When you read about an investor selling off 15% of shares of one company’s stock, you can’t help but do a doubletake.

That’s usually a sign of major trouble ahead…

Then you realize it was Warren Buffett’s Berkshire Hathaway doing the selling.

After selling 21.1 million shares late last month, the Oracle of Omaha is still holding 882 million Bank of America (NYSE: BAC) shares, which gives him an 11.4% stake in the company!

According to LSEG data, Buffett’s conglomerate has sold 150.1 BAC million shares since mid-July for profits north of $6 billion.

There are plenty of reasons why Buffett and Berkshire may have pulled the trigger on BAC.

For one, the stock is up 50% since October 2023, almost doubling the S&P 500’s gain over the same time. That’s a healthy gain for a boring financial stock.

A Deutsche Bank analyst pointed out that Buffett may be offloading shares to bring Berkshire’s total shares below the 10% reporting threshold.

Or maybe he checked the stock’s Green Zone Power Ratings…

Bank of America Stock Is Stuck in Neutral

OK, that last reason was a bit of a jest. Buffett very well could have checked our proprietary system, but I also know he has access to a massive team of analysts and investing tools to assess the health of any and every asset known to man.

But our system can hold its own…

Buffett is lauded as one of the greatest value investors in history. Heck, he may be the top dog.

Just like Buffett, Adam O’Dell designed Green Zone Power Ratings to consider the Value factor when analyzing stocks. He touched on this key factor earlier this week…

Of course, just like Buffett, Adam considers five other key investing factors within his system. The best stocks aren’t just cheap. If you buy a stock that seems like a good value but lacks solid growth or stock price momentum, you might be stuck with a dud.

I wouldn’t call Bank of America (NYSE: BAC) a dud, but its Green Zone Power Ratings aren’t blowing my socks off either.

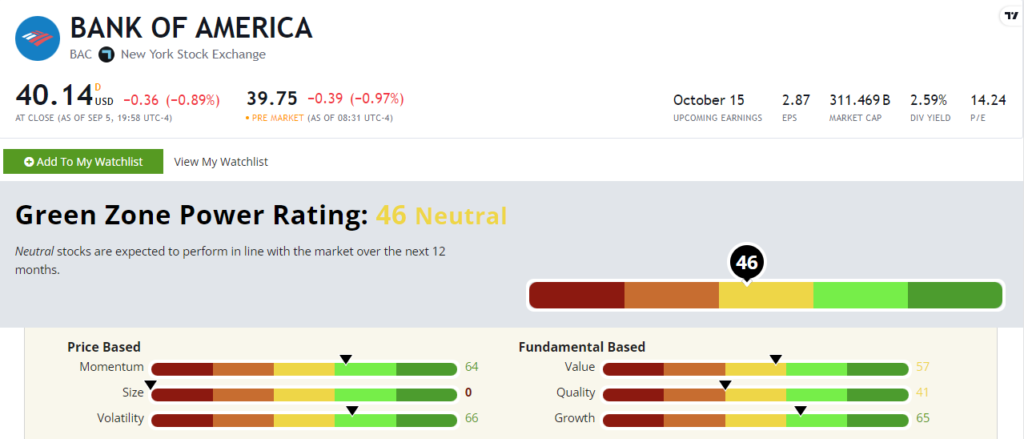

BAC’s Green Zone Power Ratings in September 2024.

With a “Neutral” rating of 46 out of 100, BAC stock is expected to track the broader market from here.

BAC’s Value factor rating of 57 indicates that its price-to-earnings ratio is slightly higher than the industry average (14.2 and 12, respectively). So this stock isn’t trading at a value price compared to its peers.

Digging into its Quality rating of 41 (which is just above our Bearish level), its 5% return on investment is lagging behind the industry’s 6.5% average.

However, Chief Research Analyst Matt Clark pointed out a critical fact: Key metrics within these factors have been declining over the last year.

BAC’s return on assets, equity and investment are all lower than where they stood in September 2023.

The same goes for its net margins and operating margins.

We’ll close by looking closer at its Momentum rating of 64. I mentioned BAC’s solid gain since last October, and a 50% gain in a year is nothing to scoff at.

In 2024 alone, the stock is up 18%, just edging out the S&P 500’s 16% gain. You could have invested in the index of 500 stocks and done almost as well this year.

Bank of America stock looks fine for now, but Green Zone Power Ratings is chock full of stocks that will do much better over the next year.

Until next time,

Chad Stone

Managing Editor, Money & Markets