This has not been a great year for the health care sector…

The State Street Health Care Select Sector SPDR ETF (XLV), which tracks the health care stocks of the S&P 500 Index, is the worst-performing major sector of 2026, down over 7%.

As for the “why,” you can point the finger at Washington.

The Trump administration has made lowering drug costs a priority. That’s good for you and me, of course. But it’s not beneficial for Big Pharma’s profit margins.

Last year, President Trump signed an executive order pushing for “most-favored-nation” drug pricing, which would bring astronomical U.S. drug prices in line with cheaper international prices.

While the deals are voluntary and the jury is still out on whether they stick, they were enough to spook investors.

Meanwhile, Medicare’s new drug price negotiation powers under Biden’s Inflation Reduction Act took effect this year. The first 10 treatments subject to price negotiations saw their prices drop by 38% to 79%.

Again, that’s wonderful for you and me… and for the taxpayers funding Medicare. But it’s not exactly great news for Big Pharma.

The Congressional Budget Office calculates that the price negotiations will save Medicare close to $100 billion over the next decade. That’s effectively $100 billion taken out of Big Pharma’s pocket.

Few people will cry for Big Pharma… and even fewer for health insurance companies. At some point, we’ve all gotten a medical bill that felt egregious. But as investors, it’s important to keep our emotions out of it.

With all of the bearishness toward the sector, might there be some opportunities flying under the radar?

Let’s see what my system has to say.

A Peek Under the Hood

Looking at the sector as a whole, it could be a lot worse.

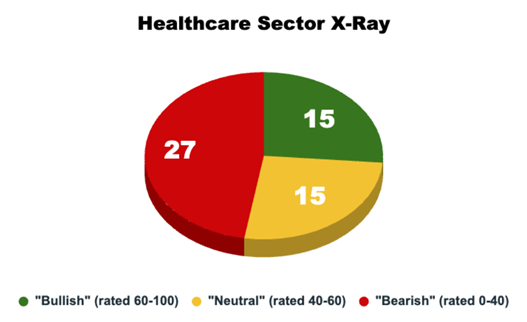

Most of the stocks rate poorly. At 27 out of 57, fully 47% rate as “Bearish” and another 15 rate as “Neutral.”

But 15 out of 57 rate as “Bullish,” meaning they have a score of 60 or higher. That’s more than a quarter of the total.

(For those new to my Green Zone Power Ratings system, “Bullish” rated stocks outperform the S&P 500 by double on average over the following year.)

Clearly, this isn’t a time to buy and hold the health care sector. It’s performing poorly, and most of the stocks rate as “Bearish” or “Neutral” on my system.

However, there are enough “Bullish” ratings to warrant a deeper look.

So, let’s keep digging!

Where Do Health Care Stocks Pick Up Points?

The Green Zone Power Rating is a composite score based on six primary factors: momentum, size, volatility, value, quality and growth, each of which is composed of several sub-factors. (As we are looking at large-cap constituents of the S&P 500, I don’t consider size when doing the sector X-ray.)

Let’s take a look at where health care stocks are putting points on the board.

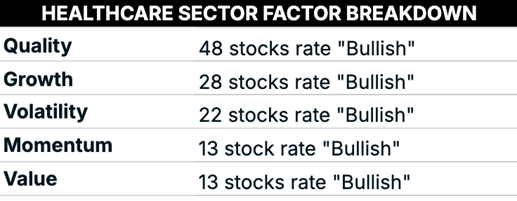

A surprisingly high number rate as “Bullish” on their quality factor. Fully 48 out of 57, or 84%, have a quality factor of 60 or higher.

Perhaps ironically, this is precisely what made them a target of Uncle Sam. My quality factor is a composite of subfactors for profitability, balance sheet strength and capital efficiency.

And branded pharmaceuticals enjoy high profit margins due to patent protections that grant them a legal monopoly for a fixed period.

There’s nothing wrong with that, of course.

Patents ensure that companies recoup their research and development costs and incentivize them to develop new treatments. But they do make the companies a target, and fears that government pressure will erode profits going forward are legitimate.

Let’s talk about momentum now. While the sector as a whole is distinctly lacking in momentum, there are 13 health care stocks bucking that trend that currently rate as “Bullish” on their momentum factor.

That’s the sort of thing that gets my attention… and alerts me to the possibility of a good trading opportunity.

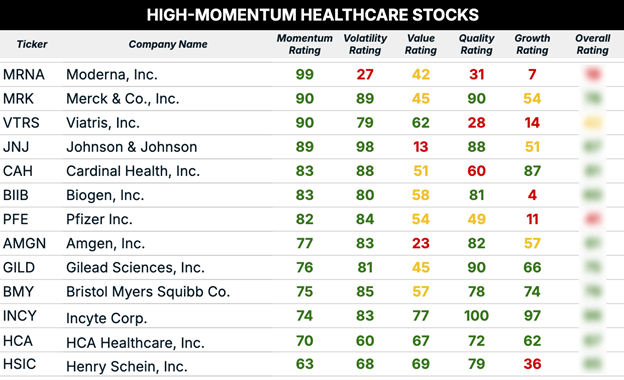

So, let’s give those 13 high-momentum health stocks a look.

Bucking the Trend

Remember Moderna (MRNA)?

It feels like an eternity ago, but Moderna quite literally changed the world. Its COVID-19 vaccine was the first mRNA treatment to go mainstream, serving as proof of concept.

Today, the company is making history again with a cancer vaccine. A recent phase two study showed that Moderna’s mRNA-based therapy, intismeran autogene, when combined with Merck’s Keytruda, reduced the risk of melanoma recurrence or death by 49% compared with solely using Keytruda.

We’re at the tip of the iceberg of what this technology can potentially do.

Rather than a one-size-fits-all drug, personalized mRNA cancer vaccines can potentially be tailored to an individual patient’s specific tumor mutations, essentially teaching the immune system to hunt down that patient’s particular cancer cells.

We’re still a long way from ridding the world of cancer. But the news has helped to shake Moderna out of its long, post-pandemic hangover.

The stock rates a 99 on its momentum factor. But before you back up the truck and start loading up on the shares, note that this is still a very speculative stock that rates as “Bearish” overall.

For a more balanced stock, consider Incyte Corp (INCY), a mid-sized biopharma company focused on cancer and dermatology treatments.

INCY rates strongly across all factors and boasts a perfect 100 on quality.

There is risk here, of course. Its bread and butter product – Jakafi (ruxolitinib), a treatment for certain forms of cancer – goes off patent in 2028.

So, a bet on Incyte is a bet on its pipeline of new treatments.

To good profits,

Adam O’Dell

Editor, What My System Says Today