Retail companies have been dropping steadily thanks to sagging consumer confidence due to the coronavirus lockdown, and while prices will rebound, there are three retail stocks to avoid at all costs.

As more and more Americans are confined to their homes because of the COVID-19 pandemic, retail chains are taking a massive hit.

Millions of workers have been furloughed or laid off as stores around the country are closed to prevent the spread of the virus.

That has put the retail sector in a huge pinch with sales confined to just online shopping.

However, as Americans fear an economic recession, most shopping is for essential items and groceries.

While all retail companies have felt the pinch of declining sales and falling consumer confidence, these are the three retail stocks to avoid investing in at all costs.

3 Retail Stocks to Avoid at All Costs

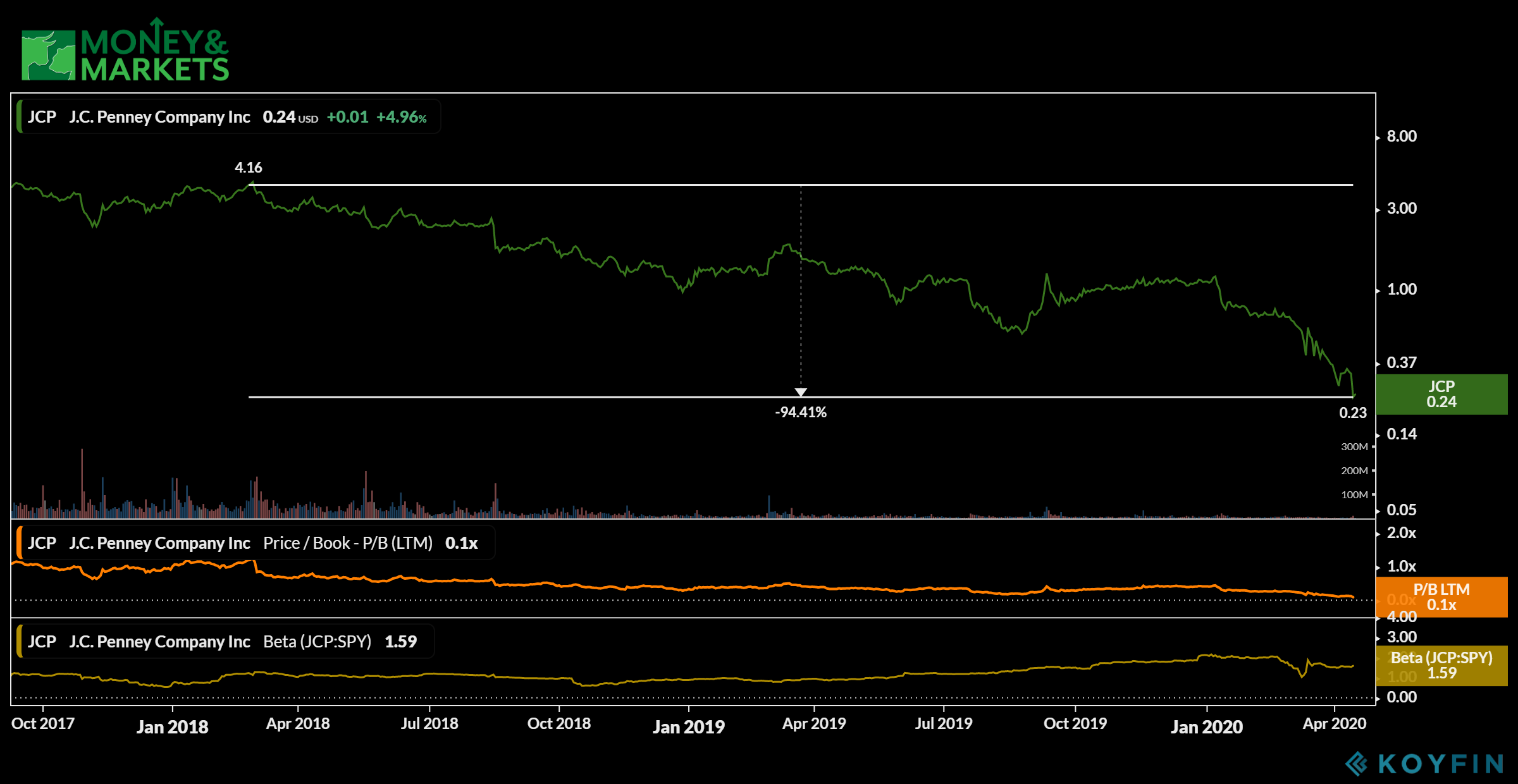

1. JCPenney Co. Inc.

Market Capitalization: $74.6 million

Annual Sales (2019): $11.1 billion

Earnings Per Share: -$0.81

60-Month Beta: 1.59

Annual Dividend Yield: 0.00%

If there is a retail company in trouble because of the recent downturn, it’s JCPenney Co. Inc. (NYSE: JCP)

Once one of the largest department store chains in the country, the company is now exploring bankruptcy to restructure its debt. It already missed a $12 million debt payment.

JCPenney’s stock was already cheap before the market tanked — only about $4 per share in early 2018 — but it has since shed more than 94% off its share price.

The company also had a nice dividend yield before but has suspended that because of tanking sales. The unstable climate has also provided little relief for JCPenney.

