Last year, COVID-19 was the great disruptor.

Stay-at-home orders and social distancing forced businesses to rapidly change the way they were doing things.

Some excelled by focusing on e-commerce and offering delivery and pick-up options. Others faltered, declaring bankruptcy or worse.

Still, others took it as a learning opportunity…

Check out these headlines:

- “Macy’s plans to shut 10 department stores in January.”

- “Macy’s Follows Amazon, Walmart in Development of Digital Marketplace.”

- “CVS to close 900 stores in big retail strategy shift.”

When you read about store closures, it usually means the business went in the wrong direction.

But things might be different for Macy’s Inc. (NYSE: M) and CVS Health Corp. (NYSE: CVS).

Retail’s Big Shift

COVID-19 hammered Macy’s. Its stock hovered near 12-year lows for eight months following the March 2020 market crash.

But 2021 has been a different story. Investors poured into the stock, driving it 300% higher over the last year.

CVS fared a little better through 2020, thanks to the nature of its business. I would hope a drug store could survive a global pandemic. Stock gains aren’t as impressive, but CVS’ share price has grown 44% over the last 12 months.

And now, these companies are changing up their strategies for the future.

Macy’s is working with a consulting firm to bolster its online presence, according to Macy’s CEO Jeff Gennette. The news, along with a blockbuster third-quarter earnings report, sent Macy’s shares 21% higher on Thursday.

CVS, on the other hand, is closing 10% (around 900 stores) of its physical locations over the next three years. It’s part of an effort to focus on more of its health services business.

I think this is an exciting shift for both companies. It shows that these more traditional businesses are embracing change.

Let’s see how they stack up in Adam O’Dell’s proprietary Green Zone Ratings system.

Green Zone Ratings: Macy’s and CVS

At first glance, both of these stocks look great right now.

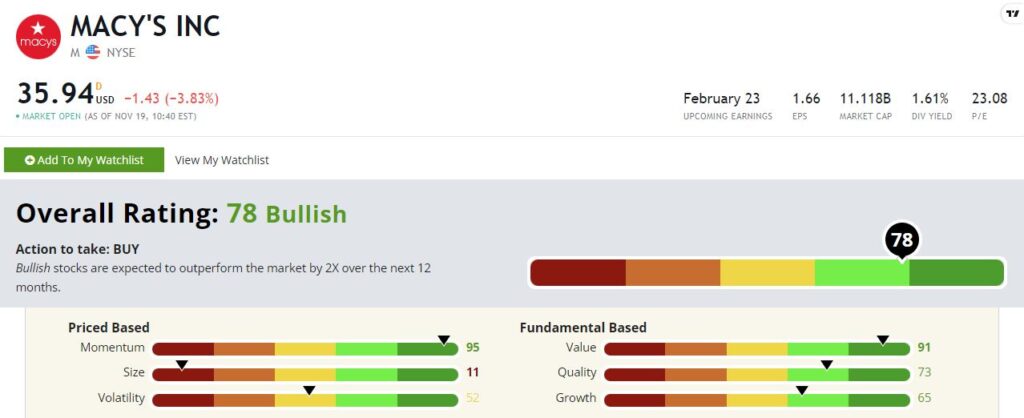

Macy’s Inc.’s Green Zone Rating on November 19, 2021.

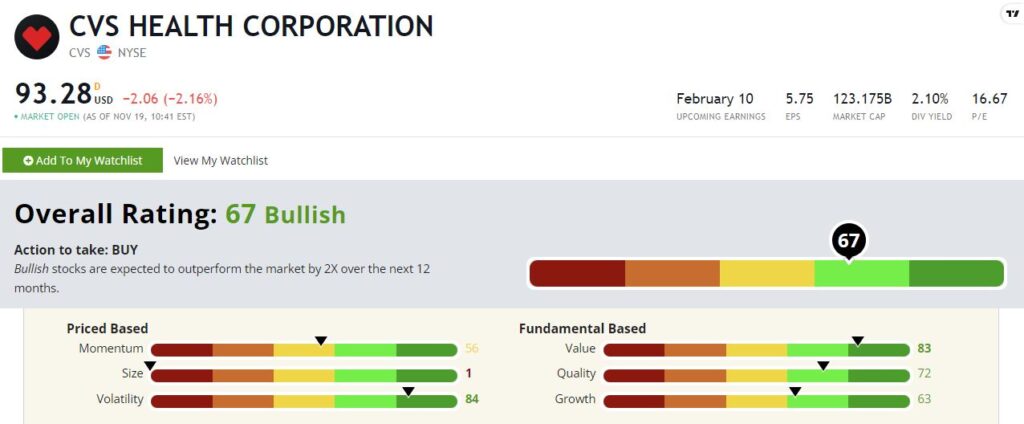

CVS Health Corp.’s Green Zone Rating on November 19, 2021.

Both stocks are “Bullish,” which means we expect them to outperform the overall market by two times over the next 12 months.

These are also both great value plays. CVS sports a value rating of 83, and Macy’s comes in at 91! Macy’s price-to-earnings ratio of 13 is much lower than the consumer discretionary average of 32.

Looking at both stocks side-by-side, it’s interesting to see how similar they are across Green Zone Ratings. (Read more about each of the factors at the end of this story.)

Both boast great ratings in value, quality and growth, the factors based on fundamentals.

Both are huge companies. That’s why their size ratings are so low.

It comes down to momentum and volatility. CVS has been more of a steady ride up over the last year, hence its lower momentum score and great volatility rating at 84 (remember, a higher volatility score denotes lower volatility).

Macy’s has enjoyed some recent momentum, but it has not been immune to big sell-offs along the way. As I’m writing, M is down almost 5% Friday morning after popping 20% higher on Thursday.

Bottom line: I think both Macy’s and CVS are stocks worth a spot on your shortlist, at least right now.

Macy’s added 4.4 million new customers last quarter, and we are heading into a huge holiday season.

CVS may not be as exciting through the end of 2021, but I think there is a lot of potential to establish itself as a threat in the health care space. It has more than 9,000 stores across the U.S., Puerto Rico and Brazil. CVS could become the No. 1 stop for any minor ailments or illnesses.

Green Zone Ratings Factors

Momentum — Strongly uptrending stocks earn higher momentum ratings. We prefer to buy stocks that are already trending higher and at a faster rate than the overall market. This approach can increase our odds of success and decrease risk.

Value — Less expensive (aka “cheap”) stocks earn higher value ratings. We prefer to buy great companies at good prices because the price we pay impacts future returns. Overpaying for a stock can be a costly mistake.

Quality — High-quality companies earn higher quality ratings. We prefer to buy high-quality companies, of course! To determine quality, the model considers a company’s returns, profit margins, cash flows, debt ratios and operational efficiency, among other things.

Growth — High-growth companies earn higher growth ratings. All things equal, we prefer to buy companies that are growing both revenues and earnings at faster rates than the market and economy.

Size — Smaller companies earn higher size ratings. We prefer to buy smaller companies for the extra “juice” that typically comes with them.

Volatility — Less volatile stocks earn higher volatility ratings. We prefer low-volatility stocks because they’re proven to generate superior risk-adjusted returns over the long run — with less heartburn.

Best investing,

Chad Stone

Assistant Managing Editor, Money & Markets