I don’t own a home.

The reason may not make sense to you, but it did to me when I made it.

In my past life as a journalist, I was never “home” for very long. I had road trips for sports or long hours doing extensive research for investigative pieces.

I didn’t spend a lot of time at home or in one place, so the thought of buying a home never really crossed my mind.

You might think I regret my decision, but I don’t … especially in today’s world.

Let me explain.

The Interest Rate Quandary

A few days ago, I was in Mike Carr’s daily trade room and we started talking about mortgage rates — the interest charged on a home loan.

The average rate on a 30-year fixed mortgage is just below 8% if you have good credit … and above 8% if you don’t.

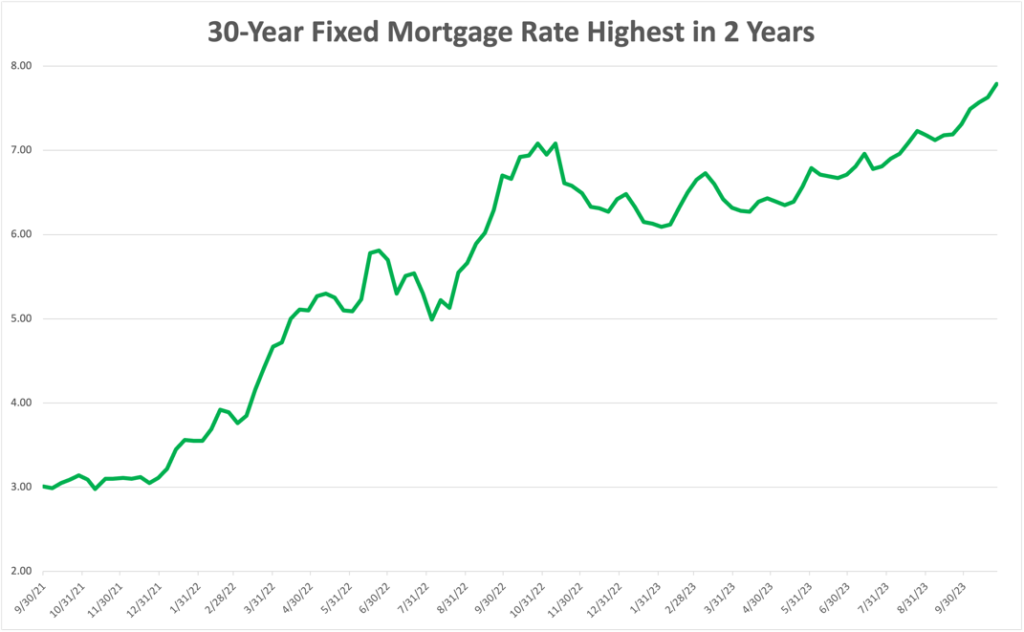

That average rate has risen higher for the last two years:

Source: Freddie Mac.

After years of the average mortgage rate fluctuating around 3%, homebuyers are looking at the highest interest rate since the turn of the century — close to 8%.

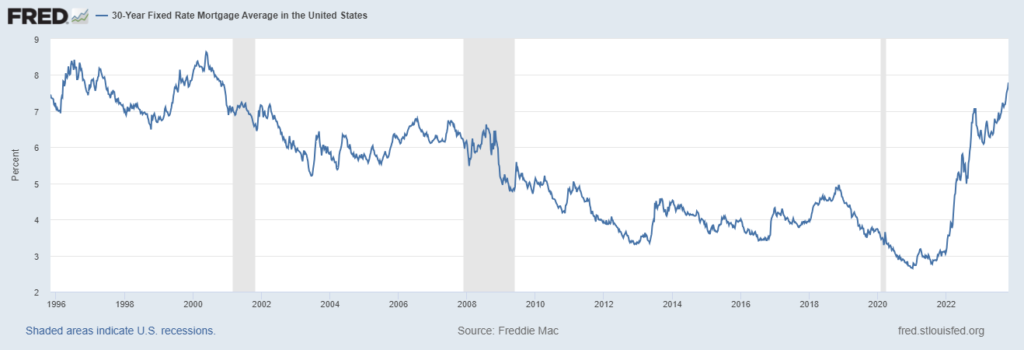

Highest 30-Year Mortgage Rate Since 2000

Source: Federal Reserve.

That means, for every $1,000 you borrow, you will pay an extra $80 in interest to the bank.

In real numbers, assuming you are buying a $300,000 home with 20% down at 3.25% interest (the average interest two years ago), your monthly payment would be $1,445, including taxes and fees.

