Today I’m going to show you how one lucky group of investors nailed a once-in-a-lifetime shot at a huge, tax-free dividend stream and a quick 18% gain, too.

Well, not exactly “once-in-a-lifetime.” Because this opportunity is still waiting for you today— you just need to know how to tap it.

In a moment, I’ll give you the goods (including a name and ticker) on a closed-end fund (CEF) to target now. It hands you a 4.2% dividend you likely won’t have to pay a penny of federal tax on (and your payout could be exempt from state taxes, as well).

To cut to the chase, thanks to its lucrative tax breaks, this fund’s 4.2% payout could be worth 7% or more to you today, depending on your tax bracket.

Giving Uncle Sam the Slip

How does this fund manage to pull off a tax-free dividend stream?

Simple: It holds “boring” municipal bonds — issued by local governments to fund infrastructure projects. Most Americans don’t pay any tax on munis’ dividends, and CEFs that own munis were at the heart of the 18-plus percent gains (and big cash payouts) our savvy contrarians bagged in the last year.

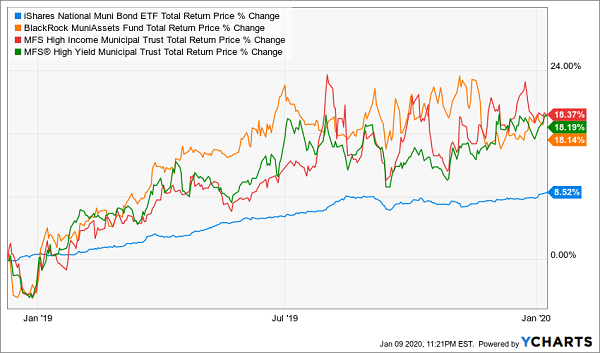

To see how they did it, let’s rewind to December 2018, when muni CEFs traded at absurd discounts to net asset value (NAV, or the per-share value of their underlying portfolios), I wrote back then that we were facing a “time-limited shot at income and gains” that would send munis soaring in 2019.

I then spotlighted three strong muni-bond funds, the BlackRock MuniAssets Fund (MUA), the MFS High Income Municipal Trust (CXE) and the MFS High Yield Municipal Trust (CMU), because they were heavily discounted and full of high-yielding, high-quality bonds. Here’s how they’ve performed since, against the benchmark iShares National Muni Bond ETF (MUB), in blue.

Soaring Past the Index

These are huge gains for this “sleep-well-at-night” asset class, and they more than doubled the return on the muni-bond benchmark ETF. The reason why: those discounts I mentioned a second ago. These three funds traded at an average 8.5% discount to net asset value (NAV, or the value of their underlying portfolios) a little more than a year ago, giving them all plenty of room to rise.

Our Second-Level Analysis of the Muni Market

Will the trend continue? My answer is yes, despite the press dwelling on overblown worries like cyberattacks on hospitals, the costs of which, some pundits claim, could lead them to default on their debts.

Truth is, these overhyped media reports don’t hold up to scrutiny. Erie County Medical Center was the hardest hit, with a $10 million bill for a recent cyberattack, but ECMC also earns $647 million in revenue, making that attack worth just 1.5% of revenue. Yes, it’s an unfortunate surprise cost, but it’s far from enough to push the hospital into default.

Further, with employment strong and tax revenue growing in most of America, there’s a solid foundation for many munis to see credit upgrades that will make their bonds more valuable.

‘One of the Most Discounted Muni-Bond CEFs Out There’

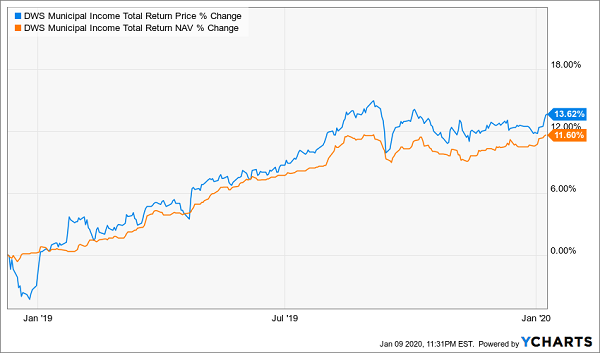

This all means that big, tax-free income streams are still available at a discount, if you know where to look. One example is the DWS Municipal Income Trust (KTF), one of the most discounted muni-bond CEFs out there, trading at 9% below its NAV, despite its 4.2% tax-free yield (which, again, could be worth 7% or more to you, depending on your tax bracket):

Strong Gains, but Not Too Strong

What’s compelling about KTF is that its total price return over the last year has only slightly exceeded its total NAV return. The average discount for muni bonds shrank considerably in 2019, due to the feeding frenzy of market demand, but KTF didn’t get as much attention. That makes it a rare undervalued muni-bond fund in a strong muni-bond market — a nice setup for a contrarian investor to swoop in and get a strong passive income stream with upside potential.

To learn more about generating monthly dividends as high as 8%, click here.