Something unusual has been happening quietly taking place Easter. analysts have actually been raising their earnings estimates.

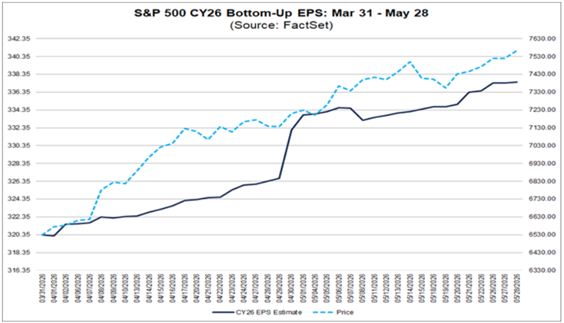

In a world where the default move is to cut and run — with tariff headlines and macro uncertainty giving every strategist cover to slash their numbers — the S&P 500 Index’s bottom-up earnings per share (EPS) forecast for 2026 has instead ground higher for two straight months, from $320 to nearly $338.

That’s not a rounding error. It’s a signal.

The market noticed, and then some.

While estimates climbed a respectable 5%, the index itself tacked on closer to 15% over the same stretch, lapping the analysts, pricing in optimism that the numbers haven’t yet fully justified.

That gap between what earnings are doing and what stocks are doing is the story right now.

It could mean investors see something the models don’t. It could mean corporate America is about to deliver a genuine upside surprise.

Or it could mean someone’s going to have some explaining to do come third-quarter 2026. It’s worth figuring out which.

So, using a special screener, I’ve broken down next week’s earnings into potentially “bullish” and “bearish” categories.

“Bullish” Earnings to Watch

These stocks are expected to beat their EPS from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are three companies that made this week’s list:

The name that jumps off the page is Oracle Corp. (ORCL).

On the surface, a move from $0.68 to $1.27 looks like a straightforward sequential improvement — nearly doubling earnings in a single quarter. But the more interesting question is whether even $1.27 is leaving money on the table.

Oracle has been quietly becoming one of the most important infrastructure plays in the AI buildout, and the market has been slow to fully price that in.

Its cloud infrastructure business — OCI — has been the engine here, consistently outgrowing rivals and signing hyperscaler-level contracts with customers who don’t renegotiate.

Demand for graphics processing unit (GPU) capacity and AI training infrastructure has given Oracle visibility into its backlog that most enterprise software companies can only dream about right now.

What makes a beat plausible isn’t just momentum — it’s the setup. Analyst estimates for Oracle have historically lagged the actual cloud inflection, partly because the old “database company” label still anchors expectations lower than the business warrants.

When a company is structurally repricing faster than the models account for, estimates tend to be conservative by default. Add in the fact that Oracle has beaten EPS estimates in each of its last several quarters, and you have a name where the bar may simply be set too low — again.

If cloud revenue comes in ahead of consensus next week, don’t be surprised if the earnings follow.

If nothing else, an earnings raise or beat will certainly help Oracle’s “bearish” rating on Adam’s Green Zone Power Ratings system.

Now, let’s shift gears to those “bearish” earnings next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are two companies that passed this screen:

The name worth watching here is Academy Sports & Outdoors Inc. (ASO).

A drop from $1.98 to an estimated $0.91 is already a brutal cut — expectations have essentially been halved. But the setup suggests even that lowered bar could be at risk.

Academy operates squarely in the crosshairs of the current consumer environment. Sporting goods and outdoor retail are a discretionary category, and it is exactly there that spending has been softening.

The consumer who was buying hunting gear, camping equipment and athletic apparel with post-pandemic enthusiasm has gotten more selective — and more price-sensitive. When budgets tighten, the $200 cooler and the new trail runners are the first things to go back on the shelf.

The tariff overhang makes it worse. A meaningful portion of Academy’s inventory — footwear, apparel, equipment — runs through supply chains with significant exposure to import costs.

Even if the company has been working to diversify sourcing, margin pressure doesn’t disappear overnight, and it often shows up in earnings before it does in guidance.

What makes a miss particularly plausible isn’t just macro headwinds — it’s that estimates may still be catching up to reality rather than getting ahead of it.

When a stock’s earnings trajectory looks like this, the analyst community is often in the middle of a downward revision cycle, not at the end of one. The $0.91 estimate might reflect where things were a month ago more than where they are today.

Missing or dropping EPS puts Academy’s “bullish” rating on Adam’s system in jeopardy.

And sometimes, the most dangerous number in earnings season isn’t the one that looks impossible — it’s the one that already looks bad and still isn’t low enough.

No matter what, it will be another interesting week of earnings.

That’s it for me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets