Stop me if you have read this before: Microsoft reported another blowout quarter on the back of stronger-than-expected sales from its cloud computing businesses.

We’ve all heard that before, and we’ll hear it again.

The Redmond, Wash. software giant (Nasdaq: MSFT) last week posted $36.9 billion in second-quarter revenue, up 14% year-over-year. Profits surged 38% to $11.6 billion, according to a corporate statement.

Microsoft is a huge company with annual sales of $125 billion. Getting the needle to move on a number that large is nearly impossible, say the skeptics. However, this line of thinking ignores the dynamism of public cloud computing. It also downplays the importance of scale.

Microsoft is growing quickly because it’s big.

The company has the largest network of state-of-the-art data centers. These data farms are strategically located all over the world to reduce latency.

Moreover, Microsoft has legions of engineers well-equipped to ferret out malicious software, while helping enterprises make the jump to public cloud, hybrid cloud and edge computing.

According to a Techcrunch report last November, Salesforce.com (NYSE: CRM) managers pointed to multi-layered security and global scale when they announced the customer relationship management company would move its Marketing Cloud to Microsoft’s platform.

A month later, the Pentagon awarded Microsoft a 10 year, $10 billion contract to supply cloud services for its Joint Enterprise Defense Infrastructure. In the end, the JEDI contract was winnowed down to the largest firms, Microsoft and Amazon Web Services, a division of Amazon.com (Nasdaq: AMZN).

This is good news for Microsoft. The better news is the corporate world is still in the early stages of the move to cloud-based systems.

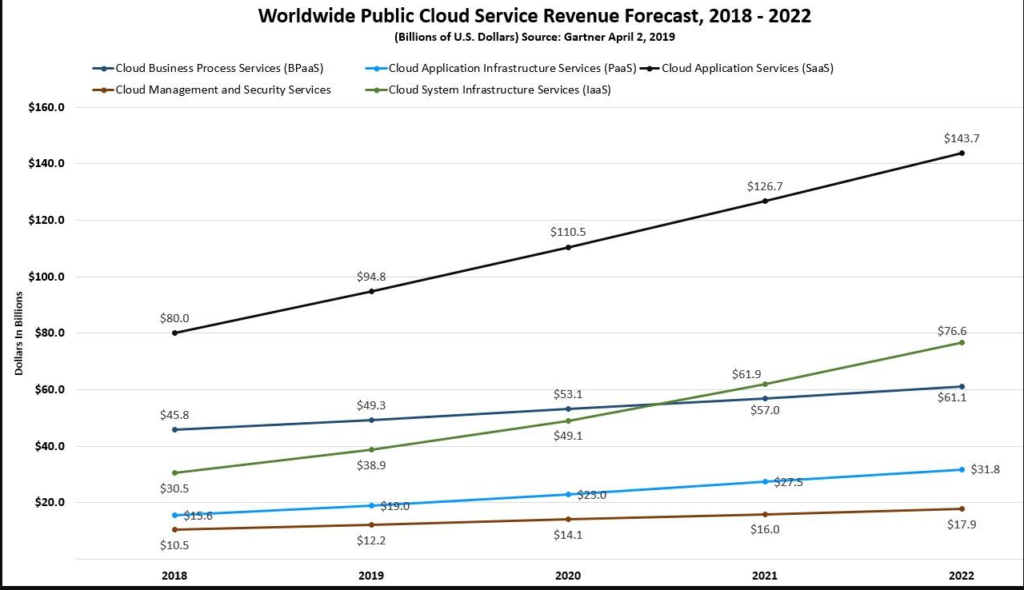

Analysts at Gartner noted in April 2019 that the size and growth of the cloud services market is growing three times the overall rate of IT services. The firm believes that many enterprises have begun to shift from cloud-first IT models to cloud-only.

The size of that marketplace is expected to reach $331 billion by 2022, up from only $182 billion in 2018.

Source: Gartner

Microsoft is winning that transition. Its cloud business, which includes Azure Intelligent Cloud and the Office 365 productivity suite, saw sales shoot 39% higher, to $12.5 billion during the second quarter.

While the company doesn’t break out exact numbers for Azure, managers say revenues at the unit increased 62% year-over-year.

A big part of Microsoft’s success is staking out leadership positions in the platforms of the future. I have written at length about its efforts in blockchain, Internet of Things and connected cars.

The company began working with automakers in 2015 to set standards for networked vehicles. Renault Nissan became the first to join the Azure connected car platform in 2017. Volkswagen signed in October 2018. Volvo, BMW, Toyota and Ford followed.

Boston Consulting Group estimates the market for in-vehicle connectivity will be $159 billion by 2020. The cloud solutions marketplace alone is expected to reach $66 billion by 2022.

Under CEO Satya Nadella, Microsoft is succeeding by being the vendor of choice in the corporate world because its business is large, and likely to get much larger. Scale provides a level of comfort that should not be underestimated.

It’s why Wednesday’s financial results, impressive as they may be, are likely only the beginning of what is possible at Microsoft.

Shares trade at 33.6x forward earnings. The market capitalization is $1.28 trillion. While this may not seem cheap, it is given the outlook.

Investors are underestimating both the size of the addressable market and how much Microsoft will ultimately claim.

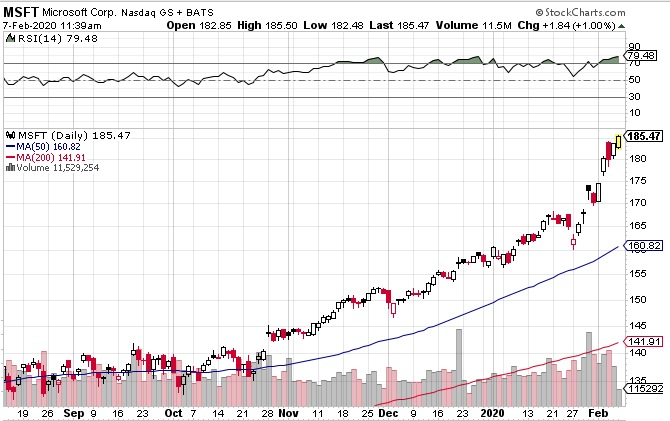

Shares recently traded at $185.29. Savvy investors should use any significant weakness to buy.

Best wishes,

Jon D. Markman

P.S. Tomorrow, Tuesday, Feb. 11 at 2 p.m. Eastern, my colleague Sean Brodrick will be hosting an online training event, Gold Stock 10-Baggers for 2020.

He sees three good reasons for gold to surge from $1,600 to $3,000 and beyond … BEFORE year-end. In this event, he’ll provide his full forecast, PLUS explain how his proven Gold X Indicator can help you pull in the profits. Click here to tune in.