As I wrote yesterday, technology shares have been rallying hard over the past few weeks, due in part to the belief that Santa might be delivering a more accommodative Federal Reserve this year for all the good little boys and girls on Wall Street.

We’ll know more after Chairman Jerome Powell delivers his remarks tomorrow. But in the meantime, let’s do a deeper dive into the tech sector.

There’s a lot happening in tech right now.

For the past three years, the bullish AI theme centered around the one-two punch of chipmaker Nvidia (NVDA) and ChatGPT creator OpenAI. These two companies together formed the engine driving the entire AI economy.

Well, that’s changing…

The AI mega trend’s center of gravity is shifting to Google parent Alphabet (GOOGL). Google’s recent version of its Gemini AI compares favorably to ChatGPT in terms of performance and general user satisfaction. And unlike OpenAI – which loses money and hemorrhages cash – Alphabet is wildly profitable and has almost unlimited resources.

Alphabet – along with Amazon (AMZN) – is also crowding Nvidia’s territory by making chips for AI datacenters. Nvidia’s chips are still generally considered to be the crème de la crème. But for the first time, they’re looking at real competition from cheaper and more energy-efficient chips designed especially for AI-related tasks.

All of this is good, in the “greater good” sense.

That’s how competitive capitalism is supposed to work. Competition drives down costs and improves quality for all of it.

But…

It also raises new questions for investors.

Does the current valuation of tech shares make sense in a world where their fat profit margins are all but certain to get chipped away by competition?

Let’s dig deeper into the sector to answer that question.

Tech is a Stock Picker’s Market

I’ll start with one objective fact.

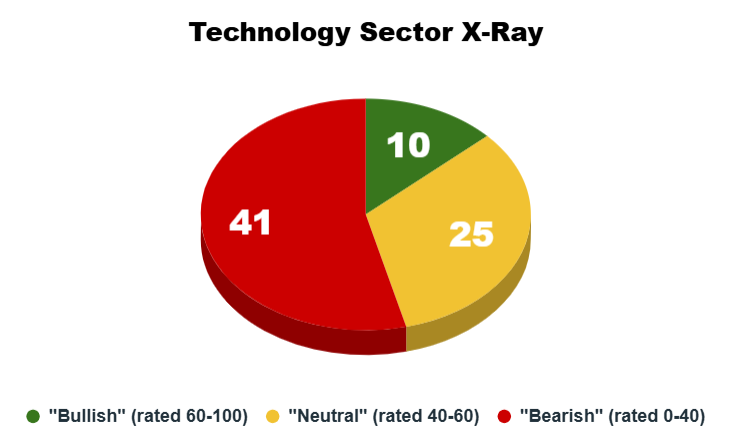

The tech sector as a whole does not rate well today on my Green Zone Power Ratings system. Of the 76 stocks in the sector, only 10 rate as “Bullish.” At 41, well over half rate as “Bearish” and another 25 rate as “Neutral.”

So, while the sector broadly may be leading the market higher, my system is telling us to be careful. This is not a time for blanket exposure to tech.

Let’s dig deeper into the ratings system to see where tech stocks are generally gaining and losing points.

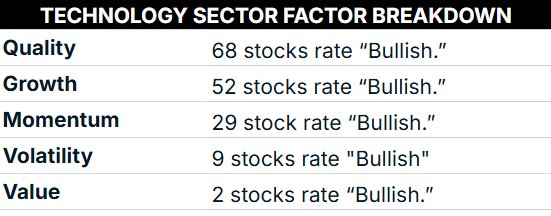

As we’ve covered before, tech stocks tend to have exceptionally strong quality factor ratings. Fully 68 out of the 76 rate as “Bullish” on quality, meaning they score a 60 or higher on their quality factor.

Technology, and particularly software and information companies, tend to have “asset-light” businesses. Software can be replicated infinitely many times at a marginal cost of effectively zero. It’s a fantastic business model once a company reaches that necessary critical mass of sales.

The technology sector also tends to rate well on growth. 52 stocks in the sector rate as “Bullish” on their growth factor.

But it’s also immediately clear where tech stocks tend to lose points. They’re volatile and, after years of outsized performance, really expensive. Only nine tech stocks rate as “Bullish” on their volatility factor, and a pitiful two rate as “Bullish” on their value factor.

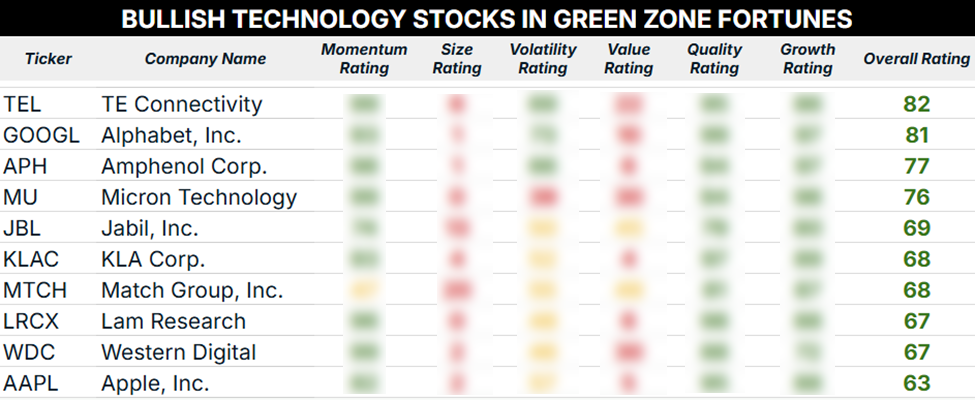

Let’s take a deeper look at those 10 tech stocks that rate as “Bullish” overall.

The Bullish 10

I teased a moment ago that the center of gravity in the AI race had shifted to Alphabet. So, it should really be no surprise to see the stock pop up near the top of the list with a “Strong Bullish” overall rating.

Unlike most of the rest of the sector, which tends to rate poorly on volatility, GOOGL rates a “Bullish” 73 on its volatility factor. This is a stock with market-crushing momentum, quality and growth that, at least based on its long history, is unlikely to give you whiplash.

Of course, you pay for the privilege. GOOGL is an expensive stock and rates a 10 on its value factor.

It’s interesting that fellow Mag 7 member Apple (AAPL) makes the cut, too. Apple has been considered something of a disappointment in AI, given the company’s lack of major breakthroughs and its far more modest investment budget.

Well, as the landscape begins to shift, Apple’s lack of investment may actually be a positive. Wall Street is starting to turn a skeptical eye to the gargantuan sums of money that “hyperscalers” like Meta Platforms (META) are pouring into AI infrastructure. Investors are demanding more accountability, and Apple’s more measured approach may explain why the shares are up 40% since June.

To good profits,

Adam O’Dell

Editor, What My System Says Today