It’s another earnings Friday here at What My System Says Today.

I was doing some currency research the other day, and something interesting caught my eye.

Over the last 12 months, the U.S. Dollar Index (DXY) is down 9.2%.

This means the dollar is weakening relative to other major world currencies. A weaker dollar makes imports more expensive for Americans, but there is a benefit to this weakening for domestic companies because it makes U.S. exports cheaper and more competitive for foreign buyers. This provides a boost for domestic companies with a strong international footprint.

I wanted to see how this has impacted earnings, and the results were pretty compelling.

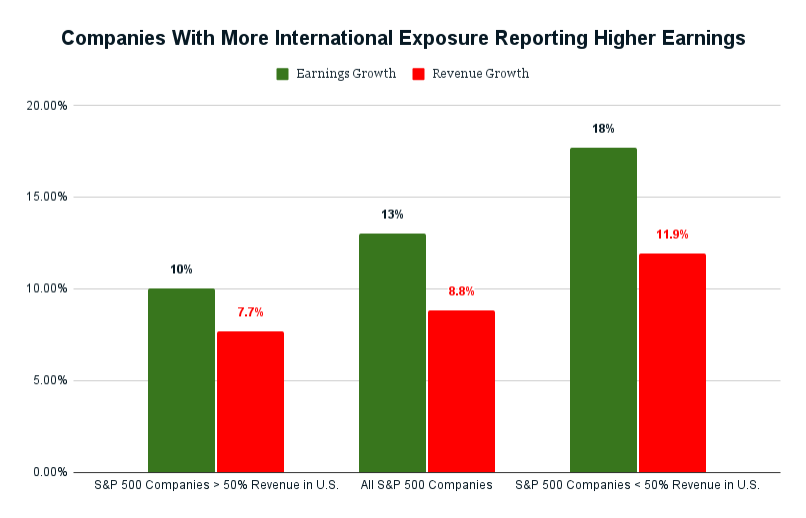

I compared earnings and revenue growth in fourth-quarter 2025 across S&P 500 companies with stronger international exposure, weaker international exposure, and the benchmark as a whole.

What I found was that companies with a limited global presence have grown earnings and revenue by 10% and 7.7%, respectively.

By comparison, those U.S.-based companies on the S&P 500 with more than 50% of revenue coming from outside the country have grown earnings by 18% and revenue by nearly 12%.

On average, all S&P 500 companies have reported a 13% increase in earnings and an 8.8% increase in revenue for the quarter.

This confirms that companies with more exposure to international markets are benefiting from a weaker dollar. That’s something we should keep in mind in the quarters ahead when looking for potential earnings surprises.

Now, let’s examine potentially “bullish” earnings for next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their previous quarter’s earnings per share (EPS). And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are 10 companies that made this week’s list:

In the battle to provide power and infrastructure for AI development, Quanta Services Inc. (PWR) is a significant player.

The company specializes in infrastructure solutions for the electric power, oil and gas, communications, pipeline and energy industries.

Over the past 12 months, PWR has grown 74% compared with the industrials sector’s average of just 38%.

That’s likely a prime reason why analysts are projecting a quarter-over-quarter (QOQ) rise in Quanta’s EPS.

The company has beaten EPS expectations in each of the last five quarters, and its earnings have grown consistently over the last three.

Given the accelerated buildout of AI infrastructure and Quanta’s ability to support it, I see no reason its trend of beating analysts’ estimates will stop now.

Now, let’s look at potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a QOQ decline in earnings.

Here are 10 companies that passed this screen:

Back in July, I mentioned Booking Holdings Inc. (BKNG) and its projected EPS increase of more than $10.

I said the increase was “lofty,” but that the company would beat expectations… which it did.

Now, the company is on the other end of the spectrum, with analysts projecting a near-QOQ halving of Booking’s EPS.

This looks massive because of the previous quarter’s EPS of nearly $85.

A resilient travel market and continued investments in its AI-powered “connected trip” platform should help the company beat the expectation of $48.67 per share.

That’s lower than the previous quarter, but we’ll call it a victory nonetheless.

It should be another very interesting week on the earnings front.

That’s all from me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets