It’s no secret why most people buy closed-end funds (CEFs): big dividends!

The 500 or so CEFs out there yield a game-changing 7%, on average. And with CEFs coming from all corners of the economy, you can easily build a nice, diversified CEF portfolio paying enough dividend cash to let you retire on $500,000 (or less!).

CEF Investors an Emotional Group

But there is one thing you should know about the CEF market: Investors who buy CEFs are a bit twitchy, meaning they can sometimes oversell in a crisis. This is why there are still plenty of great CEF bargains out there.

The flipside is that these folks also have a tendency to pile into certain CEFs when markets climb, making some funds overbought, boasting high premiums to net asset value, or NAV (another way of saying their market prices far exceed the value of their portfolios).

Buying at a big premium is a recipe for steep losses, even if you’re buying a top-quality fund with strong management. That’s exactly the case with the three CEFs I want to talk to you about today.

Good Funds, Bad Timing

When I say these three funds are well-managed, I’m not kidding: two of them have some of the highest annualized returns of all CEFs; one was the highest-performing CEF of all time before the coronavirus crisis hit its portfolio. And even with the virus’s effect, that fund has racked up an 11% annualized return over the past decade.

But that aside, they are all overpriced, which slashes their odds of hitting those heights again in the near term. So go ahead and put them on your watch list now — but definitely not your buy list.

Overbought CEF No. 1: Wrong Time for This 8.5% Dividend

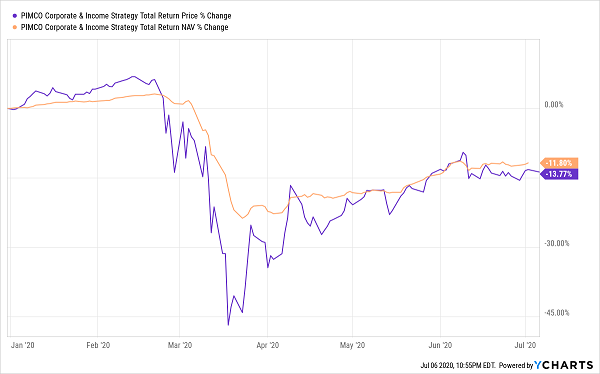

The PIMCO Corporate & Income Strategy Fund (NYSE: PCN) yields 8.5% and has returned an incredible 11% annualized, thanks to its portfolio of high-yield corporate bonds and complex debt derivatives. These are the kind of assets PIMCO is very good at managing (and most individual investors are, to be honest, pretty bad at managing on their own!).

A Lethargic Recovery for PCN’s Bonds

Unfortunately, junk bonds have been struggling to make a full recovery, as the coronavirus crisis forces several risky firms into bankruptcy. That’s why PCN’s portfolio is still down double-digits from the start of the year, even as the broader stock market has almost fully recovered.

This wouldn’t be so bad if investors were compensated for the risk, but they aren’t anymore.

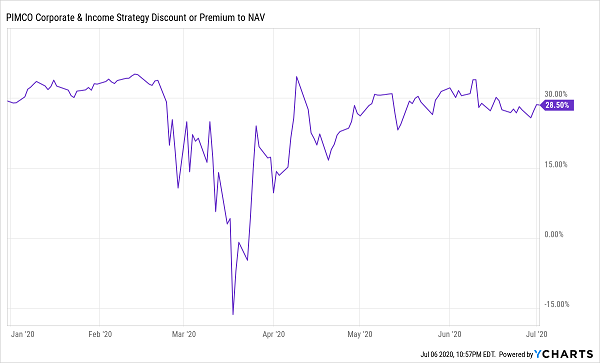

Premium to Discount … to Premium Again

PCN’s premium has come back with a vengeance, meaning it’s now as pricey as it was before the pandemic hit. That kind of pricing makes no sense given the increased risk involved with PCN’s assets.

Overbought CEF No. 2: A 9.9% Dividend … at a 30% Premium!?

