Nvidia Corp. (Nasdaq: NVDA), the largest maker of graphical processing chips enhancing computer displays and visuals, announced solid sales performance closing out its fiscal 2024.

For the essential holiday sales quarter ending January 2024, Nvidia set new all-time high revenue levels.

Nvidia Quarterly Revenue Record

Specifically, total fourth-quarter sales reached $22.1 billion — up 22% compared to the prior July-September period.

More importantly, revenue skyrocketed a massive 265% higher compared to a year ago.

Nvidia technology clearly won substantially more consumer and corporate spending despite shakier global economic conditions affecting other electronics providers.

Diving deeper into NVDA’s financial division, the data center category set its own new $18.4 billion quarterly revenue record.

This business mainly sells specialized components that power artificial intelligence, supercomputing complexes and cloud-based services. Its over 40% yearly expansion underscores Nvidia’s pole position supplying processing infrastructure enabling next-generation AI applications.

Meanwhile, NVDA’s separate gaming and professional graphics segments maintained solid double-digit percentage gains, demonstrating stability beyond just data center momentum.

Across the entire business, gross profit margins also swelled over 12 percentage points annually, nearing 80% at peak efficiency.

In total, for the full fiscal year, NVDA amassed $60.9 billion in total revenue — fully doubling prior year sales at a 126% yearly improvement pace no analyst projected.

And the company converted much of that enormous revenue influx into $29 billion-plus net profit, equaling almost $12 earnings per share.

Investors reacted ecstatically to the blockbuster financial performance, elevating Nvidia to more than $750 per share in Thursday pre-market trading.

Looking ahead, Nvidia leadership guided expectations for minimal cooldown during the first quarter, projecting continued data center and graphical chip momentum.

Management pointed to surging client orders globally across cloud providers, financial groups and manufacturing leaders seeking Nvidia processing solutions.

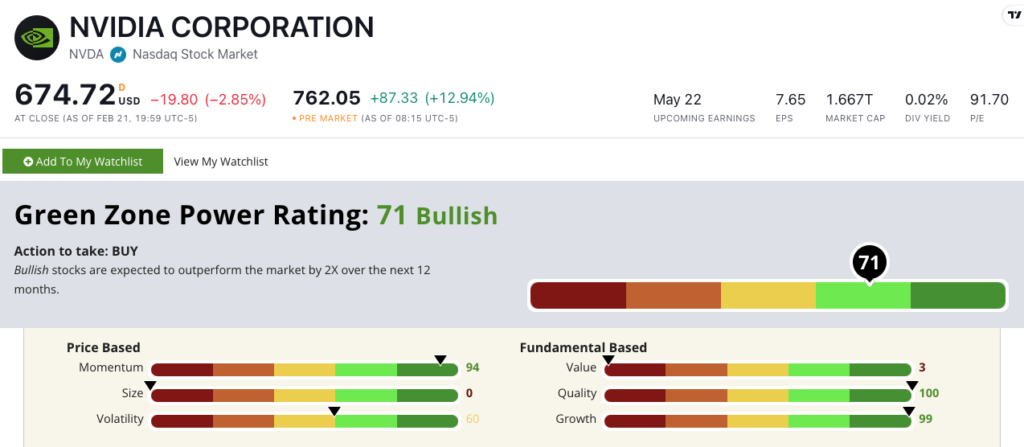

NVDA’s Green Zone Power Rating

At the time of its earnings announcement, NVDA rated 71 out of 100 on Adam O’Dell’s proprietary Green Zone Power Ratings system.

NVDA’s Green Zone Power Ratings in February 2024.

That means we are “Bullish” on the stock and expect it to outperform the broader market by 2X over the next 12 months.

The company rated 100 on Quality, with returns on assets, equity, and investment blowing the doors off the semiconductor manufacturing industry averages.

Nvidia also records a gross margin of 76%, while its industry peers average just 56%.

NVDA rates a 99 on Growth thanks to its 265% growth in revenue year over year.

The stock has been on a tear, rising 226.7% over the last 52 weeks, leading to its 94 rating on Momentum.

Bottom line: If execution persists, keeping supercharged growth and margins near peaks, Nvidia seems positioned to extend its market cap weight toward $1 trillion.

However, economic turbulence and competitive responses pose constant challenges in the long run.