Does the name sound familiar? That’s probably because it sounds like “exchange-traded fund,” or ETF. But an ETN isn’t like an ETF at all — and that’s a distinction many people fail to make.

So what’s an ETN, then?

It’s a highly leveraged, speculative instrument that lets investors access particular asset classes. In good times, ETNs can skyrocket. These, however are, er, more interesting times.

ETNs: Guaranteed Losses in the Coronavirus Crisis

As a result of the coronavirus selloff, ETNs aren’t just going to rack up big losses — they’re going to go to zero. This is a disaster, especially since there are so many valuable companies to invest in right now, including those with strong cash flows like Amazon.com (AMZN) and Apple (AAPL), which will come through this downturn just fine.

Before we go further, let’s quickly talk about how an ETN works.

Unlike an ETF, an ETN doesn’t buy the assets it’s supposed to track. Instead, it’s a debt issued by a bank that promises to pay investors the value of the index the ETN tracks. Most ETNs are issued by Swiss investment bank UBS (UBS).

So, for instance, the UBS AG FI Enhanced Global High Yield ETN (FIHD) tracks large-cap and mid-cap stocks, even though it doesn’t actually buy any of them. Instead, UBS promises to exchange the ETN for its market value, so it trades on public markets, and the market approximates the value of the ETN as if it were a real fund.

Sound abstract? It is. And a lot of ETN investors don’t fully understand this abstraction, or what it means in a downturn. One of the biggest risks with ETNs is their mandatory redemption clause. This states that, if the ETN falls under $5.00, UBS must redeem it for cash. Here’s what that would mean for FIHD.

A 52.2% Loss Is Just the Beginning

At the time of writing, FIHD trades at $80.50, so it has a long way to go (a 92.5% decline, to be more precise) before a mandatory redemption strikes. But note that it is down 52.2% already, over a period where the S&P 500 is down just 20.5%. That’s because ETNs are levered, so it would take a roughly 36% drop for FIHD to be forced to liquidate.

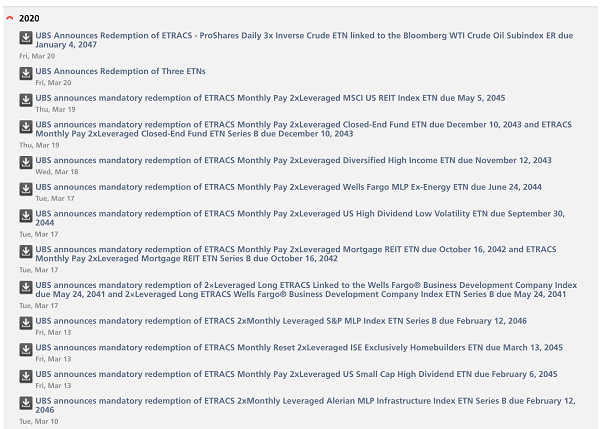

Think it can’t happen? Well, it already has for 15 of UBS’s 40 ETNs.

ETNs Disappearing Fast

Source: UBS

In other words, shareholders in those ETNs will lose essentially all of their capital because of this market downturn, while investors in dividend-paying funds backed by real assets, like closed-end funds (CEFs), can ride out the market dip while collecting dividends.

Unsustainable Payouts Drew Investors In

That brings us to why ETNs have attracted investors in the first place: income.

Before the crash, many ETNs offered dividend yields of 15% or more. These yields were just too enticing for some investors, so they bought. And they may have thought that, if they held on long enough, that income could offset the risks of holding the ETNs and their volatile assets.

There’s a simple logic to this: If an ETN is paying 15% dividends and you keep it for seven years, you’ll get your money back in income. So just hold for a decade and, if the ETN goes to zero, that’s okay, because at least you got the income.

While that may make sense in theory, reality is a bit more complicated. While some ETNs are almost a decade old, many of them have been around for only five years, and many of those are the ones being shut down now because of their huge losses.

So much for holding for the long term — these investments simply aren’t built to last.

We’ve Been Here Before

Could anyone have predicted the ETN bloodbath? Yes, because it’s happened before.

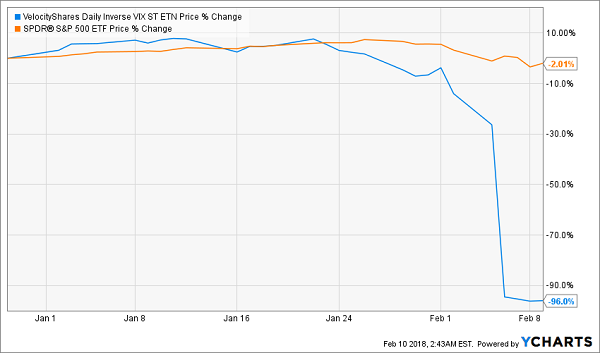

About a decade ago, another Swiss bank issued an ETN tied to the VIX called the VelocityShares Daily Inverse VIX Short-Term ETN (XIV). XIV soared during the bull market of the 2010s, when volatility kept falling. XIV, as an ETN that tracked being short the VIX, was massively outperforming the S&P 500 as a result.

How Can You Go Wrong with a Chart Like This?

Bloomberg and other professional financial outlets called this “the shoeshine boy trade” because, in 2016 and 2017, it was so popular among investors that it became a much-lauded trade in online investing forums, barber shops, restaurants and wherever else people chatted about the market.

And, like any shoeshine boy trade, it was great until it suddenly wasn’t.

This is How You Can Go Wrong

When volatility surged in early 2018, this fund went to near zero and was liquidated. That was a harbinger of doom for any ETN investor, and it prompted me to warn against ETNs at the time.

Now that many of UBS’s ETNs are being liquidated, it’s likely that this obscure corner of the financial market will shut down. At the very least, it’ll never be the same again.

To learn more about generating monthly dividends as high as 8%, click here.