It’s shaping up to be a pivotal week …

Largely because Nvidia (NVDA) is due to report earnings on Wednesday after the close, and you can bet that investors will be poring over every number and letter!

Over the past two weeks, Wall Street has really started to question the sustainability of the AI capital spending boom, and Nvidia is the epicenter of it. It’s not a stretch to say that all roads lead to Nvidia, as the company supplies the high-powered chips needed to train and run advanced AI models.

If there is any indication that demand might not be quite as strong as previously indicated, then we could be in for some real fireworks. Remember, tech shares today are priced for absolute perfection … so the bar is high.

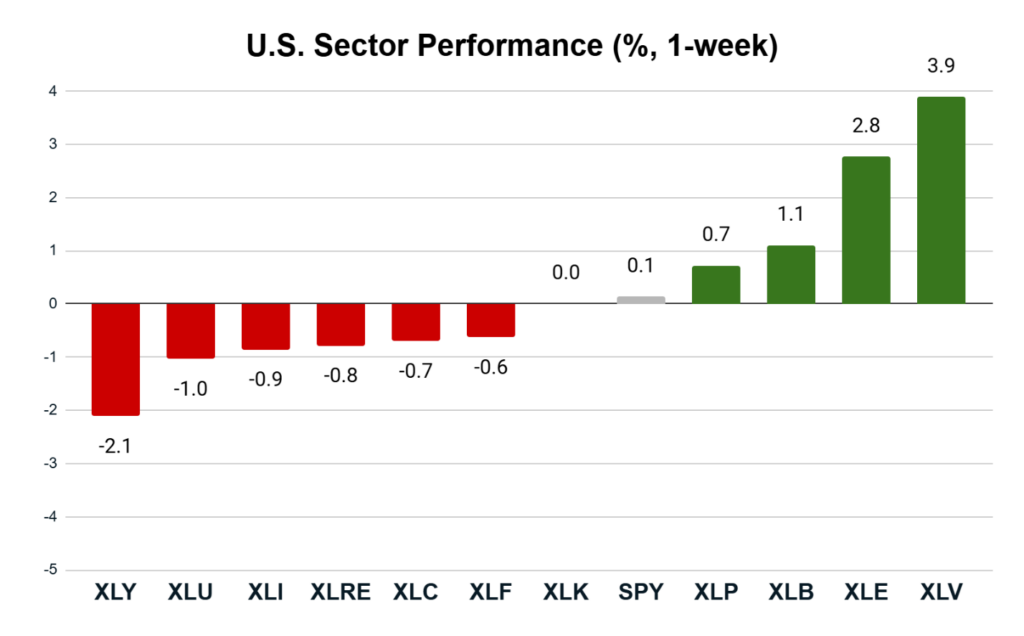

Last week, the damage in the tech sector was modest. Tech shares finished the week flat, roughly in line with the S&P 500.

Breaking down the sectors tells a muddled story.

The best performing sector was healthcare (XLV), which was up a monster 3.9% — a move that helped my Max Profit Alert subscribers see an open gain of over 100% on an XLV (options) position I recommended in late October.

Healthcare is generally considered to be a non-cyclical, defensive sector. Boom or bust, you don’t really expect healthcare demand to change all that much.

Meanwhile, consumer discretionary stocks (XLY), which tend to be sensitive to the health of the economy, were the worst-performing sector, down 2.1%.

So, a rotation out of consumer discretionary stocks and into health stocks would be a sign that investors are getting defensive.

Right?

Well, maybe not…

Utilities (XLU), generally considered to be the most defensive of all sectors, was the second-worst performing, down about 1%.

So… what’s the story?

One thing we have to remember is that the utility sector today isn’t the stodgy, old dividend play it used to be. Utilities have been major beneficiaries of the AI boom’s unquenchable thirst for power.

This means we need to be careful how we interpret sector moves. Some of the old rules about what constitutes “bullish” or “bearish” sector action may not apply here.

Key Insights:

- Sector signals are mixed but showing a defensive rotation.

- Healthcare has replaced utilities as a defensive barometer.

- Economically sensitive sectors are weak.

Overall, signs point to a market in search of direction. We could have more clarity this week after Nvidia and Walmart report their quarterly earnings. But for now, sector moves are suggesting we should be cautious.

