For the past two years, corporate America had basically stopped talking about oil.

Earnings call after earnings call, executives were focused on AI, margins, consumer spending — the usual.

Oil was barely an afterthought.

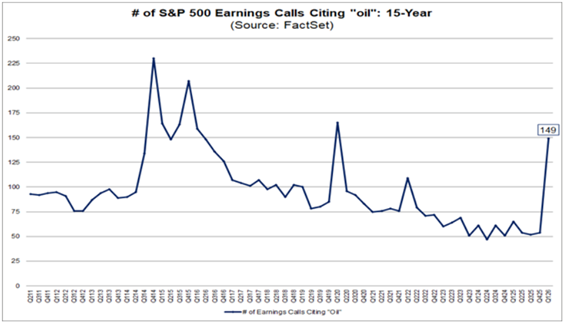

Mentions of oil on S&P 500 Index calls had quietly drifted toward 15-year lows.

Then, first-quarter 2026 changed everything.

Suddenly, 149 companies brought oil up on their earnings calls — nearly triple the count from just a quarter earlier and the highest reading since the pandemic.

That’s not noise. That’s a signal.

The last two times we saw spikes like this, investors who weren’t paying attention got burned.

The 2014 to 2015 surge came right as crude oil was collapsing from $100 a barrel, and it gutted energy sector earnings for two consecutive years.

The 2020 spike speaks for itself.

Now, here we are again, with oil back in the room.

It doesn’t mean a crash is coming. But when companies across the S&P 500 start mentioning oil again — airlines, manufacturers, retailers, chemicals — it means cost structures are becoming more complex.

It means hedges are being revisited.

As a result, the easy operating environment that corporate America has been quietly enjoying is starting to feel a little less easy.

Now, I want to revisit an earnings call I made last week…

ORCL Beats Earnings Estimates

Of the three companies that made our “bullish” list last week, I pulled out and suggested the possibility that the one we’re discussing today could beat estimates.

Oracle Corp. (ORCL) was projected to report earnings per share (EPS) of $1.27 for the quarter.

Here’s what I said about why I thought Oracle was a great candidate for an earnings beat:

Demand for graphics processing unit (GPU) capacity and AI training infrastructure has given Oracle visibility into its backlog that most enterprise software companies can only dream about right now.

What makes a beat plausible isn’t just momentum — it’s the setup. Analyst estimates for Oracle have historically lagged the actual cloud inflection, partly because the old “database company” label still anchors expectations lower than the business warrants.

When a company is structurally repricing faster than the models account for, estimates tend to be conservative by default. Add in the fact that Oracle has beaten EPS estimates in each of its last several quarters, and you have a name where the bar may simply be set too low — again.

Sure enough, that’s exactly what happened.

Oracle reported EPS of $2.03 on revenue of $19.18 billion for the quarter. That’s a 21% year-over-year jump in revenue.

Net income also rose, and the company maintained its forward revenue guidance for the rest of its fiscal year.

Now, the stock actually dropped after the earnings report, but that was more because the company also announced plans to raise more money to finance its AI buildout.

That’s not necessarily a bad thing… it just means the company plans to sell more shares and incur more debt, with the hope that it will pay dividends as AI continues to expand.

Overall, still a strong beat for Oracle.

Now, let’s shift gears to companies projected to have “bullish” earnings next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their EPS from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are two companies that made this week’s list:

Everyone wants to build AI. But almost nobody knows how.

That’s Accenture PLC’s (ACN) business right now, and it’s very, very good.

The EPS estimate of $3.72 is already a big leap from last quarter’s $2.93 — a 27% jump. And yet there’s a reasonable case that it still undersells what’s coming.

Here’s why: Accenture has quietly become the tollbooth on enterprise AI adoption. Fortune 500 companies aren’t building their own AI infrastructure from scratch — they’re paying Accenture to do it for them.

The firm has been funneling billions into AI-related services, and that pipeline keeps growing. In the company’s last report, it cited more than $3 billion in AI bookings for the fiscal year.

That number has likely only grown.

There’s also a macro tailwind hiding in plain sight.

When companies get nervous about costs — and given what we just said about oil, a lot of them are — they don’t stop spending on efficiency. They accelerate it.

Accenture sells efficiency. Cost-cutting environments are actually good for their business.

The risk? Consulting is discretionary, and if corporate clients start freezing budgets, Accenture feels it fast. That’s the bear case.

But with AI mandates coming from the C-suite at almost every major company, the odds favor ACN surprising to the upside here.

Our screen came up with no potentially “bearish” earnings for next week, so that’s all from me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets