Every earnings season, Wall Street latches onto a defining theme. Last quarter, that theme was the Middle East.

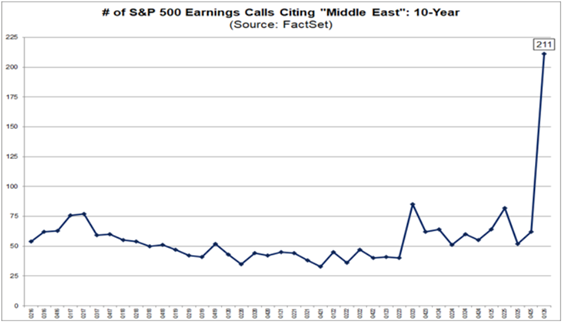

According to FactSet data, 211 S&P 500 Index companies mentioned the Middle East on their earnings calls in first-quarter 2026 — a number that doesn’t just stand out, it breaks the chart.

To put that in context, the count rarely cracked 85 over the previous 10 years. And for most of that stretch, it hovered quietly in the 40s and 50s. What you’re looking at below isn’t a gradual uptick. It’s a wall.

That kind of spike tells you something important — not just about the Middle East, but about how corporate America is thinking right now.

When executives suddenly flood their carefully scripted quarterly calls with a geographic reference they’d largely ignored for years, they’re signaling something: risk is repricing.

Whether it’s supply-chain exposure, energy costs, defense contracts or just the creeping anxiety of operating in an unstable world, the region has moved from background noise to the forefront of boardrooms across the S&P 500.

So what does it mean for investors heading into next week?

A lot depends on which companies are talking about the Middle East — and why. Some are warning. Some are winning. Below, using a special screener, I’ve broken down potentially “bullish” earnings… and ones that might be in trouble…

“Bullish” Earnings to Watch

These stocks are expected to beat their earnings per share (EPS) from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are six companies that made this week’s list:

If there’s one name I’d bet on to beat the number this week, it’s Costco Wholesale Corp. (COST) — and it’s not particularly close.

Analysts are modeling EPS of $4.98, up from $4.58 in the prior quarter. That’s an 8.7% jump, which sounds like a stretch until you remember that Costco has beaten estimates around 18 of the last 20 quarters.

At some point, that stops being luck and starts being a business model.

The macro setup couldn’t be more tailor-made for the retail behemoth right now.

Tariff anxiety has consumers bulk-buying staples, and nobody wins that trade like Costco. Its higher-income members — the ones who were supposed to be immune to trading down — are showing up at the warehouse anyway, because in an uncertain economy, value wins across the board.

Add in membership renewal rates north of 92%, and you’ve got a revenue base that’s essentially pre-sold before they open the doors on day one of the quarter.

The detail I’d watch on the call: gas station margins.

Fuel is a line item that analysts consistently undermodel, and it has a way of quietly padding the number when conditions are right.

If management also signals any acceleration in new warehouse openings, that’s a longer-term catalyst that the market tends to reward immediately.

The overall “Neutral” rating on Adam’s Green Zone Power Ratings system makes COST look like the least exciting name on my screener this week.

Sometimes boring is exactly right.

Now, let’s shift gears to those “bearish” earnings next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are 10 companies that passed this screen:

Look at this list long enough and a pattern jumps out: eight of the 10 names reporting next week are retailers, and most of them sell clothes.

That’s not a coincidence. It’s a dispatch from an American consumer who is increasingly stretched, increasingly online and increasingly done paying full price for a mall experience.

It also doesn’t help that the quarter after the holiday shopping season is typically when sales are at their lowest.

The macro backdrop explains a lot of it. Tariffs have hit apparel importers hard, and most of these brands source heavily from Asia.

That cost pressure is either being passed on to consumers — who are already pulling back on discretionary spending — or absorbed into margins. Neither option is a good look on an earnings call.

Capri Holdings Ltd. (CPRI) deserves a specific callout. This is the parent of Michael Kors, Versace and Jimmy Choo — brands that were supposed to be insulated from mass-market pressure.

An EPS estimate of $0.12, down from a prior $0.96, suggests the affordable-luxury middle is softening, a trend that should worry anyone with aspirational retail exposure.

The calls themselves may matter less than the guidance next week. What these companies say about tariff strategy, inventory levels and back-half consumer traffic will likely move stocks more than whether they beat or miss by a few pennies.

Any way you slice it, another interesting week of earnings is close at hand.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets