Fifteen years ago investors would likely have scoffed at the idea of selling used cars online as a viable business model, but demand for the Vroom IPO on Monday proved otherwise.

The Vroom Inc. (Nasdaq: VRM) initial public offering was originally projected to offer 18.75 million shares in the range of $18 to $20 per share, but that number jumped to 21.25 million shares at $22 a pop Monday. That spike helped the online auto retailer shatter expectations and raise $468 million, over $100 million more than initial estimates.

The Vroom IPO set the company’s market cap at around $2.5 billion, but is it a buy?

The Vroom IPO

There are quite a few good things to point out about the Vroom IPO, which started trading today on the Nasdaq Global Select Market under the ticker symbol “VRM.” For one, beating projections like what investors saw in Monday’s offering may be a good sign that demand is high.

As of noon EDT today, shares of Vroom are trading at $42.40, rising more than 93% by lunchtime on the East Coast.

IPO Boutique tracks every IPO hitting the stock market and found institutional investors were piling in, which caused the deal to be “many multiple times oversubscribed.”

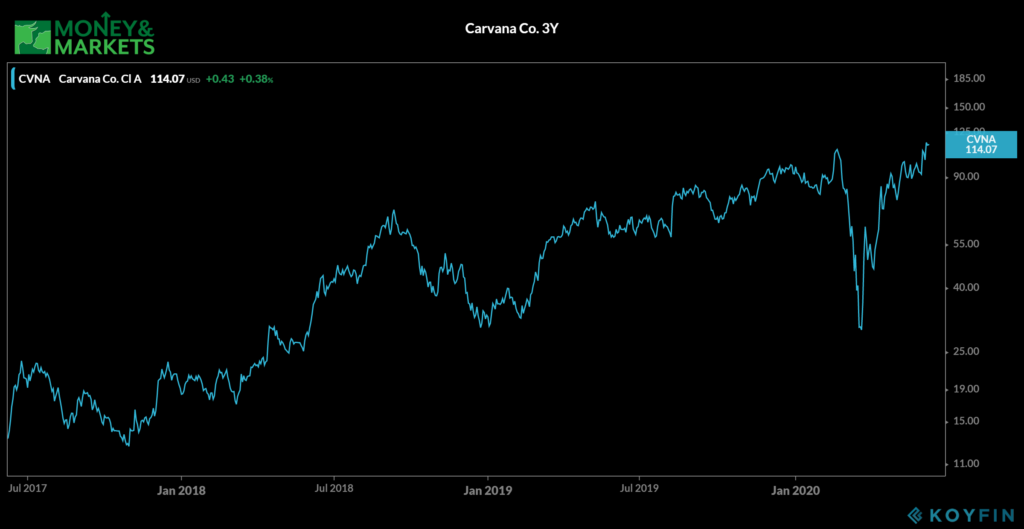

Vroom has been in business since 2012, and it has some stiff competition that may drive more success toward the Vroom IPO. Carvana Co. (NYSE: CVNA) entered the public stock market in June 2017 and has seen its market cap balloon to over $19 billion.

Shares traded at $15 three years ago, but Carvana is now trading over $110 per share, and the stock has recovered all of its losses triggered by the coronavirus crash.

After a strong first quarter that showed 43% growth year over year, Carvana slumped in mid-March through April, but the company says it’s back to 20% to 30% year-over-year growth.

Vroom has a chance to chip away at some of Carvana’s market share. Vroom’s revenue grew to $1.2 billion in 2019, a 39% surge from the year before. Of course its losses also went from $85.2 million to $143 million.

Revenue in Q1 2020 also rocketed up 60% to $375.7 million while recording $41 million in losses. But like many IPOs and startups, Vroom has not been able to turn a profit since its inception in 2012.

The Vroom IPO filing said online car sales are “ripe for disruption as an industry that is notorious for consumer dissatisfaction and has one of the lowest levels of e-commerce penetration.”

Its online approach in an industry that has been rocked by the coronavirus outbreak means it’s in a good position for when consumers ramp up spending on big-ticket items again, but also who may be wary of heading to a physical location.

Being cautious and doing your due diligence when it comes to IPOs can be the difference between getting in on the ground floor of something like Tesla Inc. (Nasdaq: TSLA), or struggling with a current loser like Uber Technologies Inc. (NYSE: UBER).

The Vroom IPO could be a good buy as its competition has thrived and more people consider online purchases as the world deals with an ongoing pandemic. However, you might want to sit out the initial pop and take a closer look once the dust settles.