In today’s Marijuana Market Update, I answer a reader question about a stock I’ve covered in the past: Hexo Corp. (NYSE: HEXO). I let you know whether it’s a pick for your portfolio or whether you should pass on it.

About HEXO Corp. (NYSE: HEXO)

Recently, Akiem commented on our YouTube channel:

Mr. Clark, first, many thanks for the consistent market updates. I would be honored if you could do a breakdown of Hexo Corp. They’ve been gaining market share in Canada, have a beverage partnership with Molson Coors that gives them exposure to the states and I think their financials look at bit better than the ultra-big Canadian players. I like it as a mid-term play, but I believe the long-term gold is in U.S. MSOs. Wondering if I’m missing anything here? Many thanks! — Akiem

Thanks for your inquiry, Akiem. I’m honored that you would ask, and thanks for watching our videos.

HEXO Corp. produces and sells cannabis, primarily in Canada. Its products include:

- Dried cannabis under the “Time of Day” and “H2” lines.

- A cannabis oil mist product line called “Elixir.”

- Fine-milled cannabis powder.

- And cannabis beverages.

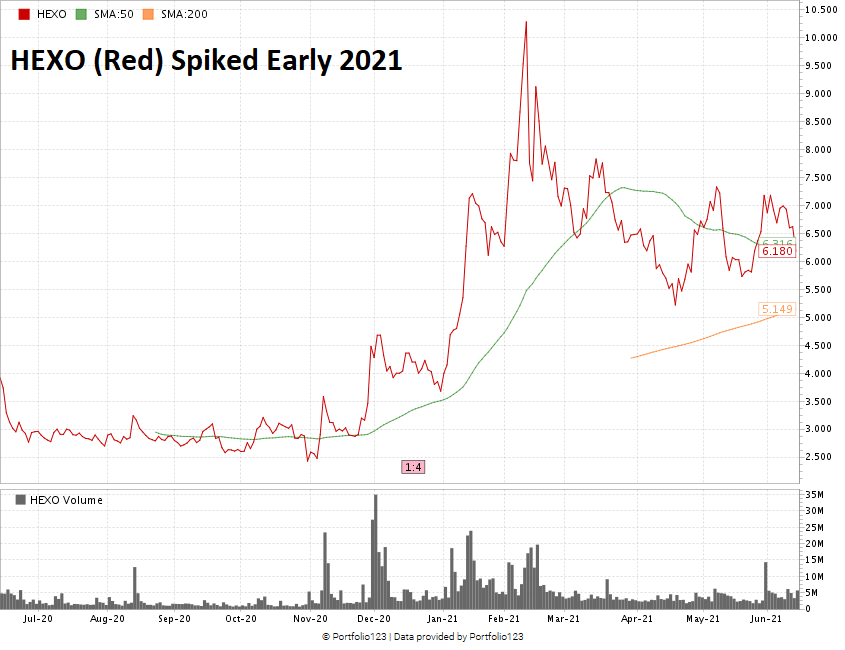

Akiem was right that Hexo Corp. stock looked strong at the beginning of the year.

Following a 1:4 stock split in December 2020, the company’s shares rocketed 179% from a low of $3.38 on January 1 to $10.28 in mid-February.

But the gains pared back, and the stock has since bounced between $5 and $7 per share.

That fluctuation is mostly due to continued uncertainty in the cannabis market.

The late-May boost coincided with HEXO’s announcing a $925 million cash deal for Redecan — one of Canada’s largest privately-owned licensed cannabis producers.

This is potentially a good deal for Hexo — albeit a little expensive — as it strengthens its footprint in Canada.

Additionally, the company is working to close a deal to acquire 48North Cannabis Corp.

Despite Deals, HEXO’s Earnings Are Poor

This week, HEXO released what I can only call a horrendous quarterly earnings report.

For the quarter ending April 30, 2021, HEXO’s total revenue was CA$22.6 million — a whopping 31% quarter-over-quarter drop.

In the previous quarter, Hexo reported positive earnings before interest, taxes, depreciation and amortization (EBITDA) of CA$200,000.

For the most recent quarter, its EBITDA was minus CA$10.7 million.

To put that in perspective, analysts expected HEXO’s EBITDA to be around CA$600,000 — so the actual figure is a massive gut-shot.

If you couple a miserable quarter along with the purchase of Zenabis — a deal that closed June 1 for $235 million — and the pending deals for Redecan and 48North, Hexo is spending a lot to gain market share in Canada.

With all of these deals and an at-the-market equity offering of $150 million, HEXO’s share count has gone from 122 million to 147 million in just six weeks.

The pending deals will add another 75 million.

