If I ever get burned out as a portfolio manager, I may start a new life as a trucker.

After taking a long road trip across the northern Peruvian desert with my two sons screaming at each other, my wife screaming at them to stop screaming, and our 11-month-old baby just screaming for the sake of screaming … the quiet, solitary life of a trucker sounds awfully good.

I’m (mostly) joking … I think?

At any rate, I think about this as I look at trucking and logistics company Ryder System Inc. (NYSE: R). I first mentioned Ryder back in February, and I want to reiterate that recommendation today.

Ryder’s Business Model and Dividend

Ryder is best known for its truck rental business. You’ve no doubt seen plenty of Ryder-branded vehicles trucking up and down America’s highways. The company owns a fleet of more than 270,000 trucks of assorted shapes, sizes and functions.

But the company does a lot more than that. It serves as a turnkey logistics and supply-chain operation, and — importantly — Ryder has recently expanded its offerings to include e-commerce fulfillment.

There may be no company on earth that is truly “Amazon-proof,” but Ryder is as close as you can get. It’s a gritty old-economy stock that is critical in the function of the new economy.

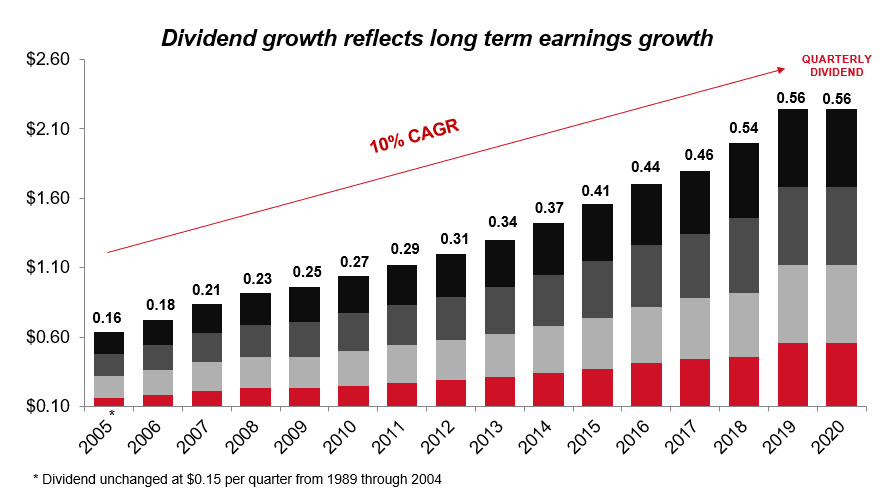

Let’s talk dividends. Ryder pays a current yield of 3.1%. That’s almost double the yield on the S&P 500 these days. And, with inflation back with a vengeance, Ryder‘s history of raising its dividend is a big plus. It has more than doubled its payout since 2011.

Source: Ryder Inc.

The trucking and logistics company raised its dividend by another $0.02 to $0.58 per share earlier this month. It has paid its cash dividend for 180 consecutive quarters. That’s 45 years of dividend history!

If you’re looking for a respectable dividend payer in a future-proof industry with a history of dividend growth that more than keeps pace with inflation, Ryder is a worthy addition.

Ryder Stock’s Green Zone Rating

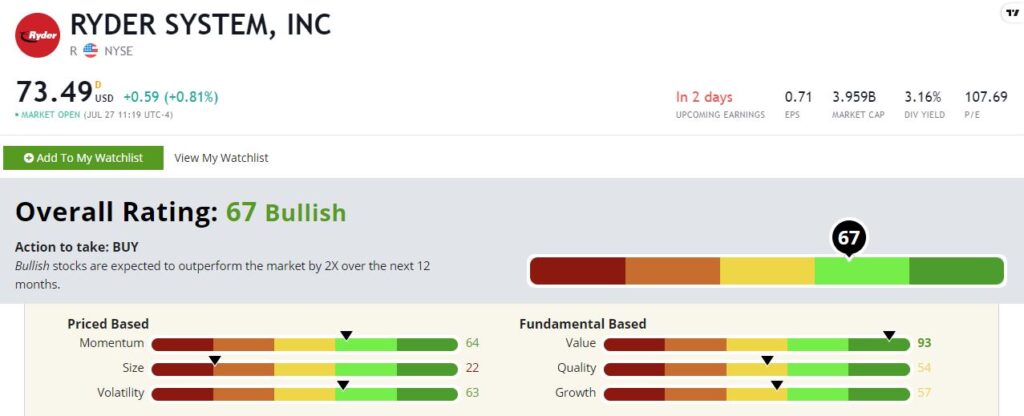

Ryder stock scores a “Bullish” 67 out of 100 on our Green Zone Ratings system, meaning we’d expect returns over the next 12 months to at least double that of the broader S&P 500.

Ryder System Inc.’s Green Zone Rating on July 27, 2021.

Let’s drill down to see what’s driving that rating.

Value — Ryder scores a 93 on our value factor, meaning it’s cheaper than all but 7% of the stocks in our universe. But this is also a value stock you might overlook when doing a more simplistic screen. At first glance, Ryder looks to be anything but cheap, with a price-to-earnings ratio over 100. But a deeper look shows that this is an anomaly caused by a temporary collapse in profitability last year. Our value factor takes a comprehensive look at valuation using multiple factors. It helps us to avoid getting tricked by a single outlier metric.

Momentum — Ryder stock also looks lively by our momentum metric with a score of 64. We like to see stocks trending higher. History shows that stocks trending higher tend to continue that upward movement. A cheap stock trending higher is best of all.

Volatility — Less is more when it comes to volatility. By simply avoiding the most volatile stocks, we avoid a lot of potential landmines. Ryder scores a 63 on volatility, meaning it is less volatile than about 63% of the stocks in our universe.

Growth — These days, “growth” seems to be synonymous with “tech.” Most of the fastest-growing stocks are in the technology sector. All the same, Ryder is firmly in the top half of all the stocks in our universe, with a growth score of 57. And with its growing reach into e-commerce, don’t be surprised to see that number improve in the years ahead.

Quality — Our quality rating rewards “capital-lite” businesses like software companies. Companies with a lot of physical assets — like trucks —get penalized. Yet Ryder still scores a respectable 54 here.

Size — Ryder is a large company with a market cap (outstanding shares times share price) of almost $4 billion. It rates low on our size factor at 22.

Bottom line: I favor stability over all else when it comes to dividend stocks. We’re buying these things for the income, after all.

In Ryder, we get a growing company in a stable industry with a long history of raising its dividends. There’s not much to dislike here.

To safe profits,

Charles Sizemore

Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is featured each week in the YouTube segment Investing With Charles. He is also a frequent guest on CNBC, Bloomberg and Fox Business.

Story updated on July 27, 2021.