It’s nearly 2023, and we’re on the precipice of something that’s never happened in our lifetimes: A recession is coming — and when it does, it will surprise no one.

Believe it or not, that’s good news because it lets us buy stocks — and high-yield closed-end funds (CEFs) — cheap right now. We don’t have to wait months for the recession to subside.

I’ve got an 8.4%-yielding CEF for you to consider below. It’s discounted twice: Once because the stocks it holds, which include S&P 500 standouts like Visa Inc. (NYSE: V), UnitedHealth Group Inc. (NYSE: UNH) and Amazon.com Inc. (Nasdaq: AMZN), have sold off, and second because the fund itself trades at a rare discount.

Now is the time to buy this one (and the other buy-rated funds in the portfolio of my CEF Insider service). Here’s why.

The “Real” Yield Curve Locks In a 2023 Recession

A closely watched recession predictor is the relationship between the yields on the 2-year and 10-year Treasury notes. When the yield on the 2-year moves above that of the 10-year, a recession is likely on the way.

That’s pretty well understood by most people, but this long-touted indicator has been wrong at times. That’s why I look for an inversion of the 3-month and 10-year Treasury yields, which has predicted every recession in the last 50 years. And the shorter yield indeed peaked above the 10-year yield briefly in mid-October, indicating a recession is on its way, likely within a year.

Stock markets are hardly surprised; they’ve been pricing in a recession for a year now. And therein lies our buying opportunity, because it’s extremely rare for stocks to fall into a bear market for 12 months.

In fact, it hasn’t happened before a recession in the last 50 years. In that time, stocks have either been slightly down or flat (2001, 2008) or up (1991, 2020) in the year preceding the recession. In other words, this recession is the most anticipated one in recent history and the most priced in.

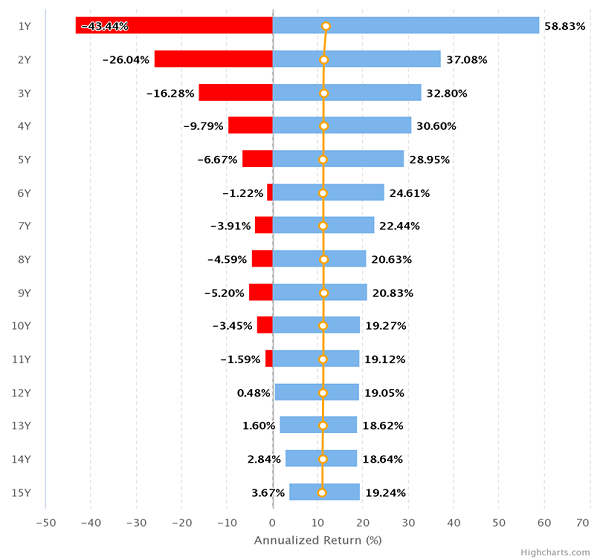

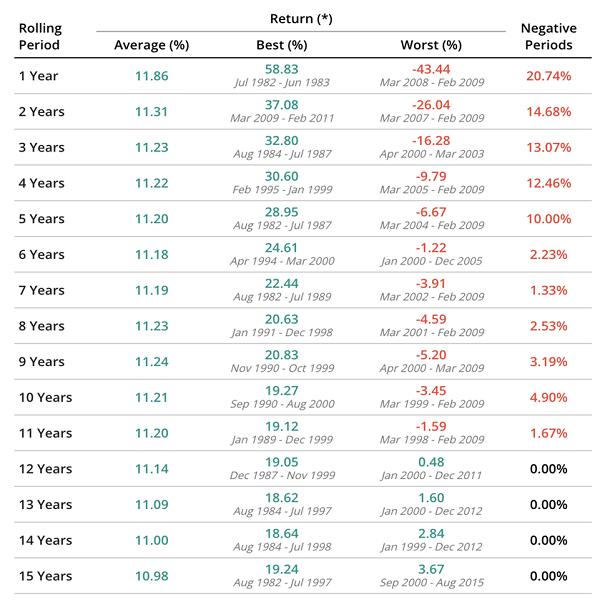

How Long You Need to Wait

This likely means we won’t need to wait as long for prices to recover after the recession hits, as the market is prepared. But how long will we have to wait?

