With investing, you win by not losing.

Even mediocre returns will compound into a proper fortune over time if you simply avoid major drawdowns.

This is especially true with dividend investing.

As the longtime financial writer Raymond DeVoe, Jr. wrote:

“More money has been lost reaching for yield than at the point of a gun.”

I’ve done it, and I’m betting you’ve done it. Given enough time, every dividend investor will succumb to yield chasing, but it’s a bad idea most of the time.

I’d rather own a conservative 3.5% yielder that is safe than a 10% yielder that is likely to slash the dividend and fall into financial distress later.

The first is a recipe for consistent, if somewhat boring, gains. The second is a recipe for losses and perpetual heartburn.

This brings me to our dividend stock of the week, Kellogg Company (NYSE: K).

Kellogg is a quintessential conservative dividend stock. It sells products — breakfast cereals and salty snacks — that are iconic and more or less future-proof. Apart from its iconic cereals, its brands include:

- Keebler.

- Cheez-It.

- Pringles.

- Famous Amos.

Sure, consumer tastes change over time. But it’s not like Frosted Flakes can ever be disrupted by a new killer app out of Silicon Valley. Kellogg is a timeless company with timeless brands.

At current prices, Kellogg yields 3.5%. And even more importantly, Kellogg has raised its dividend every year since 2004. Over the past 10 years it’s raised its dividend at a respectable 4.5% compounded annual rate. You’re not getting rich at that rate, but it’s well ahead of inflation.

Let’s take a look at how Kellogg’s stock stacks up in our Green Zone Ratings model.

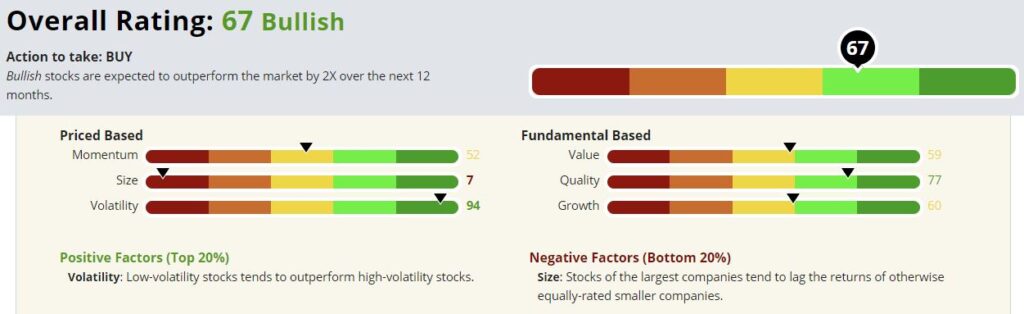

Kellogg’s Stock Rating and Dividend

All investments have opportunity cost — the risk that you could have made more money elsewhere — so we want to make sure that any dividend stock we buy has at least the possibility of generating respectable capital gains.

Well, Kellogg fits the bill. It rates a 67, putting it firmly in “bullish” territory for us. Money & Markets Chief Investment Strategist Adam O’Dell’s extensive backtesting suggests that stocks with ratings over 60 are expected to outperform the overall market by 2X over the next 12 months.

Kellogg’s Green Zone Rating on October 27, 2020.

Let do a deeper dive to see what’s driving Kellogg’s bullish rating.

Volatility — You want low volatility when investing for income. It’s hard to stomach wild price swings when you just want to earn a couple percent in dividends. Well, Kellogg scores a 94 here, making it one of the lowest-volatility stocks in our universe (a high score here means low volatility).

Quality — Kellogg also rates highly based on quality, scoring a 77. Our quality metrics are driven mostly by profitability. The company sports a return-on-equity of 33%. While breakfast cereals and snacks are a commodity business, Kellogg enjoys premium pricing due to its strong branding.

Growth — Kellogg’s growth rating is a respectable 60. This is impressive given that none of the company’s major products are “spring chickens.” This is an older company with established brands. It’s worth noting that Kellogg has also benefitted from the trend of eating at home during the pandemic. It’s provided a nice bump in sales this year.

Value — This isn’t a deep-value stock by any stretch of the imagination, but Kellogg rates a respectable 59 based on value. This places it in the top half of the companies in our universe. Often, companies that rate highly based on quality rate poorly based on value, as investors pay up to get the best. But Kellogg is a nice exception to that rule.

Momentum — At 52, Kellogg is middle-of-the-pack in terms of momentum. It’s essentially pacing the market’s momentum, which is pretty impressive. This is a market that has rewarded high-growth tech stocks. It’s impressive to find a stodgy old snack maker in the mix.

Size — Alas, Kellogg is a large company. It’s not some small, yet-to-be-discovered diamond in the rough. It rates a 7 based on size.

Bottom line: Are you going to get filthy rich with Kellogg’s stock?

Probably not.

But will you collect a respectable and growing dividend while outperforming the market over the next year?

I would say that’s likely.

Money & Markets contributor Charles Sizemore specializes in income and retirement topics. Charles is a regular on The Bull & The Bear podcast. He is also a frequent guest on CNBC, Bloomberg and Fox Business.

Follow Charles on Twitter @CharlesSizemore.