Editor’s Note: In September, Qualcomm noted interest in acquiring Intel as the AI revolution entered its next phase. The news triggered a spike in INTC’s stock price, but Chief Research Analyst Matt Clark knew something was up…

Since publishing this deep dive into Intel’s role in the race for AI dominance, its stock has lost more than 12%. And Green Zone Power Ratings now rates it a “0 out of 100.”

Read on to see why Intel lost the AI popularity contest in 2024.

Is Intel “Mr. Popular” Again?

The investing world can feel like a popularity contest.

Intel Corp. (Nasdaq: INTC) was once “Mr. Popular ” and one of the largest chipmakers by revenue.

Companies wanted to install Intel chips in their personal computers (PCs) and other products, and people wanted to buy those computers in droves.

But Intel’s popularity waned alongside the PC market…

In 2023, the PC shipments fell 14.8%, marking the second straight year of double-digit declines.

Suddenly, Intel was eating lunch alone because no one wanted what it had to offer.

Until now…

In the span of a few days, Intel has regained popularity amid reports of semiconductor maker Qualcomm Inc. (Nasdaq: QCOMM) potentially acquiring Intel.

Bloomberg also reported that asset management firm Apollo Global Management had also approached Intel about a multibillion-dollar investment offer.

Is Intel “Mr. Popular” again?

Today, I’ll examine Intel’s fall from grace and share which deal I believe has the most potential. More importantly … what does this mean for you as an investor?

Semiconductor Companies Coming in Hot

In 2022, major semiconductor companies like Nvidia Corp. (Nasdaq: NVDA), Qualcomm Inc. (Nasdaq: QCOM) and Advanced Micro Devices Inc. (Nasdaq: AMD) all posted declining revenue.

The eight largest semiconductor companies in the U.S. combined reported a nearly $10 billion revenue drop for the year.

However, after a rough first quarter of 2023, the tide started to turn, and semiconductor companies picked up steam, thanks in large part to the massive artificial intelligence (AI) mega trend.

Revenues for companies in the S&P Semiconductor Select Industry Index reached nearly $100 billion in the second quarter of 2024.

A bulk of that gain comes from Nvidia and increased demand for its AI-related chips.

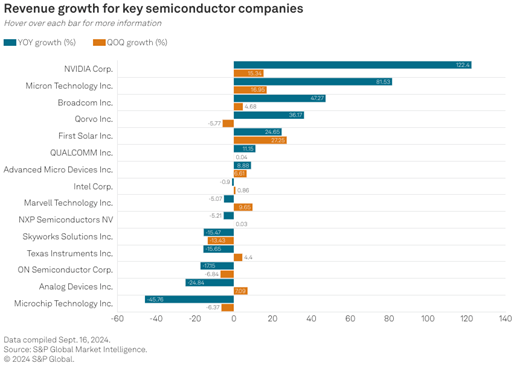

However, Nvidia wasn’t the only semiconductor company gaining additional revenue:

Right in the middle of the chart above, you’ll see what was once the leading chipmaker by revenue: Intel Corp.

Its revenue growth has been pretty stagnant … especially in 2024.

After declining in 2022, Intel’s revenue started to pick back up in 2023. But a rough start to 2024 has led to flat revenue growth.

The slowdown is related to headwinds in the PC market that I mentioned earlier and a significant increase in market competition in the semiconductor space.

Qualcomm, Apollo or Go It Alone?

INTC stock got a boost after Friday’s news of Qualcomm’s “friendly” deal to acquire it.

The boost was made even stronger Monday on Apollo’s interest in a $5 billion investment.

However, neither of those reports has propelled INTC to its former glory yet:

Despite INTC’s stock pop, it remains well below both its 50-day and 200-day exponential moving averages … mainly due to the bearish price movement since the start of 2024.

When considering if either of these two deals comes to fruition, my money is on Apollo’s investment.

Intel has spent billions pivoting away from its PC segment and into AI computing. This got a significant boost when Amazon.com Inc. (Nasdaq: AMZN) announced a multibillion-dollar deal with Intel to co-invest in a custom AI semiconductor.

That investment could be strong enough to push the raiders from the gate and keep Intel independent.

Adding in a potential $5 billion equity investment helps buoy that position.

Accepting a deal to be acquired from Qualcomm amounts to Intel admitting defeat. It says they couldn’t rebound from a tough few years.

Plus, going with Qualcomm is going to introduce a new foe to the mix: U.S. government regulators.

These are the kinds of deals that face heightened scrutiny amid antitrust laws.

As an investor, you have to look at all the angles.

And here’s one more fact to consider…

Based on Adam’s Green Zone Power Ratings system, Intel rates a “High Risk” 1 out of 100 and rates in the red in five of the six metrics that make up its overall rating.

Neither of these propositions to bring Intel back to the cool kid’s table is a guarantee.

And our ratings system says Intel is one stock to avoid right now.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets