“US and Israeli forces pressed ahead with attacks on Iran while the Islamic Republic launched missiles across the Persian Gulf, sending oil prices higher once again amid no sign of an imminent peace deal.”

The Bloomberg quote above could have been published any day since the beginning of March. Unfortunately, it was printed this morning.

The Iran war is raging on with no immediate end in sight.

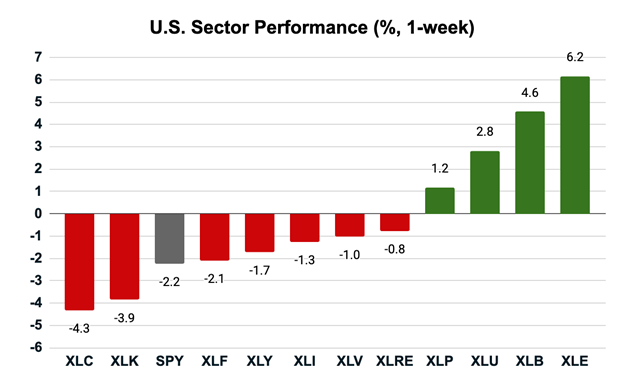

Care to guess what the best-performing sector was last week?

Sure enough, it was energy.

Again.

The State Street Energy Select Sector SPDR ETF (XLE) blasted higher by 6.2%, continuing its winning streak. And the inflation-sensitive State Street Materials Select Sector SPDR ETF (XLB) rose 4.6%.

They were joined by the State Street Utilities Select Sector SPDR ETF (XLU) and the State Street Consumer Staples Select Sector SPDR ETF (XLP) as the only sectors to finish the week positive.

We know why energy stocks are rocketing higher. With Middle Eastern oil largely offline right now, American energy companies have a really nice profit runway in front of them.

I’m more interested in one particular combination of profitable sectors last week… and what that combination implies.

An Unfortunate Combination

It’s not unusual to see energy and materials rising together. Both have historically performed well during times of rising inflation, and energy and broader commodity bull markets often overlap.

But now, we have utilities and consumer staples in the mix…

These are traditionally defensive sectors that tend to outperform during recessions. They tend to thrive in deflationary markets, not inflationary ones.

So, how do we explain this apparent contradiction?

It seems that the market is pricing in stagflation… that ghoul from the 1970s that combines the worst of all possible worlds: high inflation and stalling growth.

One week doesn’t make a trend, of course, and it is a mistake to read too deeply into this. So, we’ll do what we always do: let the data guide us as we follow my system.

But right now, that means staying alert for more signs that stagflation could become a reality.

What About Tech?

We also need to talk about tech…

The two worst-performing sectors last week were communications and technology, which overlap. The State Street Communications Select Sector SPDR ETF (XLC) and the State Street Technology Select Sector SPDR ETF (XLK) were down 4.3% and 3.9%, respectively.

It’s no coincidence that the S&P 500 Index joined them at the bottom of the list. The S&P 500 is completely overloaded with tech and communications names. Together, they make up 43% of the index.

Energy and materials together make up less than 6% of the index.

What does this mean?

It means that energy and materials are not capable of pulling the S&P 500 higher. They’re just too small. NVIDIA (NVDA) and Apple (AAPL) are each, by themselves, larger than the entire combined weighting of the energy and materials sectors.

So, as goes tech… so goes the S&P 500.

If you’re an active investor, that’s not a problem. You can invest in the sectors that are outperforming and steer clear of the ones dragging the index down. But it’s not quite that simple for the millions of investors who depend on S&P 500 index funds in their 401 (k) plans…

Yes, the lousy performance of tech and communications is a major problem. The S&P 500 can’t get its mojo back until those sectors find their footing.

Key Insights:

- Energy continues its dominance, leading the pack for another week.

- The market’s action last week suggests that investors are pricing in stagflation.

- Until tech finds its footing, the S&P 500 is going to struggle.

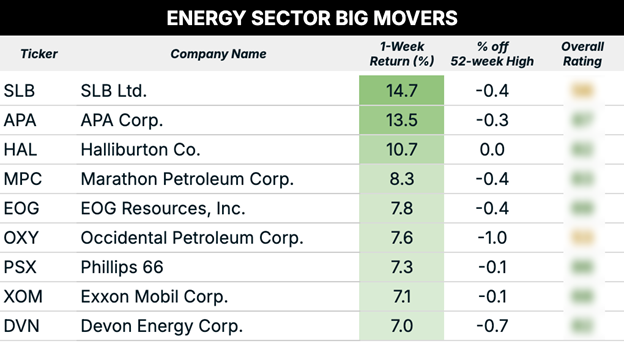

Energy Reigns Supreme

For the fourth week in a row, energy finished on top.

I ran my customary screen of the biggest movers in the energy sector that were also still within 10% of their 52-week highs last week. The idea is to look for solid, market-leading stocks that are getting stronger.

Here’s what I came up with:

We see several holdovers from last week.

Oilfield servicers SLB Ltd (SLB) and Halliburton (HAL), domestic drillers APA Corp (APA), Occidental Petroleum (OXY) and Devon Energy (DVN) all made the list last week.

Moreover, refiners Marathon Petroleum (MPC) and Phillips 66 (PSX) have made appearances throughout March, as has ExxonMobil (XOM).

All of these stocks continue to rocket higher… and all but Occidental and SLB rate as “Bullish” or “Strong Bullish” on my Green Zone Power Ratings system.

I also want to emphasize that the energy sector was flashing “Bullish” on my system months before bombs started dropping in Iran. The war obviously accelerates the trend, but the trend was well in place long before the conflict started.

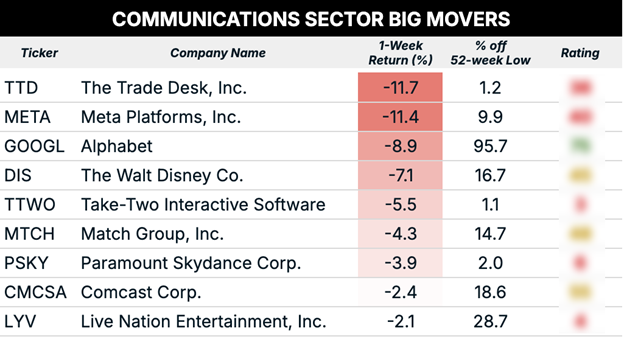

What Happened in Communications?

There is no mystery as to what happened in the communications sector last week.

Two companies – Meta Platforms (META) and Alphabet (GOOGL) – account for nearly 40% of the sector by market cap. And both of those companies recently lost lawsuits from users who claimed that their products were addictive… and that social media addiction caused them serious harm.

Meta was down about 11% last week, and Alphabet about 9%.

Companies that depend on ad spending on social media also took a hit. For instance, The Trade Desk (TTD) was down about 12% last week.

The case was reminiscent of the tobacco lawsuits of the 1990s, which ended with major restrictions on how tobacco products were marketed, along with required safety labels and a large monetary settlement.

Is this the future for social media?

It’s too early to say. But the loss in court was enough to spook investors. For what it’s worth, Alphabet – which is less directly exposed to social media – rates as “Bullish” on my Green Zone Power Ratings system, while Meta – which depends almost entirely on it – rates as “Bearish.”

What about the rest of the sector?

I ran my customary screen of the sector’s biggest losers for the week that are still trading within 10% of their 52-week lows. The idea is to find beaten-down gems that look poised to recover.

Well, the pickings were slim. Despite the drop in prices, most were still well above their 52-week lows, so I had to relax the criteria.

There’s not a lot to see here…

There’s only one “Bullish” rated stock on the list – Alphabet. And given that the stock is still almost 96% above its 52-week low, it’s hard to say we’re buying a dip here.

Still, Alphabet is one of the key players in the AI revolution… so any lawsuit-related share price declines could be seen as a good entry point.

To good profits,

Adam O’Dell

Editor, What My System Says Today