The Prisoner’s Dilemma is a classic thought experiment about cooperation … and how acting in your own interests might actually make you worse off.

As it goes, two suspects in a crime are caught and separated. Each is offered a deal: Sell out your partner, and you walk free while the other guy takes the blame.

If they both stay silent, both are likely to get away with it. If one talks and the other remains loyal, the snitch walks away clean, and the loyal one takes the fall. But if they both betray each other, then they both get punished … which would be the worst possible outcome for all.

The catch is that they have to make the decision without knowing what the other one will do. And because trust isn’t exactly high between the two suspects (remember, they’re being interrogated for a crime!), the assumption is that the other guy is going to sing. So you sing first … guaranteeing the worst outcome for all.

This is the scenario that the AI hyperscalers find themselves in. Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), Meta (META) and OpenAI (the creator of ChatGPT) are locked in a wildly expensive AI arms race costing them hundreds of billions of dollars each. They are all plowing gargantuan sums of money into AI infrastructure because they can’t afford to let their rivals leapfrog them.

Larry Page, the co-founder of Google, reportedly said he’s willing to go bankrupt before losing the AI race, and Meta’s Mark Zuckerberg made a similar comment, saying he’d rather “misspend a couple of hundred billion dollars” than fall behind.

Breaking Down Monopolies

Technology stocks tend to rate exceptionally well on the Quality factor of Adam’s Green Zone Power Rating system. Adam wrote at length on this yesterday in What My System Said Today, but I can summarize it here. A major contributor to tech’s high quality is their capital efficiency. Their businesses are often extremely scalable and “capital light.” They require very little in new capital spending to grow.

Think about it. How much does it cost Microsoft to sell an additional Excel or Word license? Nothing, other than an infinitesimally small amount of electricity or server bandwidth.

On top of this, technology tends to create natural monopolies or oligopolies. Microsoft has largely owned the operating system and office productivity world for decades. Apple and Alphabet have a duopoly on the smartphone market. Oracle (ORCL) has very little competition in its particular corner of the Big Data market. And Amazon, Microsoft and Google have an effective triopoly on cloud computing.

With no real competition, all of these companies have been able to sustain ridiculously high profit margins and returns on equity.

The AI arms race shakes up this equilibrium. For the first time in years or even decades, the tech giants suddenly have competition.

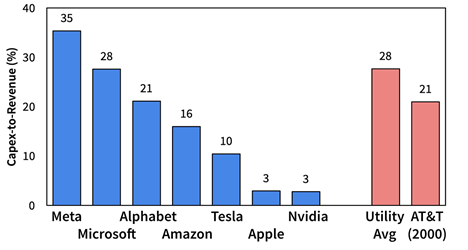

Take a look at the following chart, put together by Kai Wu of Sparkline Capital. This illustrates just how much these companies are plowing into AI infrastructure.

Meta is spending 35% of its revenues on capex, most of which is going to AI infrastructure. That’s more than what the typical utility company spends and significantly more than what AT&T (T) spent at the peak of the last tech infrastructure boom in 2000.

The implications here are interesting. The mega-cap tech stocks are transforming from high-quality, capital-light businesses to something that looks more like an asset-heavy utility company. But there’s a key difference here. Utility assets are made to last for decades. Capex spending on new Nvidia chips has a useful life of maybe a couple of years before it becomes old technology and essentially useless.

We’re going to see this affecting the Quality score of tech stocks in the years ahead. Higher depreciation charges on all of those infrastructure investments are going to lower profit margins, and we should expect to see some deterioration in capital efficiency.

Putting it bluntly, these companies simply aren’t going to be as attractive going forward.

That day might still be months or years away. As of today, all of the major AI hyperscalers have Quality scores in the 90s. They’re still some of the highest quality companies in the history of American capitalism.

But it’s also best to look beyond the big names, which is where this month’s Green Zone Fortunes recommendation comes in…

Later this week, Adam will send out his latest research to subscribers of his flagship investing service. This company designs and manufactures critical electrical solutions powering the next phase of the AI mega trend. And its customer rolodex includes many of the companies mentioned above.

And its strong rating in Adam’s system (including a 99 on Quality) means this stock is set to crush the market in the coming months.

Click here to see how you can join up in Green Zone Fortunes so that you’re one of the first to find out about this stock in the coming days.

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets