With the market melting down, dividend stocks have built-in cushions. Unlike profitless tech shares, which rarely pay, our dividend payers’ yields go up when prices go down.

The result? Stronger price action for our favorite yield plays, thanks to attention from NASDAQ refugees.

But we need to be extra vigilant about dividend cuts. They, after all, provide a sickening “double whammy.” We lose our cash flow and some capital as the shares get repriced lower post-cut. And the drop can be even worse in panicked markets like today’s.

AT&T Investors Suffer Over and Over—From 1 Dividend Cut

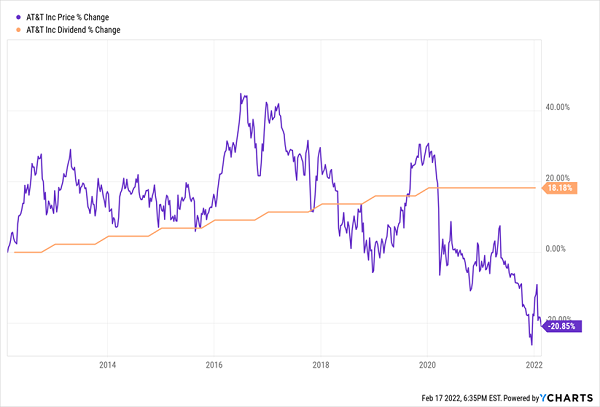

AT&T Inc. (NYSE: T) is a prime example. It’s yielded north of 7% for years now, and I regularly get questions from readers wondering if they should buy it. Not a chance, because that high yield masks the fact that AT&T has been a dividend dud for years because its payout hikes were fake smiles.

Over the past decade, its dividend has barely inched ahead every 12 months — just enough for the stock to hang on to its membership in the Dividend Aristocrats! We’ve talked before about how a rising dividend has a “magnetic” pull on share prices, and you can see that below, with the dividend’s anemic gains pacing the stock (slightly!) higher, until COVID-19 hit.

AT&T’s Weak “Dividend Magnet” Shuts Down

As you can see, the stock was just climbing back toward the payout when, in May 2021, management cut the legs out from under it when it said it would reduce the dividend as part of the spinoff of its WarnerMedia subsidiary, which will merge with Discovery Communications Inc. (Nasdaq: DSCA).

The worst part was that AT&T was unclear on the size and timing of the cut. Then, a few weeks ago, it announced that it would be deep — 47%, to be precise, leaving the stock with a 4.7% forward yield. (The cut hasn’t shown up on screeners yet, so it’s not on the chart above, but as you can see, the stock price anticipated it.)

Truth is, even this sickly payout may not last, given AT&T’s $178 billion in long-term debt, which exceeds its value as a public company ($170 billion). It will get $43 billion in cash and other considerations from the spinoff, but even if it puts all of that on its debt, it would be indebted to the tune of around 80% of its market value. If you’re still sitting on this one, it’s beyond time to let it go.

A Power Provider With a Flickering Payout

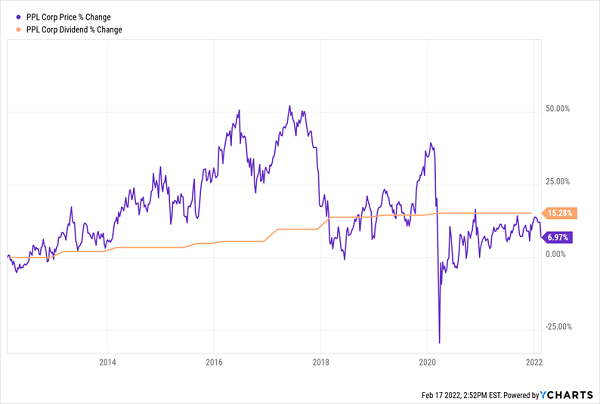

On the surface, PPL Corp. (NYSE: PPL) looks like a dividend investor’s dream: It owns four regulated utilities serving some 2.5 million customers in Pennsylvania and Kentucky. Its shares yield a high 5.8%.

Of course, utilities are a safe haven when the economy gets rocky, but you can’t just buy any utility, and PPL is an example of one that isn’t the best choice. As you can see below, the payout is stalled, having risen just 15% in the last decade.

PPL’s Underpowered Dividend Fails to Ignite Its Stock

When a dividend stalls or goes flat, it can hold a stock back — which is our Dividend Magnet working in reverse! You can see that above: Each time the stock gets ahead of PPL’s low-voltage payout growth, it gets hauled back down. The result? A mere 7% price gain for the stock over the last five years!

In March, the company plans to close its purchase of privately held Narragansett Electric Company of Rhode Island from UK-based National Grid PLC (NYSE: NGG) for $3.8 billion. It’s a big purchase for PPL, whose market cap is $21.2 billion. However, it sold its UK-based Western Power Distribution subsidiary to National Grid for $10.4 billion last June and plans to use some of that cash to fund the deal.

Once the purchase is firm, PPL says it will adjust its dividend to target a payout ratio of 60% to 65% of earnings per share (EPS). It’s unclear what that would mean for the payout, given that the company has generated negative EPS over the last 12 months, including one-time items. Adjusted for special items, PPL has earned $1.42 a share in that time, well below the $1.66 it’s paid in dividends. That lack of clarity, as we saw with AT&T, is a good sign it’s time to sell.

Kraft Heinz Co.: Use This Bounce to Check Out

Pre-pandemic, Kraft Heinz Co. (Nasdaq: KHC), with its packaged-food brands (such as Oscar Meyer, Velveeta and Jell-O) was out of step with consumers, who were keener on fresh fare. That trend reversed during the lockdowns, when canned and frozen foods were all the rage. Plus, KHC’s products had no competition from restaurant food.

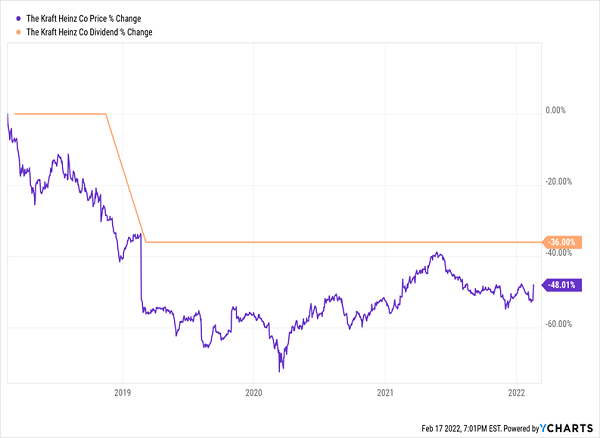

But now, with omicron fading, the trend is flipping back — and threatening to end diners’ brief (re) flirtation with KHC’s products. That’s bad news for shareholders because KHC’s above-average 4.4% dividend hides the fact that it already slashed its payout by 36% in 2018, with the share price falling in lockstep.

KHC’s Dividend Tracks Its Share Price (the Wrong Way)

Now the current is turning against the company again, and its cash dividend payout ratio (or the percentage of the last 12 months of free cash flow paid out as dividends) is rising: It’s now at 61%, compared to 40% at the end of the first quarter of 2021. With that in mind, I’m concerned that even this lighter payout will be too much for KHC to bear, especially as inflation drives up its input costs.

Here’s the good news: Investors have overlooked this in their panic over rate hikes and the Ukraine crisis and have piled into what they view as a “safe” stock, driving KHC up 4% this year as of this writing. That gives you a nice bounce to sell into if you still own it.

To learn more about generating monthly dividends as high as 8%, click here.