Nine weeks ago, our fellow income investors were concerned about rising tariff tensions and falling stock prices (sound familiar?). So in late May, we discussed seven dividend payers (yielding 6% on average) that wouldn’t go down if stocks-at-large kept dropping.

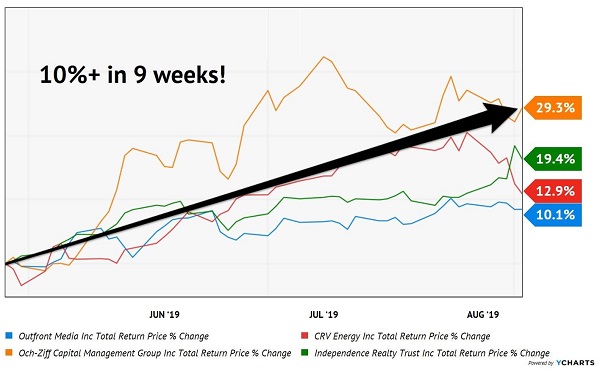

The broader markets soon reversed, as they usually do when pessimism is running high. But our defensive dividend machines did even better. Five out of my seven “never go down” plays beat the S&P 500. On average they returned 12.5% (including their big dividends) over the last nine weeks. A percent a week or better will sure boost your retirement account quickly!

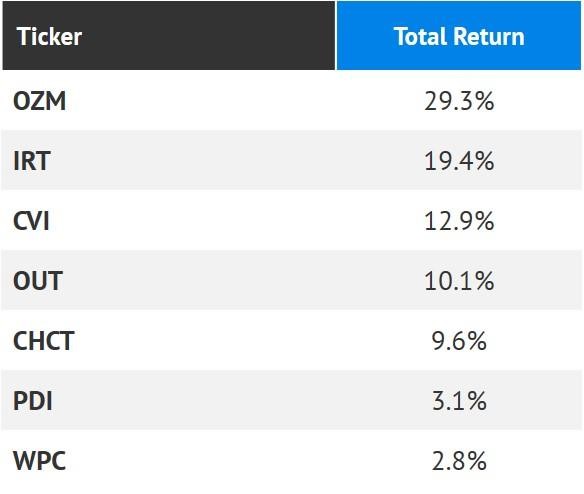

Big Gains in 9 Weeks

As you can see, the winners really ran. Their May resilience (the fact that they finished that month higher when most other stocks were creamed) carried over and continues today. Their investors are still riding high with fast double-digit gains that sailed through last week’s selloff:

Never Go Down, Usually Go Up

Of course these dividend trees won’t continue growing to the sky. These hot stocks will eventually take a break. And that will leave anyone sitting on these profits with two choices:

- Sit on your hands and keep banking the big dividend, or

- Book the 12.5% gains on these shares and hop on the next income horse with double-digit upside over the next nine weeks.

Both approaches can work, and it’s possible to employ them together in a single retirement portfolio. You can think of one bucket of dividend payers as your long-term positions, and the next one as your “rent-a-payer” portfolio.

Regardless of our time frame, we are only going to deal with high-quality dividend payers. Fundamentals such as profits, cash flows, payout ratios and business prospects tell us “what to buy.” Next, depending on your personality (and return requirements!) we should determine “when to buy” — and also sell.

Strategy No. 1: Buy Right, Sit Tight and Add Smartly

My Contrarian Income Report service provides a safe, heartburn-free way to retire on dividends and enjoy some price upside, too. We don’t over-trade. In fact, in four years, we’ve only sold 13 positions! That’s about three sales per year.

We don’t have to sell often because we buy high-quality, high-paying stocks and funds when their prices are cheap. Our contrarian approach helps us “time” our entries by focusing on plays when they are out-of-favor and hence in the bargain bin.

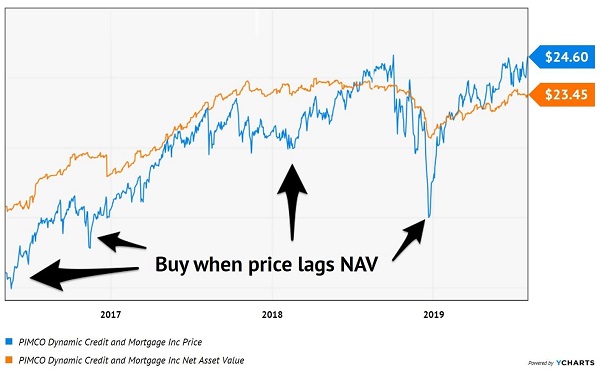

For example, we bought PDI’s sister fund, the PIMCO Dynamic Credit and Mortgage Income Fund (PCI), in May 2016. The talented PIMCO team has handpicked a portfolio of 835 high paying bonds, which have powered our 8% and 9%, yields.

These bonds also appreciated in value by 16%. This is reflected in the fund’s higher NAV, and this is important because this underlying value acts like a “magnet” for PCI’s trading price. As a CEF, the fund has a fixed pool of shares and is subject to the short-term whims of the market (like an individual stock).

As days and weeks turn into months and years, PCI’s price always gravitates towards its NAV. This has worked in our favor because we’ve had a “buy” rating on the fund whenever its NAV drifts too far below its price:

We Buy When Price Lags NAV

These price lags have provided us with additional opportunities to add to our position (and for new subscribers to get in at a good price). When PCI trades at or above its NAV (as it does right now), we don’t do anything. We just bank the 8.5% dividend.

(I explained our CEF strategy to The Wall Street Journal on Monday.

Mr. Owens says high-premium CEFs are often similar to high-flying stocks with big price-to-earnings ratios. “Maybe it’ll work out for investors who buy high and sell even higher, but income investors should play the probabilities,” he said. “And the odds favor the conventional wisdom: Never buy a CEF trading at a premium.”

You can read the WSJ’s full CEF column here.

Our contrarian income approach is simple, and it works. We’re sitting on 87% profits including dividends from PCI, while the riskier S&P 500 returned only 52% over the same time period. Additional purchases in between (when we had a buy rating on the fund) also generated 20%+ annual gains.

One click to 8%-plus dividends and 87% total returns, what’s not to like? Well, for those of you itching for more action and even higher returns, here’s what to do.

Strategy No. 2: More Clicks, More Opportunity for 20%-plus Per Year

In the long run (months and years), fundamentals drive stocks. This is why safe dividends and dividend growers are the way to go. They will outperform non-payers and measly-payers over any meaningful time period.

But in the short run (days and weeks), there are “technical” factors that matter more. And I’m not talking about chart patterns, waves or other mythical models. I’m talking about good old-fashioned supply and demand.

These are “momentum income” buys. It’s a real thing and it can be a useful tool, even to us fundamental-focused investors.

While interest rates have downward momentum, big dividends are in high demand. I like five “2008-proof” payers yielding 7.5% in particular right now. These stocks didn’t blink during the recent carnage, a sign that their shares are ready to run when markets calm down.

To learn more about generating monthly dividends as high as 8%, click here.

• This article was originally published by Contrarian Outlook. You can learn more about Brett Owens and Contrarian Income Report right here.