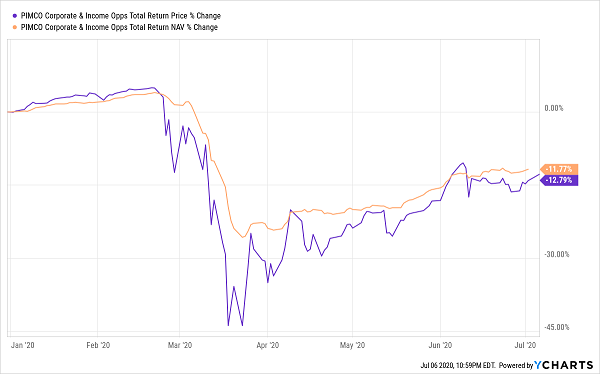

Our next fund, the 9.9%-paying PIMCO Corporate & Income Opportunity Fund (NYSE: PTY), is a close relative to PCN and has given investors a 10.6% annualized return over the last decade. At one time, PCN was the best long-term performer in the CEF universe. Unfortunately, the COVID-19 crisis and sell-off reversed that trend, depressing both its NAV and its market price.

Another Big Pandemic Loss

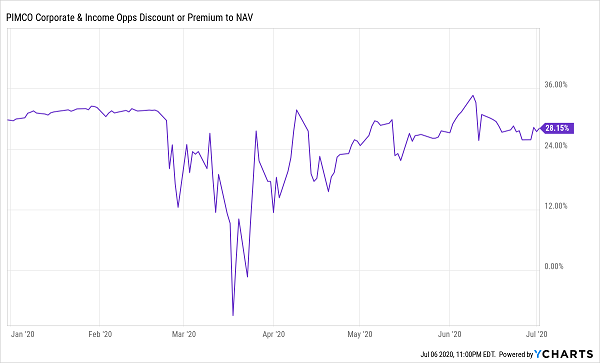

Considering PTY’s portfolio is very similar to that of PCN, this isn’t surprising. Nor is it surprising that PCN’s premium has returned in full, just like PTY’s has.

Another Pre-Pandemic Premium Returns

Will these funds’ discounts return soon? If we see another steep market sell-off, it’s likely — and that makes these funds great opportunities when they’re cheap, but not worth the risk when they’re overbought.

Overbought CEF No. 3: A Risky Fund in a (Normally) Safe Sector

The third fund I want to warn you about is the DNP Select Income Fund (NYSE: DNP), a utility-focused CEF with a 9.9% annualized return over the last decade. It’s another well-run fund with a strong management team and a 7.1% dividend (paid monthly), so it’s no surprise that it has a lot of fans — too many, in fact.

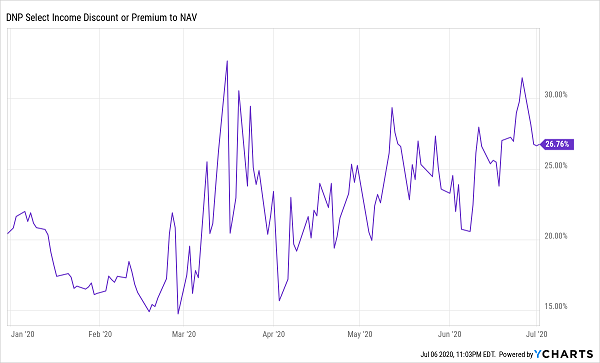

A Big Premium Gets Bigger

This chart is different from those of the two PIMCO funds; DNP’s premium dipped moderately during the February-March sell-off, only to spike, recede and rise again. This kind of erratic movement is particularly worrisome in light of the fund’s declining NAV and price return over the same period.

No Big Performance for the Premium

DNP’s portfolio has been hit not only by the pandemic but also by a general move away from utilities and into tech during the market’s recovery.

Sure, there’s a chance investors could swing back into utilities if there’s another pullback, but DNP’s massive premium still caps its upside, even if that were to happen. And if markets keep rising, a continued move into growth stocks could be especially harmful to DNP, given its high premium. Either way, the fund’s massive premium isn’t worth paying, no matter how well it has performed in the past.

To learn more about generating monthly dividends as high as 8%, click here.