Donald Trump has been fast and furious in his implementation of new policies and agendas — doing more in his first year than most presidents do in an entire term.

As a result, it’s not always easy to pick out the impact of these policies … how effective they might really be … and how much money they’re saving for the American taxpayer.

So today, I wanted to zero in on a single situation where Trump’s policies are having a massive impact on America’s economy. Hit today’s video update for the full story:

Video transcript:

Welcome to Moneyball Economics, I’m Andrew Zatlin.

And if you are in the path of winter Storm Fern, hope you get through this with no problems.

I myself, I’m sitting here in Charlotte, North Carolina and I have no idea what to expect. I mean, we’re not Michigan, we’re not built for ice storms. I’m hoping no tree damage, no burst pipes, nothing like that. So, wish me luck!

In today’s episode of Moneyball Economics, I want to talk about something that I’ve uncovered.

It, to me, changes my entire thinking about what to expect with inflation in 2026, and while inflation sounds kind of whatever, understand that everything that happens with inflation will dictate what happens with interest rates and company profit margins, which affects stock prices.

Right now, big picture, we know that the economy’s firming up. Fourth quarter expectations for the GDP are 10% year-over-year. We are going into a place where business conditions are improving and we know that Trump is going to try to run the economy hot.

All these things point to a fed maybe not willing to cut interest rates primarily because all these things will drive up inflation. However, what I’ve uncovered suggests that maybe inflation’s going to be more tamed than the markets are going to expect. So that’s an interesting opportunity…

If inflation is more tame, then profit growth is stronger. Let me share with you what I’ve uncovered and what some of the implications are. It started off with me looking at payroll growth.

The reason I was looking at payroll growth is I was doing a thought experiment. Every time we’ve had an economic slowdown, every time revenue growth has slowed recessions and so forth, companies take about two years to lay off workers, negative payroll growth, not higher, still negative payroll growth, and then finally start to hire two years. 1990 was about 17 months. 2001, it was 20 something months, 27 months I think 2007, 29 months.

I think you get the idea … about two years.

So I was looking at our payrolls trying to uncover when our payrolls are going to start to move up again because another reason why the fed might delay interest rate cuts is payrolls are firming up. And so I’m trying to look at that part of the inflection. Well, as I looked at the payroll data, I noticed something very interesting.

Now remember, we are not in a recession even though we’ve had all these job cuts. It’s not a recession, it’s not a traditional economic cyclical downturn. This is really the tail end of what I call the COVID cycle where we overhired because of COVID.

And then in 2023, folks realized corporate profits were getting hit as the economy normalized and that growth was just not there anymore. And so they looked at their staffing and they had to rightsize staffing and spending to realign with what is really normal economic growth, 3% plus or minus.

It was painful to get through that. And as I looked at payrolls, I said, “huh, companies really didn’t really do much.” They tapped the brakes. We went from say 2023, a little over 3% payroll growth year-over-year, pretty big, not as big as it was in the previous COVID years, but 2023 still good. And they started tapping the brakes and it went from 3% to two to 1% and so forth.

Except what I did is I started digging into the data and I noticed last year there really wasn’t any payroll growth. I mean, in fact, most sectors, not only were they fired, they weren’t hiring. There was no payroll growth with one notable exception, and that was healthcare.

Last year, healthcare grew almost 1 million, and it’s been growing 1 million year in year out for three years. I thought that was very interesting. On the one hand, healthcare growing and growing a lot, healthcare is growing 4% year-over-year, much more than the population growth.

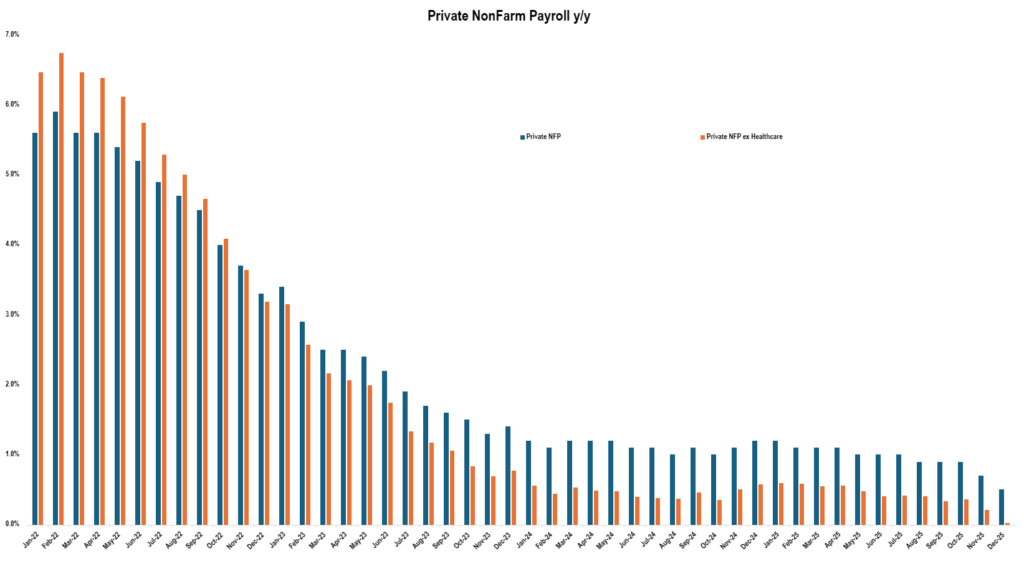

But when I look at other sectors, basically the rest of the economy, they didn’t tap the brakes. Take a look at this.

They slammed the brakes.

See folks, when we look at the headline number of payrolls, that four to 3% down to kind of sort of one and 2%, that’s not the story. You strip out healthcare, and we went from that four, that three percent-ish level almost immediately down below 1% to half a percent year-over-year payroll growth. What I’m saying is for two years, 20, 24 and 2025 companies stopped hiring.

So when I compare that to previous recessions, I go, aha, we’re at that two-year point. It’s likely payrolls are going to start to go up again.

And indeed, let’s face it, business conditions are very pro-growth as we come into this new year. So that’s one way to look at it as we might be seeing firming payrolls, the Fed might be reluctant to cut, but I started to notice this issue of why did healthcare resist the other trend?

And this is interesting off on the side because it speaks to why inflation might be more tame coming down the pipeline. Healthcare. Look, it’s a business they’re going to hire if the money’s coming in and a million people, 4% growth year-over-year in 2024 versus, well, according to the Census Bureau population growth of less than 1%, not even what was going on there? Who’s driving up this demand for healthcare services and who’s paying for it after all?

If our workforce was relatively flat, if our population was relatively flat, then the amount of medical treatments was relatively flat and so demand wouldn’t be there. And that’s when I had my aha moment.

See, the Census Bureau and the Bureau of Labor Services ignores the 12 million undocumented immigrants who came in during that time. If you take those 12 million people and you fold ’em back into the total population estimate, you find that our population grew about 4%.

In other words, healthcare growth was reflecting population growth. And this is where I think the inflation story needs to be considered. Over the past year, we have seen estimates are about two, two and a half million people leave the country, maybe another million leave the country this year. Bottom line, we’ve seen healthcare hiring last year come down a little bit. So what we’re seeing is some interesting changes in what’s going on under the surface.

What we’re actually seeing though, is that undocumented immigrants contributed to payroll growth contributed to consumption here in the United States, and they are leaving. And so we can expect healthcare, which was the single driver of payrolls last year, healthcare is going to add a lot fewer payrolls going forward. Not because we have fewer people coming into the country, which is true, but because we have more people leaving the country.

So it’s a double hit, and it makes me think it’s not just happening in healthcare. It’s everywhere. Housing, food, you take a few million people out of this economy and guess what? Spending goes down. You have a major deflationary pressure underway at a time when the economy’s going to be heated up. So we have these offsetting, potentially offsetting trends.

And so I think inflation is going to be pulled back a little bit because of the deportation and self-deportation, undocumented immigrants. So let’s see how this plays out this year, because I don’t think the market has factored this in. And that’s an opportunity, a positive opportunity for the stock and bond markets.

We’re in it to win it, folks.

Zatlin out.

Andrew Zatlin

Editor, Moneyball Economics