Average Wait Time: One Year

Source: Lazyportfolioetf.

Historically speaking, negative one-year returns are pretty rare (they happen 20.7% of the time in total), and those negative returns turn positive 100% of the time if we wait long enough.

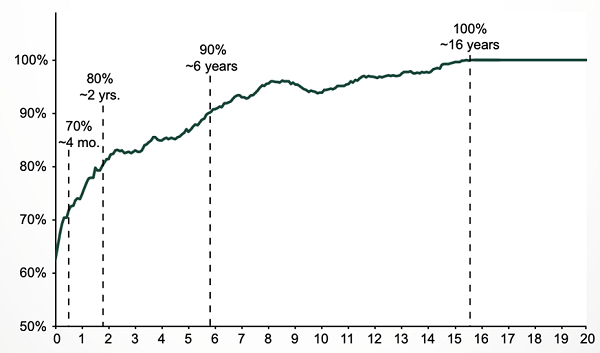

Over Time, Negative Periods Disappear

Note also that many of those unusually long periods where the market provides negative returns were between the dot-com bubble and the housing bubble — two periods of massive run-ups in assets untethered to reality, when markets had failed to price in future downturns. In other words, the opposite of today’s market conditions.

Big, Unpopped Bubbles Lead to the Longest Downturns

Source: Lazyportfolioetf.

This makes it plain to see that the market has priced in more pain than it typically has, including a recession, which stocks haven’t done for two generations. Which is why now may be the best time to buy.

An 8.4% Dividend to Play This Pre-Recession Dip

There are three ways you can buy this priced-in recession: stocks, ETFs or — our favorite route — high-yield CEFs.

I say “our favorite route” because CEFs pay us at least 7% dividends, so we’re getting most of our return in safe cash. CEFs also routinely trade at discounts to their true value (and especially so today) and let us hold the same household-name stocks we likely do now, except with much higher dividends than we get by purchasing them ourselves.

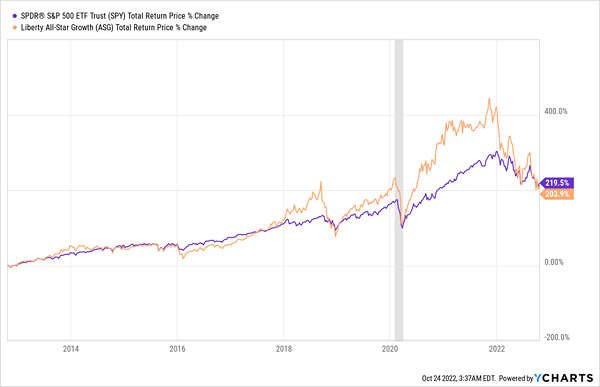

A CEF like the Liberty All-Star Growth Fund Inc. (NYSE: ASG), for example, holds many top S&P 500 names while paying an 8.4% dividend yield. ASG can afford to pay this hefty payout by periodically and strategically selling its holdings and taking profits, which it then hands to investors as cash dividends.

Plus, as I mentioned off the top, ASG is on sale in two ways: First, it now trades at a 2.4% discount to net asset value (NAV, or the value of the stocks in its portfolio), even though it’s traded at a premium for most of the last decade. And then there’s this:

The Big Sale Appears

ASG has historically outperformed the market, but it’s converged on the S&P 500 in 2022 as its tech holdings have experienced a bigger sell-off than the broader market and its normally large premium (which was 20% in 2018 and over 10% for most of 2020 and 2021) has turned into a discount. This gives us two opportunities to profit: First as ASG’s portfolio reverts to the historical mean of outperforming the S&P 500 and as the fund’s discount vanishes.

Until those things happen, we have an 8.4% yield to keep us flush with cash and help us avoid selling into a bear market.

To learn more about generating monthly dividends as high as 8%, click here.