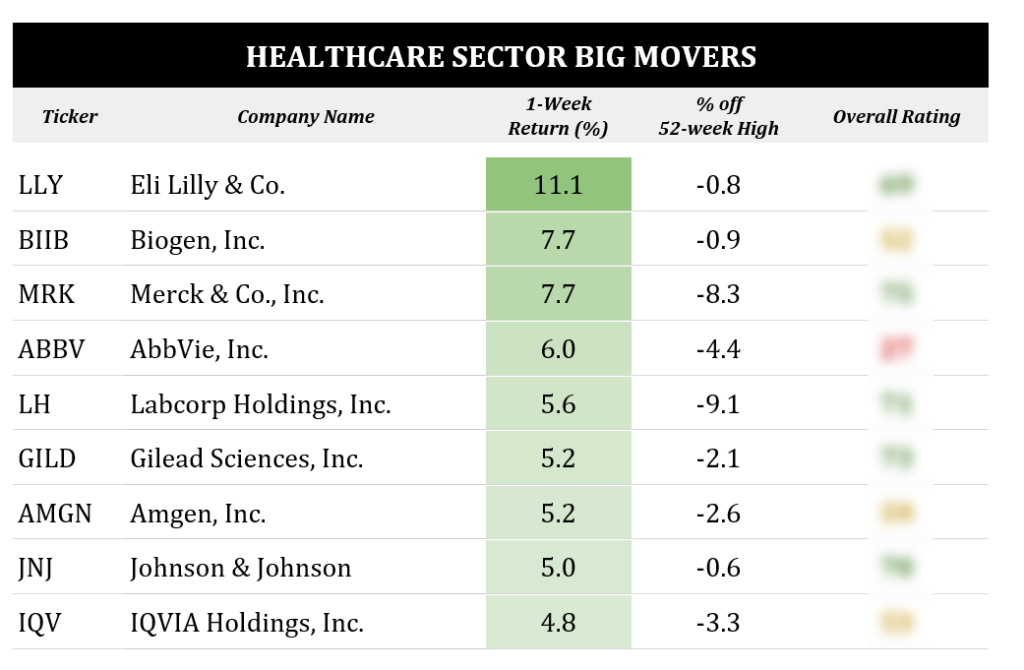

Low-Volume Winners in the Healthcare Sector

Let’s take a deeper look at the healthcare sector. I screened for the biggest winners of the week that are still trading within 10% of their 52-week highs.

The real standout last week was Eli Lilly (LLY). The shares were up 11% on the news that the company inked a deal with the Trump Administration.

Starting April 1, 2026, Medicare will begin covering Lilly’s leading weight loss drug, Zepbound. While the Administration is taking its pound of flesh – Medicare will reportedly be paying a 55% discount off of retail prices – it potentially opens the floodgates by making the drug available to the 68 million Americans currently on Medicare.

At $245—a 55% discount from current net prices, according to Leerink Partners. While this is a steep concession, it opens a vast new market for Lilly. As an added bonus, Lilly also won an exception from the administration’s tariffs in return for lowering its prices.

Lilly currently rates a “Bullish” 69 on my Green Zone Power Ratings system, and it’s not the only one. Merck (MRK), Labcorp (LH), Gilead Sciences (GILD) and Johnson & Johnson (JNJ) all make the cut as “Bullish” as well.

These companies have one thing in common: all rate exceptionally well on my system’s volatility factor.

That’s exactly what you expect to see from a defensive sector. If you’re looking for quality, low-vol companies that won’t give you heartburn, then health stocks are a great place to start.

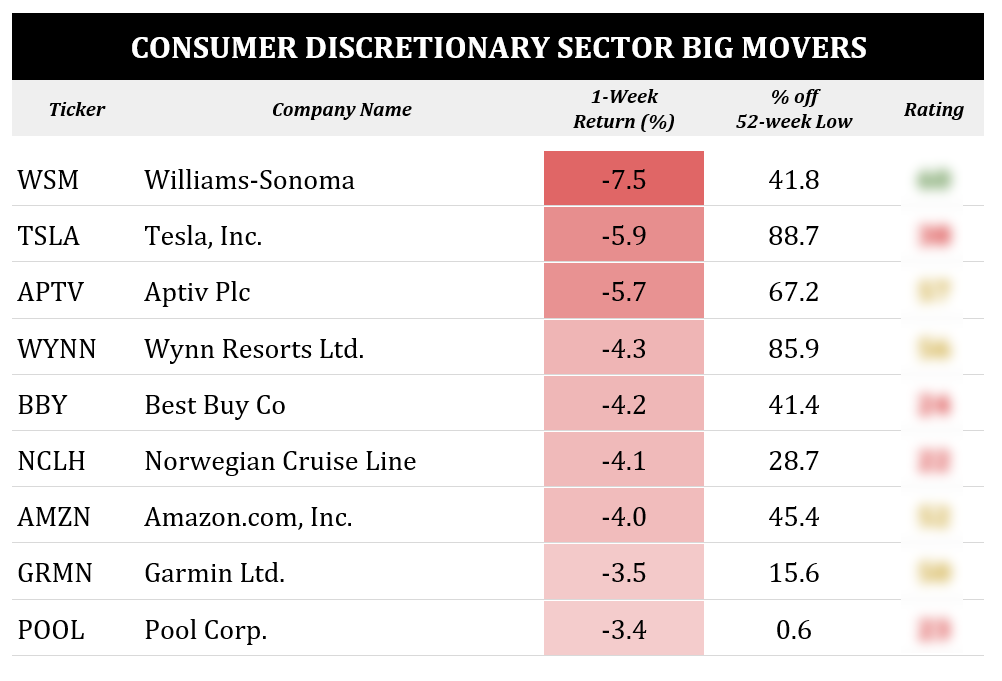

Consumer Discretionary Stocks Had a Rough Week

Normally, when I do a deep dive into the worst-performing sector, I look for stocks that sold off aggressively that are also within 10% of their 52-week lows.

Well, this week is different…

I had virtually no stocks meeting those criteria. All of the consumer stocks that got beaten up last week also happened to be some of the year’s standout performers … so they’re nowhere close to their 52-week lows.

As an example, look at Tesla (TSLA).

While Tesla is considered an “AI stock,” it is technically classified as a consumer discretionary.

Well, it got shellacked last week and finished down almost 6%. Yet despite this, it’s still more than 88% above its 52-week low.

So, how do we interpret this?

To start, it’s far too early to go bottom fishing in the consumer discretionary sector. Many of the stocks still look very extended after the epic run they’ve enjoyed since April, even after accounting for last week’s sell-off.

Furthermore, apart from Williams-Sonoma (WSM), which just barely qualifies with a Green Zone Power Rating of 60, none of the other stocks on the list qualify as “Bullish.”

So, what is my system saying today? That this is a market in search of direction, and until it breaks one way or the other, sticking to defensive sectors and highly-rated “Green Zone” stocks is a wise choice.

To good profits,

Editor, What My System Says Today