Welcome from the frigid, grassy plains of Kansas, as I spend a week with my grandson before returning to the sun of South Florida.

Today, I want to unpack a topic you hear about a lot in financial media, but that many investors don’t fully understand: hyperscalers.

A hyperscaler is a massive provider of cloud, networking and internet services.

Prime examples include Microsoft Azure, Google Cloud and Amazon Web Services.

What makes them hyperscalers is their ability to rapidly scale infrastructure to support millions of users.

Part of that scaling includes building and operating massive data centers – typically with more than 5,000 servers that provide Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

The tools they provide include artificial intelligence (AI) and machine learning, storage, security and analytics.

Since the public release of AI in 2022, these hyperscalers have become the backbone of the modern digital economy by providing the necessary infrastructure for Big Data, AI development and Internet of Things platforms.

Since that year, these hyperscalers have begun pouring millions into this infrastructure.

The actual amount will shock you.

Let me explain…

Spending Money Hand Over Fist

When ChatGPT was launched to the public in 2022, AI was the thing of science fiction movies.

Don’t get me wrong, AI was real before 2022… It just wasn’t available to the general public.

But since then, demand for AI capability has skyrocketed.

What was once reserved for large tech companies is now available to everyday people.

That comes with a significant increase in demand for the services hyperscalers provide.

Look at it from this perspective:

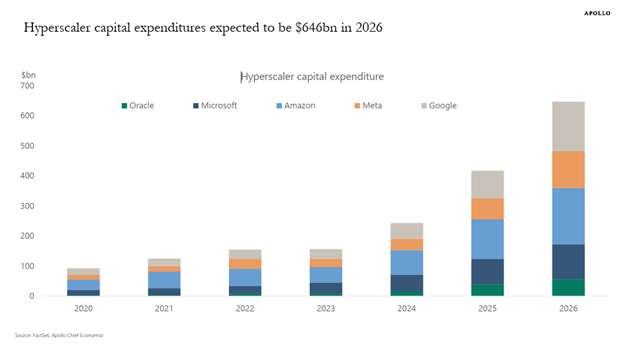

In 2022, the big five hyperscalers (Oracle, Microsoft, Amazon, Meta and Google’s parent company Alphabet) spent less than $200 billion on capital expenditures to build data centers and infrastructure.

By the end of this year, that amount is expected to reach near $650 billion — a 225% increase in four years.

Let me put that in perspective:

- $650 billion is roughly equivalent to the size of Singapore’s, Sweden’s and Argentina’s gross domestic products.

- Defense spending in 2026 is expected to reach $917 billion.

- Hyperscaler capex exceeds the combined military spending of Germany, France, the United Kingdom, Japan, Italy and Canada.

- Hyperscaler capex is nearly the same size as the market cap of stock markets in Belgium, Denmark and Indonesia.

In other words, $650 billion in hyperscaler capex this year is massive.

Keep in mind that $650 billion is spread only among the five largest hyperscalers in the U.S. It does not include smaller companies spending money to develop products for data center infrastructure.

That brings up a logical question relative to this massive spending increase…

Why Are Hyperscalers Backing Up A Brink’s Truck?

There are many possible answers to that question.

The first, obvious answer is competition.

Companies believe that if they don’t invest aggressively to secure a foothold in AI, they will lose their competitive edge.

Secondarily, there is an intense competition to develop the most advanced AI models and infrastructure.

However, the increased demand for AI has put pressure on hyperscalers to build massive, new or upgraded “gigawatt-scale” data centers, which are 20 to 100 times larger than regular data centers.

Hyperscalers are investing the majority of their capex in short-lived, high-cost assets such as graphics processing units and custom silicon.

But that’s not all they’re splurging on…

Spending capex on these assets also requires increased spending on high-speed, sophisticated networking equipment to connect thousands of these chips.

There is a significant risk to spending this kind of money.

By allocating hundreds of billions of dollars on capex, these hyperscalers risk straining short-term free cash flow – a company’s ability to pay operating expenses, meet debt obligations and fund short-term growth without relying on external financing.

So, these hyperscalers are betting that these investments will lead to exponentially higher future revenue… but that’s a big risk.

From an investing perspective, all you see right now is significant expenditures without immediate return on that investment.

These companies are spending billions with the hope that those expenses will be recouped (and then some) in the future.

Hyperscalers are looking at this investment from one perspective:

- “Hope is a good thing, maybe the best of things, and no good thing ever dies,” from one of my favorite movies, The Shawshank Redemption.

But many investors are still on the fence.

That’s all from me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets