Recent full-year earnings figures released by automaker Stellantis N.V. (NYSE: STLA) suggest the company demonstrated respectable durability during an economically challenging 2023 for global auto manufacturers.

Two notable metrics affirm investor confidence in Stellantis right now:

Record $204 Billion Net Revenue Driven by Vehicle Delivery Growth

Most critically, Stellantis increased overall 2023 net revenues to $204 billion — an all-time high.

The 6% expansion versus last year was fueled partially by a 7% jump in total vehicles sold, reaching 6.4 million units.

Outpacing initial estimates proves demand held firmer than expected. Higher volumes converted to record monetary returns are critical.

The company reported a net profit of $20 billion and industrial free cash flows of $13.8 billion — a 19% year-over-year increase.

Doubling down, Stellantis saw growth for Jeep SUVs and commercial vans, which offset weakness in European sedan purchases — signaling management can pivot smarter if specific markets or products weaken temporarily.

Adaptivity ensures stability when unpredictability looms.

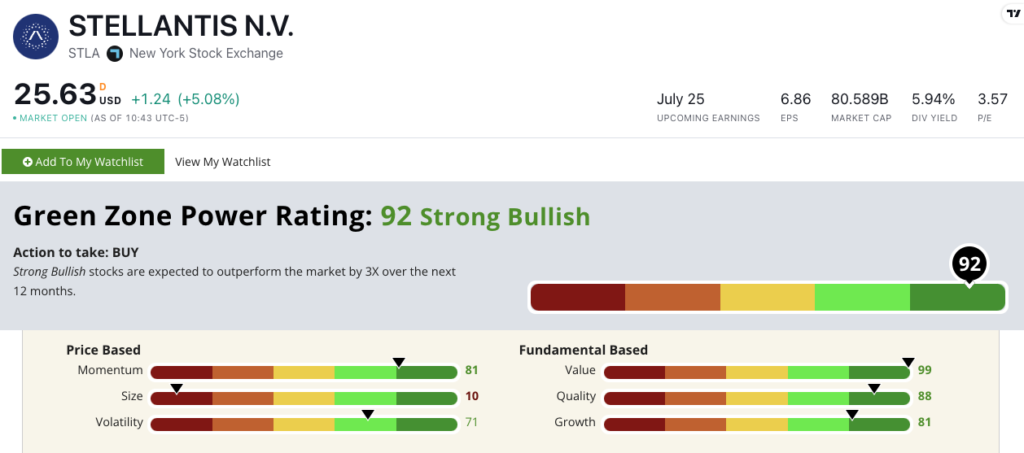

Bullish Stock Rating Backed by Quality Metrics and Reasonable Valuation

Adam O’Dell’s proprietary Green Zone Power Ratings system scores STLV at 92 out of 100 overall.

This means we are “Strong Bullish” on the stock and expect it to outperform the broader market by 3X over the next 12 months.

Stellantis N.V. Green Zone Power Rating in February 2024.

Stellantis’ overall rating is highlighted by strong Quality (96) and Value (91). This externally validates in-house profitability plus affordable pricing multiples that insulate against downside risk if headwinds linger.

Compared to rivals trading at higher valuation ratios, Stellantis shows measurable upside safety.

On Quality, Stellantis maintains better-than-average returns on assets, equity and investments. Its return on equity is 27.3% compared to the consumer vehicle industry average of minus-9.3%.

The company’s gross margin is 24.2%, while its competitors are averaging 15.4%.

For Value, STLA trades with a price-to-earnings ratio of 3.7, while its competitors average a ratio of 19.8 — meaning Stellantis trades with a P/E ratio nearly six times less than its peer average.

The company’s price-to-sales ratio is 0.4 compared to its peer average of 2.3.

Bottom line: Encouraging full-year figures showcase Stellantis entering 2024 in pole position operationally and financially, buffered against economic turmoil.

However, sustaining momentum via competitive electric vehicle adoption and manufacturing improvement remains vital to fend off born-electric threats in the long term.