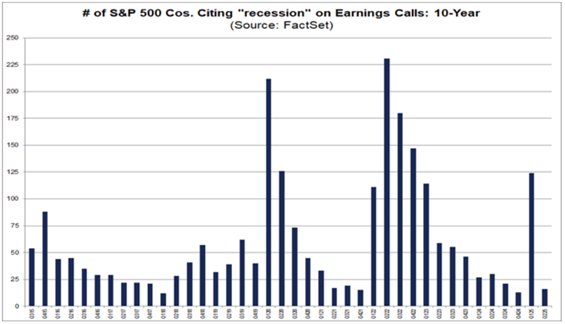

Despite mixed employment data, higher production costs and flat consumer costs, S&P 500 companies are no longer worried about the dreaded R word: recession.

According to data firm FactSet, there’s been a significant drop in companies citing the word “recession” in quarterly earnings reports:

Only 16 earnings calls (4% of companies) for the second quarter used the word “recession,” compared to 124 in the previous quarter.

The five-year average is 74, and the 10-year average is 61.

On the sector level, the highest percentage of companies mentioning “recession” is just 10% for real estate and 7% each for financials and industrials.

We’ll keep a close eye on this trend going forward…

But for today, I’ll review one company’s earnings and then analyze “bullish” and “bearish” earnings potentials for next week.

The Deere Has Stopped Running

Last week, I mentioned the turmoil that Deere & Co. (DE) was likely in due to tariffs on its component imports.

I said that Deere was likely to drop its earnings per share (EPS) and that I wouldn’t be surprised to see the company miss both revenue and EPS due to tariff impacts.

Well, I was partially correct … Deere is feeling the tariff pressure.

The company reported EPS of $4.75, slightly better than analysts’ expectations. Deere also notched $1.29 billion in revenue… but that’s well below the $1.73 billion it recorded during the same quarter a year ago.

Total sales dropped 16%, while net sales were off 9%.

The company said it was considering higher prices and production shifts to offset the nearly $600 million in tariff costs it expects to incur this year.

That prompted Deere to reaffirm its projections for sales to fall between 10% and 20% for the year.

As a result, the company’s stock got whacked for a 6% loss in trading yesterday. DE is still rated “Bullish” in our Green Zone Power Rating system, but I could see this bearish report and price action dragging the stock’s rating lower. (To see where DE stands now, click here to see how you can gain full access to Adam’s system with a Green Zone Fortunes subscription.)

Now, let’s look at potentially “bullish” earnings for next week.

These stocks are expected to beat their previous quarter’s EPS, and thus, if those expectations are met or exceeded, they could potentially trade higher.

“Bullish” Earnings to Watch

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are the nine companies that made the list:

I won’t focus on the companies with the biggest expected jump in EPS; instead, I’ll focus on a theme.

Discount retailers … namely The TJX Cos. Inc. (TJX) and Ross Stores Inc. (ROST).

According to retail analysis firm Placer.ai, these stores, which offer clothes and other household items at a cheaper price, have seen a surge in popularity.

Consumer discretionary spending is always fickle when prices are higher due to inflation and tariff trade wars.

So, consumers typically pivot. Rather than not spending money at all, they’ll go where they can buy cheaper items.

Places like Dollar General and Five Below continue to see consistent foot traffic in their stores. The same is true for Ross Stores and The TJX Cos. Inc.

I expect both TJX and ROST will outperform expectations for the quarter and report resiliency for the rest of the year as consumers hunt for bargains.

Now, we’ll switch gears and analyze potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are the two S&P 500 companies that passed this screen:

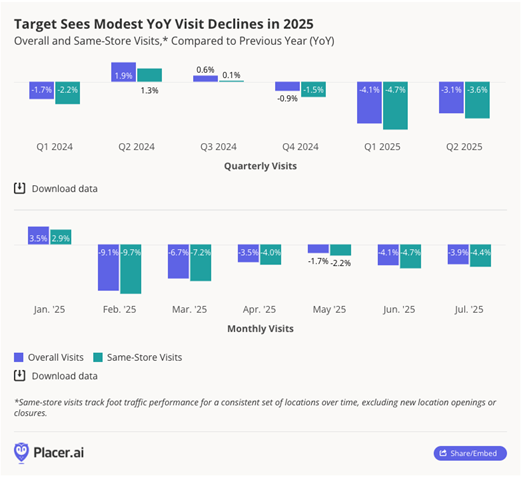

Just as discount retailers have seen steady foot traffic in 2025, large-scale retailer Target Corp. (TGT) has seen declines.

Except for January, Target has experienced declines in overall and same-store visits by customers every month of 2025.

Target is also facing headwinds from increased import tariffs, as some goods sold in Target stores are imported from other countries.

In the competition for shoppers, Target also has to contend with Walmart, which has been able to stabilize its foot traffic despite an increased push toward e-commerce sales.

Target is going to come very close to its earnings estimates this quarter, but its forward guidance for the rest of the year is something to pay attention to.

If Target misses on EPS and revenue, what will that do to its already “Bearish” standing on Adam’s Green Zone Power Rating system?

Buckle up for another interesting week of earnings.

Have a great weekend, everyone.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets