Historically, for whatever reason, stocks have made most of their gains between November 1 and May 1. (Hence the phrase “sell in May and go away.”)

I won’t bore you with the statistical details because they don’t matter for our purposes. Every year is unique, and we treat each as such. But, for our contrarian edge, it is helpful that the onset of fall provokes fear in the hearts of mainstream investors.

The S&P 500 is acting like it’s about to slip off a cliff. It’s been a year since the market’s last meaningful correction. We’re in the fragile half of the year and, seasonally speaking, September and October tend to be particularly weak.

Heck, just this time last year, the stock market was correcting for the second time in six months. Shouldn’t we be worried that history is repeating itself?

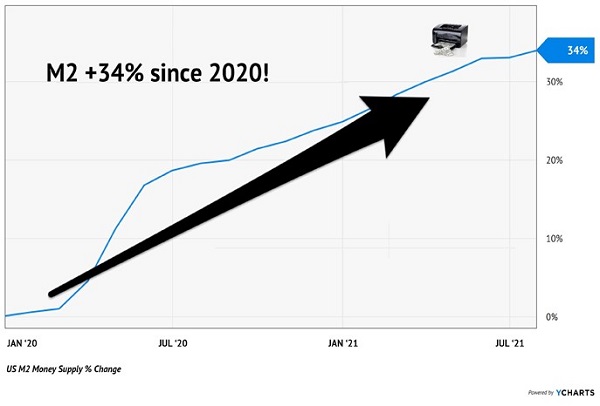

Nope — the Fed’s got our back. Sure, stocks are pricey by traditional measures. But the Federal Reserve has printed a ton of money, increasing the existing M2 money supply by more than one-third since the start of 2020:

Print, Baby, Print

This money is flooding the capital markets and boosting stock and bond prices. It’s the reason why the S&P 500 briefly stumbles, but then quickly gathers and hits new highs in no time.

High-fear sentiment is showing us that this mini-correction is probably close to completion. Which means it’s a good time to start deploying any remaining dry powder into dividend trades. And closed-end funds (CEFs) are a great way to buy this dip.

CEFs stand out from their mutual fund and exchange-traded fund (ETF) brethren in a number of ways, one of them being that CEFs’ share value can (and often does) decouple from the collective value of their holdings. In short, depending on when you’re looking to buy, a closed-end fund could allow you to buy its stock and/or bond holdings at a discount to their value, at their value, or at a premium to their value.

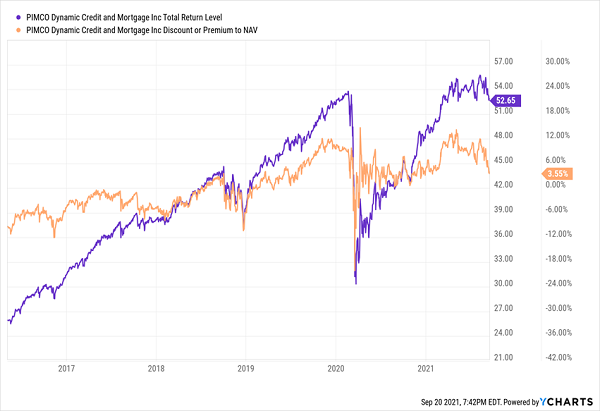

Consider current Contrarian Income Report holding PIMCO Dynamic Credit and Mortgage (NYSE: PCI), which has more than doubled on a total-return basis since we bought it in 2016. Valuation has delivered part of those returns — we bought at a juicy double-digit discount to NAV back then, and that discount has evaporated into a 3%-plus premium today.

The Deeper the Discount, The Better Potential for Bigger Returns

And that’s what you want to be on the watch for today.

Here, I’m going to take a look at three CEFs that are already trading at delicious discounts — and 7% to 8% yields. In theory, you could buy them now and never look back … but a quick panic-sell in the coming weeks could make them all the more enticing.

Royce Micro-Cap Trust (RMT)

Dividend Yield: 7.2%

Discount to NAV: 11.6%

You might not expect to find deep value among some of the market’s smallest stocks, but that is precisely the goal Chuck Royce has strived toward in his 27 years managing Royce Micro-Cap Trust (NYSE: RMT).

What does RMT do, exactly? Chuck himself explains:

“Our task is to scour the large and diverse universe of micro-cap companies for businesses that look mispriced and underappreciated, with the caveat being that they must also have a discernible margin of safety. We are looking for stocks trading at a discount to our estimate of their worth as businesses.”

Royce Micro-Cap’s holdings, such as Par Technology (NYSE: PAR) and Mesa Laboratories (Nasdaq: MLAB), average a mere $811 million in market cap. You’ll be hard-pressed to find many fund managers and index operators alike willing to zoom in this far on the microscope.

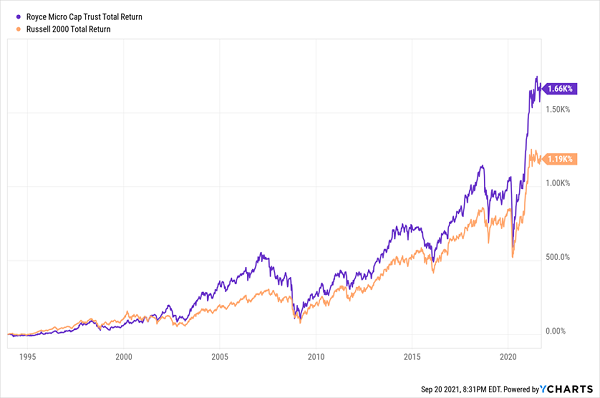

And what a legend! Since inception in December 1993, Chuck has earned 11.3% annually, which comes out to 1.4 percentage points of outperformance against the Russell 2000 — compounding to a massive advantage over time.

How Do You Beat the (Small-Cap) Index? Ask Chuck.

The seeming cherry on the sundae is an 11.6% discount to RMT’s holdings’ net asset value. That’s great — who wouldn’t love to buy a hand-picked set of microcaps for roughly 88 cents on the dollar?

But historical context is important. Royce Micro-Cap has traded at an average 12% discount to NAV over the past five years, meaning the current “sale price” is roughly par for the course.

Virtus AllianzGI Convertible & Income Fund II (NCZ)

Dividend Yield: 8.4%

Discount to NAV: 7.1%

Let’s apply the lesson we just learned from RMT to the Virtus AllianzGI Convertible & Income Fund II (NYSE: NCZ).

This is an aggressive fixed-income play that typically invests about half of its portfolio in U.S. convertible securities, with the rest going toward corporate debt — almost all of which is rated junk. At the moment, only 7% of the portfolio is investment-grade issues. More than half of NCZ’s holdings don’t even have a debt rating.

The convertible angle is interesting. The fund’s marketing materials say “Allianz Global Investors seeks to capture the upside potential of equities with potentially less volatility than a pure stock investment.” However, in an attempt to magnify returns, NCZ employs a hefty amount of leverage — 38% at the moment, via preferred shares. That boosts price returns and yields, but also makes for a twitchier performance.

Well … It’s Better Than Junk Bonds

This volatility means investors are best served by taking advantage of any historically high discounts to NAV.

On its face, NCZ doesn’t appear to be a screaming bargain, trading at a mere 7% discount to the value of its assets. But historically speaking, this is a steal. This Virtus CEF has traded at an average discount of just 1% over the past half-decade.

Kayne Anderson NextGen Energy & Infrastructure (KMF)

Dividend Yield: 7.8%

Discount to NAV: 17.2%

Kayne Anderson NextGen Energy & Infrastructure (NYSE: KMF) might sound like a green energy fund rife with solar companies and EV-charger manufacturers.

The pitch is even more convincing:

Investments focused on “NextGen” Energy Companies and Infrastructure Companies that are meaningfully participating in, or benefitting from, the “Energy Transition” mega trend. Energy Transition is the global shift to a more sustainable mix of lower carbon and renewable energy sources aimed at reducing emissions of carbon dioxide and other greenhouse gasses.

You get a little of that in holdings such as Atlantica Sustainable Infrastructure (Nasdaq: AY) and Brookfield Renewable Corporation (NYSE: BEPC). But KMF actually shares a lot in common with its sister fund, the Kayne Anderson MLP Investment Fund (NYSE: KYN) — namely, it’s full of oil-and-natural-gas master limited partnerships (MLPs) and other high-yielding, traditional-energy firms.

Nothing wrong with that. In theory, a mix of companies that also includes Enterprise Products Partners, LP (NYSE: EPD) and MPLX, LP (NYSE: MPLX) will ensure that KMF can benefit from various energy trends — continued use of crude oil, further adoption of natural gas as a “cleaner” alternative, and even greener energy sources.

In practice, however…

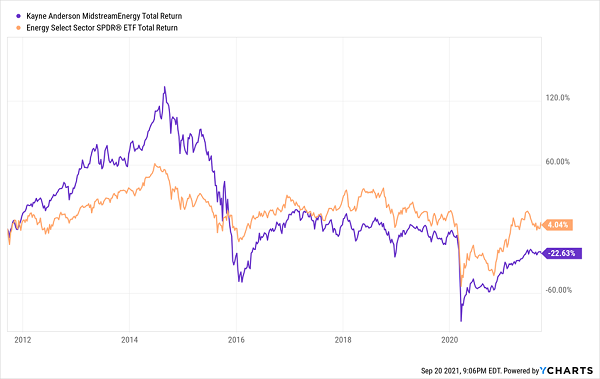

KMF Can’t Even Keep Up With the Energy Index

Healthy 22% debt leverage in a sector with years’ worth of problems has amplified energy’s losses. That means if you are interested in playing a comeback, you should do so when KMF is ideally priced.

It’s arguably a deal right now, at a massive 17% discount that compares well to its 13.6% five-year average.

To learn more about generating monthly dividends as high as 8%, click here.