And, yes, Akiem is also correct that HEXO has a deal with Molson Coors to give HEXO access to the U.S. market. However, HEXO has done little (if anything) to make any inroads here in the States.

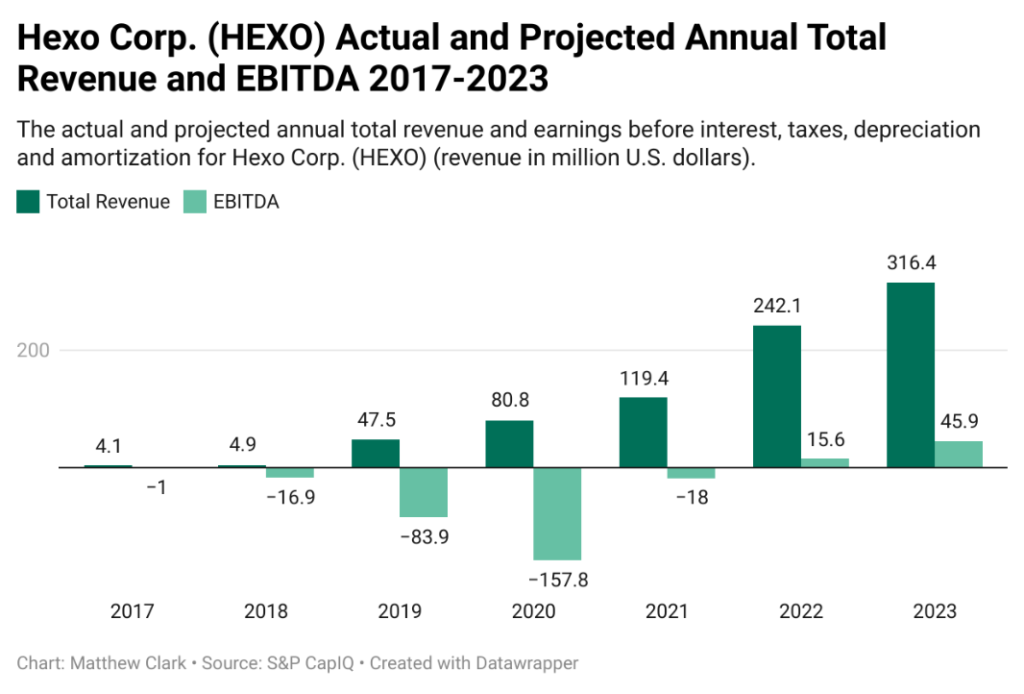

The total revenue picture for Hexo looks decent in the coming years. The company projects $316.4 million in total revenue by 2023.

That’s a 291% increase from 2020.

What concerns me is its growth in EBITDA — or lack thereof.

The company had massive losses in 2020 … in a time when fellow Canadian and American cannabis companies did well.

Projections are for the company to hit a positive EBITDA by 2022 — but only to the tune of $15.6 million.

Hexo could see $46 million in EBITDA by 2023, but if it continues to spend money in acquisitions, any gains realized for Hexo Corp. stock could be much farther down the road.

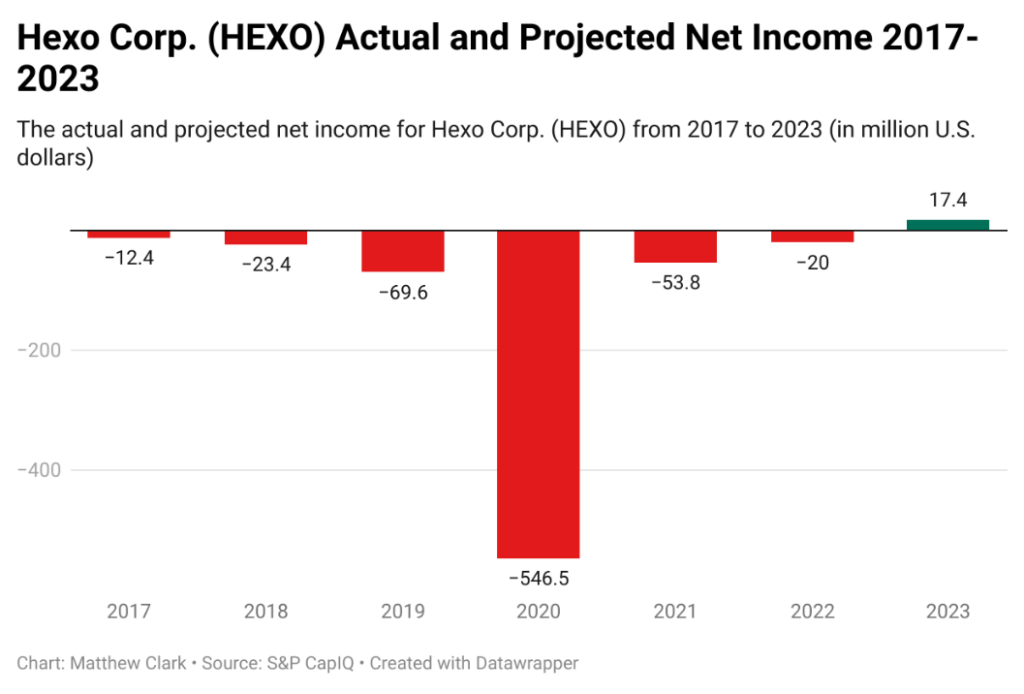

Its projected net income is also a flag for me.

Hexo is digging itself out of a pretty big hole from 2020 with minus-$546 million in net income.

Projections are that the company may not have positive net income until 2023, when it will be a paltry $17 million. That’s not promising. Even in the cannabis space, where you don’t expect a lot of positivity in terms of numbers, only gaining $17.4 million after a huge $546 million loss in net income is something to take a closer look at.

Another concern I have is that the company has not really exploited its toehold in the United States with its Molson Coors partnership.

The Takeaway for Hexo Corp. Stock

Overall, Hexo Corp. stock remains a pass for me.

The company is in a hole, and I’m concerned it isn’t making the best moves to get out of it.

Now, it could all change, but its lack of movement in the U.S. worries me, especially if legalization starts to pick up more steam. HEXO could get left behind.

And Akiem is right — the investment potential of American multi-state operators is much greater — especially if we see more movement on the legalization front.

Marijuana ETF Poll Results

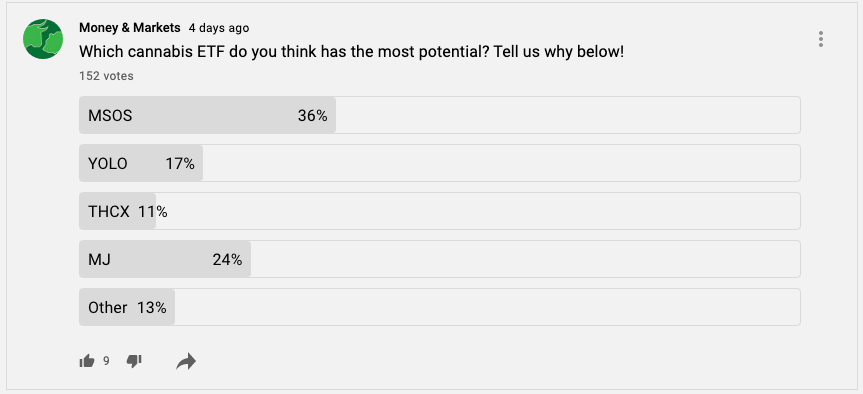

Last week, we asked you which cannabis ETF you think had the most potential.

Nearly 36% of you said MSOS was your ETF of choice. MJ was a close second with 24%, and YOLO was third at 17%. Some of the “Other” responses mentioned TOKE.

Thank you all for your responses. We’ll try to add polls on our community section weekly, so check back for more. Now I am looking at a few cannabis-related ETFs to add to our Cannabis Watchlist.

If you want to keep track of our Cannabis Watchlist progress (we’re up double digits, by the way) and know as soon as I add a company to the list, I encourage you to join our membership program on YouTube. Speaking of which…

New YouTube “Join” Feature

We offer members new exclusive content, including:

- Interviews with cannabis insiders.

- Blog posts, stock analysis and company breakdowns.

- More about our Cannabis Watchlist.

- Monthly live chats with me, where we’ll discuss cannabis stocks, the cannabis sector and much more.

Just click “Join” on our YouTube page to find out what you can access.

If you have a cannabis stock you’d like me to look at, email me at feedback@moneyandmarkets.com.

Where to Find Us

Coming up this week, we’ll have more on The Bull & The Bear podcast and our Money & Markets Week Ahead, so stay tuned.

Don’t forget to check out our Ask Adam Anything video series, where we ask your questions to Chief Investment Strategist Adam O’Dell.

Green Zone Fortunes co-editor Charles Sizemore also has a weekly series called Investing With Charles, where he breaks down dividend investing each week.

Remember, you can email my team and me at feedback@moneyandmarkets.com — or leave a comment on YouTube. We love to hear from you!

Safe trading,

Matt Clark

Research Analyst, Money & Markets

Matt Clark is the research analyst for Money & Markets. He’s the host of our podcast, The Bull & The Bear, as well as the Marijuana Market Update. Before joining the team, he spent 25 years as an investigative journalist and editor — covering everything from politics to business.