In normal times, we contrarians are stuck combing the market’s backwaters — REITs, closed-end funds (CEFs) and the like — in our hunt for outsized dividends.

But, of course, these are not normal times.

This crisis has flipped the script. Now we can get the same big payouts but with much less work. In fact, we can get them from the same stocks you’ll find in any American’s portfolio. This is a once-in-a-generation opportunity, and it can’t last.

Fishing Close to Shore

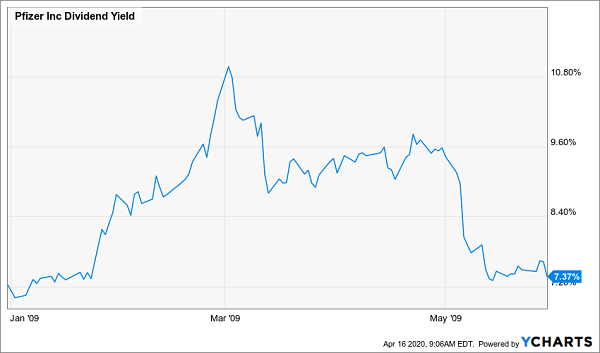

The last time I saw a situation like this was in March 2009, days before the S&P 500 bottomed in the financial crisis. Back then, the yield on sleepy dividend payer Pfizer (PFE) did something extraordinary: It nearly tripled almost overnight!

Normally the pharma giant’s payout meanders between a 3% and 4% yield:

Pfizer’s Tranquilized Dividend

But, for a short time in early March 2009, we could buy Pfizer and lock in an 11% income stream.

Pfizer Becomes a Dividend Legend

That unusually high yield stuck around, too. Even if you’d waited till late May, you’d have locked in a nice 7.4% payout, twice what Pfizer usually pays.

To be clear, this huge payout didn’t happen because Pfizer got generous with its cash — it resulted from a drop in the share price as the recession hit.

That brings me to this latest crisis, which has prompted other S&P 500 companies to “pull a Pfizer” and hand us payouts that were unthinkable just one month ago. And because these stocks have been overly beaten down, they give us a shot at price gains, too.

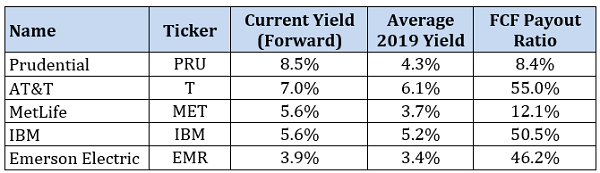

Five S&P 500 names stand out. Here they are, ranked by dividend yield. Below, we’ll take a deeper dive into each one.

5 Huge S&P 500 Dividends

‘Sudden’ High Yielder No. 1: Prudential

Prudential (PRU) has plunged 45% year-to-date, as of this writing, much further than the S&P 500:

PRU Gets Tossed Over the Side

This knee-jerk reaction literally broke the usual valuation measures. You can buy PRU today for a ridiculous 33% of book value, or what it would fetch if it were broken up and sold for parts.

That’s insulting for a 140-year-old firm whose name is synonymous with group and individual life insurance, both of which will bounce back post-crisis. Its wealth-management business is also a giant, administering $1.4 trillion of assets.

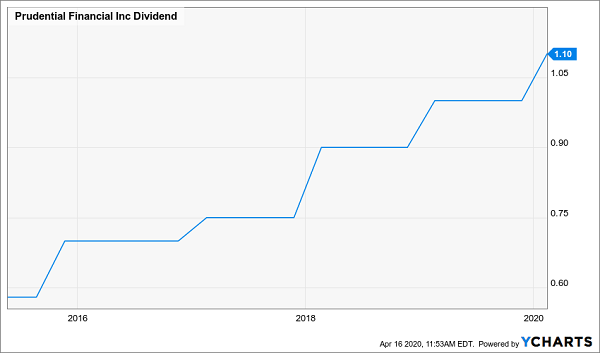

As you can see above, PRU’s yield has soared to 8.5%, and it boasts one of the lowest payout ratios I’ve seen, with just 8.4% of free cash flow (FCF) going to dividends. Management could boost the dividend five times today and still be under 50%.

No wonder this is one of the few 8.5% dividends that’s growing — and fast, having nearly doubled in the last five years:

A Rare 8.5% Dividend That Grows

This is another Pfizer-in-2009 situation. I don’t expect it to last.

‘Sudden’ High Yielder No. 2: AT&T

AT&T (T) doesn’t give you Prudential’s payout growth — in fact, I bemoaned its penny-a-year hikes just last month.

But if AT&T has been on your watch list, now is the best time to buy that we’ve seen in years. The stock has also been unfairly punished, falling behind the S&P 500 and Verizon Communications (VZ):

Investors Forget That AT&T Is Essential

The dividend accounts for 55% of AT&T’s last 12 months of FCF, a reasonable ratio for an essential-service provider, and that isn’t the only thing protecting the payout: The company ended the first quarter with $10 billion in cash, far more than the $3.7 billion it pays in quarterly dividends. Net debt was also a reasonable 27% of assets, and AT&T will bring in $2 billion from property sales later this year.

These moves should see AT&T through the crisis. On the other side, it will benefit from its 5G rollout and the work-from-home trend.

‘Sudden’ High Yielder No. 3: MetLife

MetLife (MET) is another insurer that’s been unduly punished this year, dropping 30% to trade at just 44% of book value.

Buying now also gets you a 5.6% yield, way up from the 3.6% average for all of 2019. The payout is also easily protected by MET’s low payout ratio, at just 12% of FCF. Its balance sheet also shines, with $20.5 billion of cash, more than its $16.9 billion of long-term debt.

If you’re looking to bolster your financial holdings while going beyond banks like JPMorgan Chase (JPM) and Bank of America (BAC), MetLife is worth a look.

‘Sudden’ High Yielder No. 4: IBM

One stock likely to raise its dividend this year is International Business Machines (IBM). The company has raised its dividend for 24 straight years, so it has one hike to go before becoming a Dividend Aristocrat.

IBM’s reasonable FCF payout ratio of 50.5% should help it over the line, as should its healthy balance sheet, with reasonable debt and $11.2 billion of cash on hand as of the end of the Q1, well above the $1.4 billion of dividends it paid in the quarter.

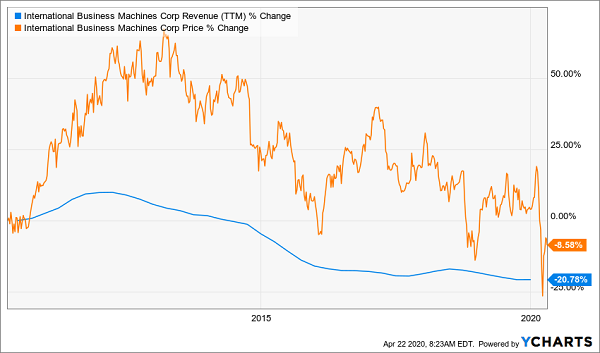

Unfortunately, IBM’s revenue has tracked the wrong way in the last decade, and that’s pulled the share price down with it:

IBM’s Frozen Sales

The company is making progress in some areas, like the cloud (sales up 23% in the first quarter). But it still lags in this market, well behind Amazon.com (AMZN) and Microsoft (MSFT).

Even so, if you want to bet on a comeback for Big Blue, you can buy this soon-to-be Aristocrat at a higher-than-average yield now.

‘Sudden’ High Yielder No. 5: Emerson Electric

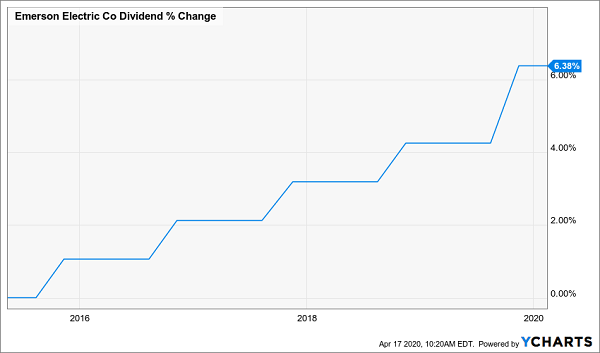

Emerson Electric (EMR) is a long-time Dividend Aristocrat. The 130-year-old firm, supplier of everything from valves to engineering services, raised payouts for 63 years running, though its yearly hikes have been a penny or less for most of the last decade.

Emerson’s Dividend: Management Could Do More

The hikes are also disappointing, with Emerson’s trailing 12-month revenue up more than 10% in that time, and free cash flow up 14%. Its balance sheet is also healthy, with long-term debt of $3.1 billion, or just 15% of assets.

In fairness, management is a big buyer of its own stock, having taken 8.5% of its shares off the market since 2015. And therein may lie the best reason for buying Emerson — its share price has been sliced 30% this year, far more than the market, setting it up for a nice bounce. Plus, you’ll get a 4% dividend, too.

To learn more about generating monthly dividends as high as 8%, click here.