The same $300,000 home with 20% down at 8% interest brings that monthly payment up to $2,162.

It’s a significant difference in monthly payments — $717 a month, to be exact.

That’s a big reason why I — and millions of other Americans — are not buying homes right now.

Even if I did own a home and wanted to buy a new one, the timing is awful because I would pay significantly more for a new home than what I’m paying for now.

It’s one of the reasons why the housing market is struggling right now … and why there will be more pain to come.

Housing Market Woes to Continue

This week, the Federal Open Market Committee held the fed fund rates as expected.

So the obvious question … especially for prospective homebuyers … is: Why are rates still climbing higher?

In March 2022, the Federal Reserve started its interest rate hike spree in hopes of tamping down inflation.

That made it more expensive for banks to borrow.

And as every business does, banks pass those costs along to consumers in the form of higher interest rates for every type of loan.

As the Fed continues to hold rates higher for longer, bank costs continue to rise, thus rates continue to climb.

So even though the Fed held its fund rates steady, bank costs will continue to grow and push loan rates — such as mortgages — higher.

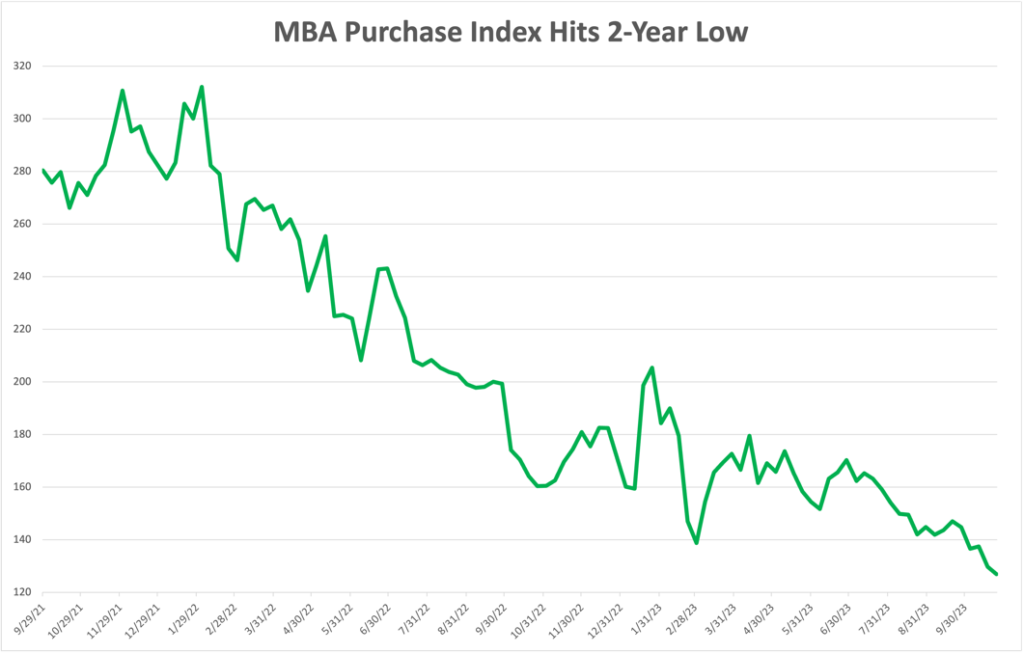

And that means new mortgage applications have hit a wall:

Source: Investing.com.

The Mortgage Bankers Association Purchase Index tracks the mortgage applications on single-family homes in the U.S.

It hit a two-year low at the end of October. The index is down more than 60% from its 2021 high and shows no signs of slowing down.

People aren’t buying homes as much as before due to higher prices, higher interest rates and a lack of supply.

Bottom line: As rates go higher and applications dwindle, the pain in the U.S. housing market is only going to get worse.

For many owners and non-owners alike, you aren’t likely to buy because it’s too expensive.

If you do own a home and are looking for a change of scenery, you aren’t likely to buy because … well … it’s too expensive. You’re better off just staying where you are and paying less.

With the Fed’s “higher for longer” rate mantra, mortgage rates are only going to go up…

It’s likely to only get worse for the U.S. housing market before it gets better.

Tomorrow: How Housing Stocks Stack Up

Managing Editor Chad Stone is going to run some of the most popular housing stocks through our proprietary Green Zone Power Ratings system to see if any are investable as interest rates remain elevated.

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets