell, CMT

Chief Investment Strategist, Money & Markets