Editor’s note: LIVE on Thursday, Adam O’Dell will reveal a simple two-day trade that we believe is the fastest way to grow a trading account ever devised. In the six months we’ve been testing it internally, it’s produced gains five times larger than Warren Buffett’s best year as an investor. To reserve a VIP spot to this ground-breaking live event, click here.

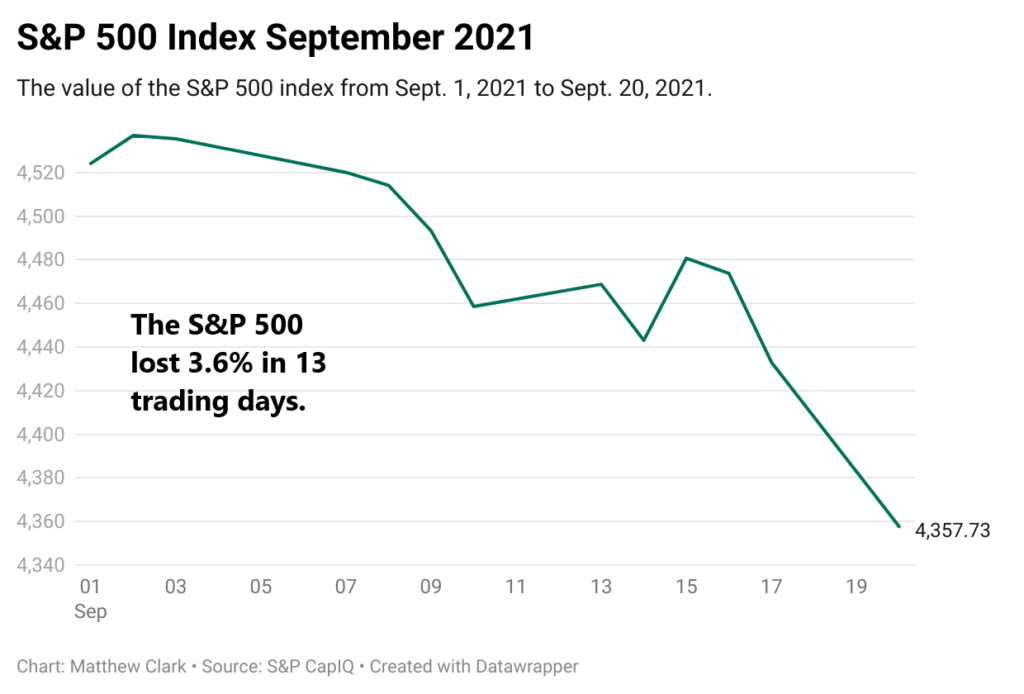

September has been nasty.

Out of the 13 trading days so far, the S&P 500 has finished lower in 10 of them. Monday’s market rout saw the index lose 1.7%.

The total peak-to-trough damage hasn’t been devastating, or at least not yet. But it’s been a rough market to trade. Nothing seems to work.

So, after a market rout like Monday’s, it’s good to take a step back and look at what we can do as investors when the market just flat-out isn’t playing ball.

After a Market Rout: Separate the Wheat from the Chaff

I personally separate my portfolio into what I consider “core” positions and what I consider more speculative positions.

A month like September isn’t going to affect my core portfolio. These are positions that I intend to hold for years … possibly forever. A lousy month, or even a full-blown bear market, isn’t going to change that.

But I have plenty of other positions that I’m far less committed to holding. They’re shorter-term trades or, if I’m to be completely honest, sometimes outright gambles.

I hate taking losses, but it’s important to be willing to take them on these non-core positions. Cutting your losses early preserves the capital you’ll need to buy the dip later. So, if you have a low-conviction trade working against you right now, don’t get stubborn and cling to it. Follow your risk management and get out.

Don’t Hurry to Buy the Dip

I recommend patience here. If you had limit orders placed previously to buy at current prices, then by all means, stick to your plan. You liked that price before, and nothing about the current sell-off should change that. But don’t get greedy at the first sign of a dip and rush to change your plans.

The average market correction sees a dip of nearly 14%. The recovery takes an average of about four months. This little sell-off we’re experiencing might be far less bad than that … or it could be much worse. We won’t know until it’s over. But if you’re looking for real deals, it’s still a bit early to bargain hunt.

Investment Returns are Only One Part of Your Retirement Plan

It’s fun to make money in the stock market. But in a really good year, your returns might be 20%.

But think about the employer matching on your 401(k) plan. If your employer offers a dollar-for-dollar match, your returns are an instant 100% … and that’s before you risk a nickel.

The same goes for the tax break. Let’s say you’re in the 32% tax bracket. On every dollar you invest in your 401(k) plan, you just make a 32% “return” on the tax break. And that’s true even if you put the entire amount in T-bills or money market funds.

So, even if you’re wary of putting new money into stocks during a market rout, you should still do everything in your power to make sure you’re maxing your retirement plans. The matching and tax breaks alone will almost always make it worthwhile, even if you decide to keep the contribution in cash rather than put it at risk in the market.

To safe profits,

Charles Sizemore

Co-Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.