The coronavirus outbreak has created a lot of economic uncertainty in the U.S. and around the world, but a recent Gallup poll shows the pandemic isn’t drastically changing anyone’s retirement plans yet.

Gallup’s annual Economy and Personal Finance survey, which was conducted April 1-14, is a good gauge of sentiment for both retirees and those preparing to retire alike.

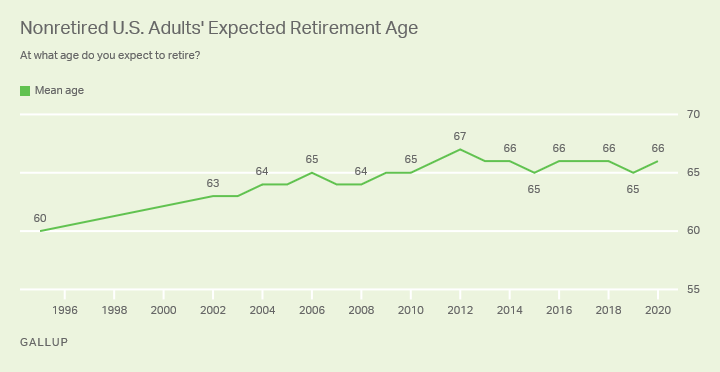

Focusing on the former group, one number to take into consideration is when people plan to retire. The average expected retirement age was 66 in this year’s iteration of the survey, and while that’s a slight jump from 2019’s expected age of 65, the number has floated between 65 and 67 over the last decade.

It seems like retiring later has become the new norm, though, and that will likely continue to trend up as Social Security’s full retirement age (FRA) continues to climb and people generally live longer. The full retirement age for 2020 is 66 and 8 months, and the FRA will cap at 67 in 2022.

Your FRA is important because it determines what age you are eligible for your full Social Security benefits. Claiming as early as 62 (the lowest age of eligibility) will cut your benefits permanently by up to 30%.

Staying on the topic of Social Security, the most recent Gallup poll shows that 36% of respondents plan to rely on Social Security as a major source of income in retirement, which is 3% higher than last year’s results. Expanding on that a bit, 88% say benefits will be a major or minor source of income in retirement, a 5% increase from 2019’s numbers.

What’s problematic about this is Social Security is only meant to replace about 40% of your income after leaving the workforce, so having a retirement plan that relies heavily on Social Security is not likely to work in your favor.

It also looks like more people preparing for retirement are prepared to jump back into the workforce. An impressive 70% expected to be supplementing their retirement income through part-time work, a 6% increase from last year.

While you may think working in retirement defeats the purpose, earning a little extra cash through a part-time gig isn’t just a financial boost. It can be great for keeping your mind sharp and fostering social connections that may be lost after leaving the workforce.

Retirement plans seem mostly intact, though that could change depending on how the economy recovers from the COVID-19 lockdown that is still in effect for much of the U.S.

What Should You Do About Your Retirement Plan Amid COVID-19?

While the most recent Gallup poll doesn’t reflect a huge change in retirement sentiment, you may still be worried about your future and wondering if you should change anything up.

The simple fact is, there are still a ton of uncertainties surrounding the economy and financial markets right now, and that means changing anything about your retirement strategy becomes a tough prospect.

Money & Markets contributor and retirement specialist Charles Sizemore recently laid out a post-coronavirus retirement plan that gives you some different aspects of saving for you to consider.

It’s tough to predict what any of this economic recovery from COVID-19 is going to look like, but thinking about and tailoring your retirement plan to work for you during this crisis can make a world of difference years down the line.