I have to admit, we’re spoiled. In the past year or so, we realized just how much we enjoy low interest rates.

After all, low rates made it possible to buy larger homes. And we got to splurge on cars and other big-ticket items.

But we weren’t the only ones taking advantage of 5,000-year lows in interest rates.

Companies issued low-cost debt to expand … private equity firms relied on cheap money to fund acquisitions … and venture capital firms funded countless startups, many of which weren’t viable at higher rates.

Investing During a Time of Cheap Money

As investors, we benefited from publicly traded companies using low-cost debt to fund share buybacks.

With higher rates, buyback activity in the first quarter fell more than 21% compared to the same quarter a year ago (see the most recent data here).

The 20 largest companies account for almost half of the buybacks. These companies have solid balance sheets and access to the lowest available interest rates.

Buybacks increase the value of stocks. That’s because they increase earnings per share (EPS) by reducing the value of the denominator in that calculation. The effect has been small. But with fewer buybacks, many companies are struggling to report higher EPS.

Cheap money also allowed companies to invest heavily. To determine whether an investment makes sense, companies compare the expected returns of the project to their cost of financing. If a company expects to earn 4% a year on an expansion, it makes sense to do that if financing costs are less than 4% a year.

Low rates made many projects attractive. Former Federal Reserve Chair Ben Bernanke explained how far this process could go:

…If the real interest rate were expected to be negative indefinitely, almost any investment is profitable. For example, at a negative (or even zero) interest rate, it would pay to level the Rocky Mountains to save even the small amount of fuel expended by trains and cars that currently must climb steep grades.

With rates rising, fewer projects will be funded. That can also reduce earnings growth in the long run.

Of course, concerns about higher rates aren’t important if rates quickly fall. But that doesn’t seem likely.

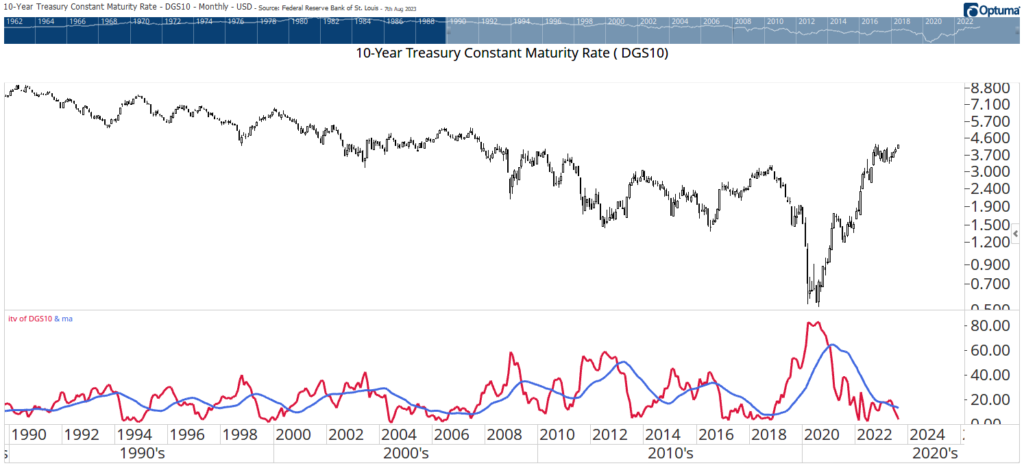

The chart below shows monthly values of 10-year Treasury rates. This is a benchmark for long-term interest rates. Mortgage rates, for example, show a high correlation to 10-year rates.

Rates Are at the Beginning of an Uptrend

The indicator at the bottom of the chart measures volatility. It rises when rates fall and declines when rates rise. The blue line is the moving average of the indicator. It highlights transitions in the trend.

In June, the indicator fell below its moving average. This tells us that rates are at the beginning of an uptrend.

The pandemic crash in rates distorted the scale of the chart. The current reading of the indicator looks low but is still rather high. It would need to fall more than 80% to reach a new low. That shows there is significant upside potential in interest rates.

Rates are really at a normal level right now. They are higher than the rate of inflation, and they should be. When rates are below inflation as they were in recent years, investors are losing money. That can’t last long, and it didn’t.

In time, markets and consumers will adapt to normal rates. The last few years were an aberration that will be missed. But we can still function and profit with rates at higher levels, and we’re likely to get that chance for the next few years.

This is just the new normal…

Until next time,

Mike Carr

Senior Technical Analyst

P.S. If you’re looking for stocks that are performing well in this new normal, you should check out what my colleague and fellow CMT Adam O’Dell has on offer in his premium Green Zone Fortunes stock research service.

Like me, Adam is always on the hunt for what’s working now, and he’s created a well-diversified model portfolio full of stocks that should thrive from here. For more information, click here.