Its current earnings is actually minus-$0.81 per share.

Despite its bargain-basement share price of around $0.25 per share, the company remains volatile with a 60-month beta of 1.59.

While the retail sector will bounce back at some point, bankruptcy talk is a big reason why JCPenney Co. Inc. is one of the three retail stocks to avoid at all costs.

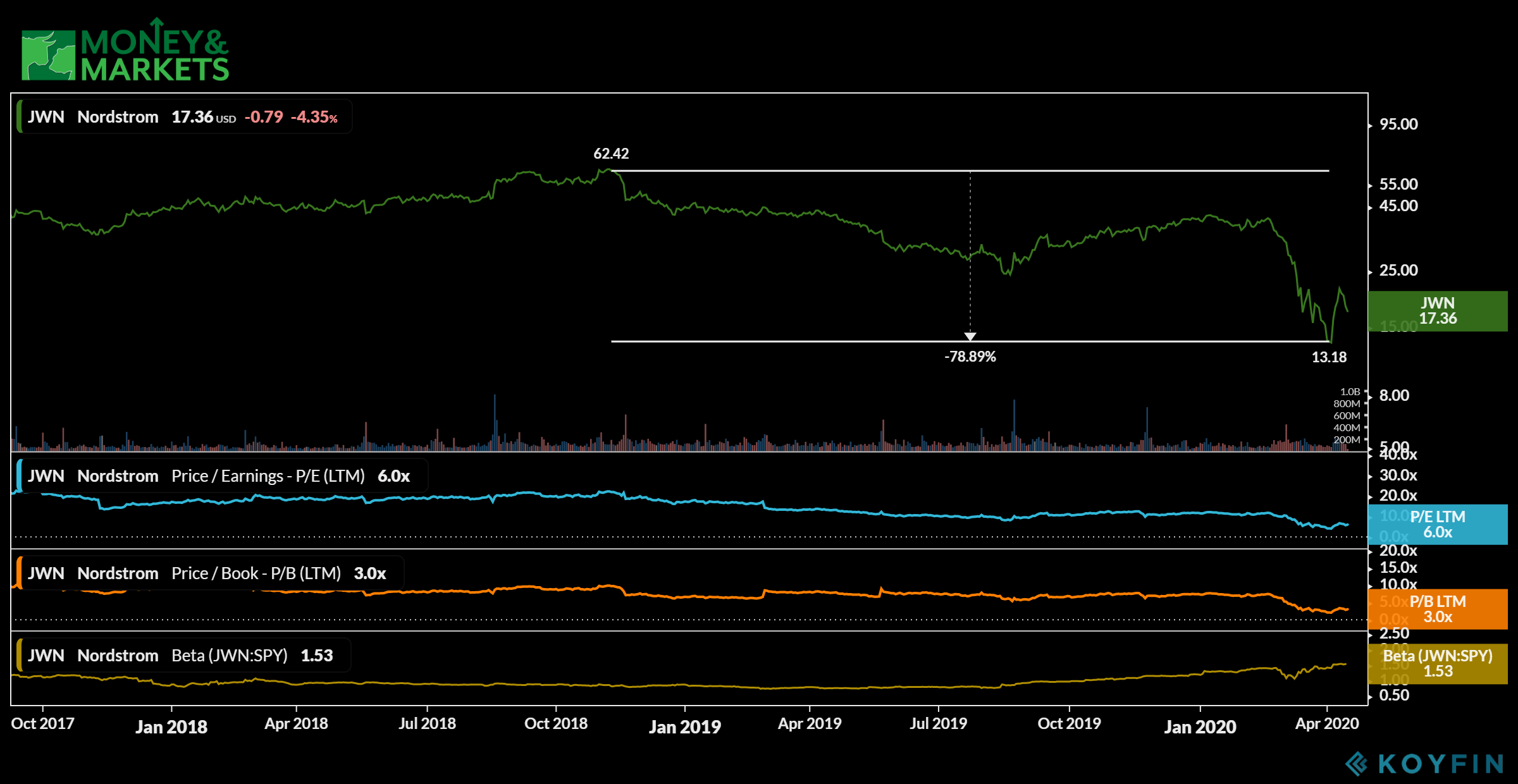

2. Nordstrom

Market Capitalization: $2.8 billion

Annual Sales (2019): $15.5 billion

Earnings Per Share: $3.36

60-Month Beta: 1.53

Annual Dividend Yield: 0.00%

If discount retailers are suffering, high-end retailers are getting hit much worse.

As is the case with Nordstrom (NYSE: JWN). The company’s leadership group is forgoing its salary as are the CEOs and the board of directors.

Nordstrom was already trending down before the COVID-19 market crash and it just got worse.

Since reaching a high of around $62 per share in November 2018, the company’s share price plummeted by 79% to around $13 per share in March 2020.

But the biggest issue for Nordstrom is that the market crash came at a time when the company was transitioning. It was moving from its high-end department store model to more niche stores.

You couple a crater in the market with a huge change in the business model and you have a recipe for disaster.

Nordstrom remains a volatile stock to get into with a 60-month beta of 1.53. And while its price is cheap — around $17 per share — it hasn’t shed enough of its previous losses to add any confidence.

Between that and the fact that its transition is going to be pushed back even farther makes Nordstrom one of the three retail stocks to avoid at all costs.

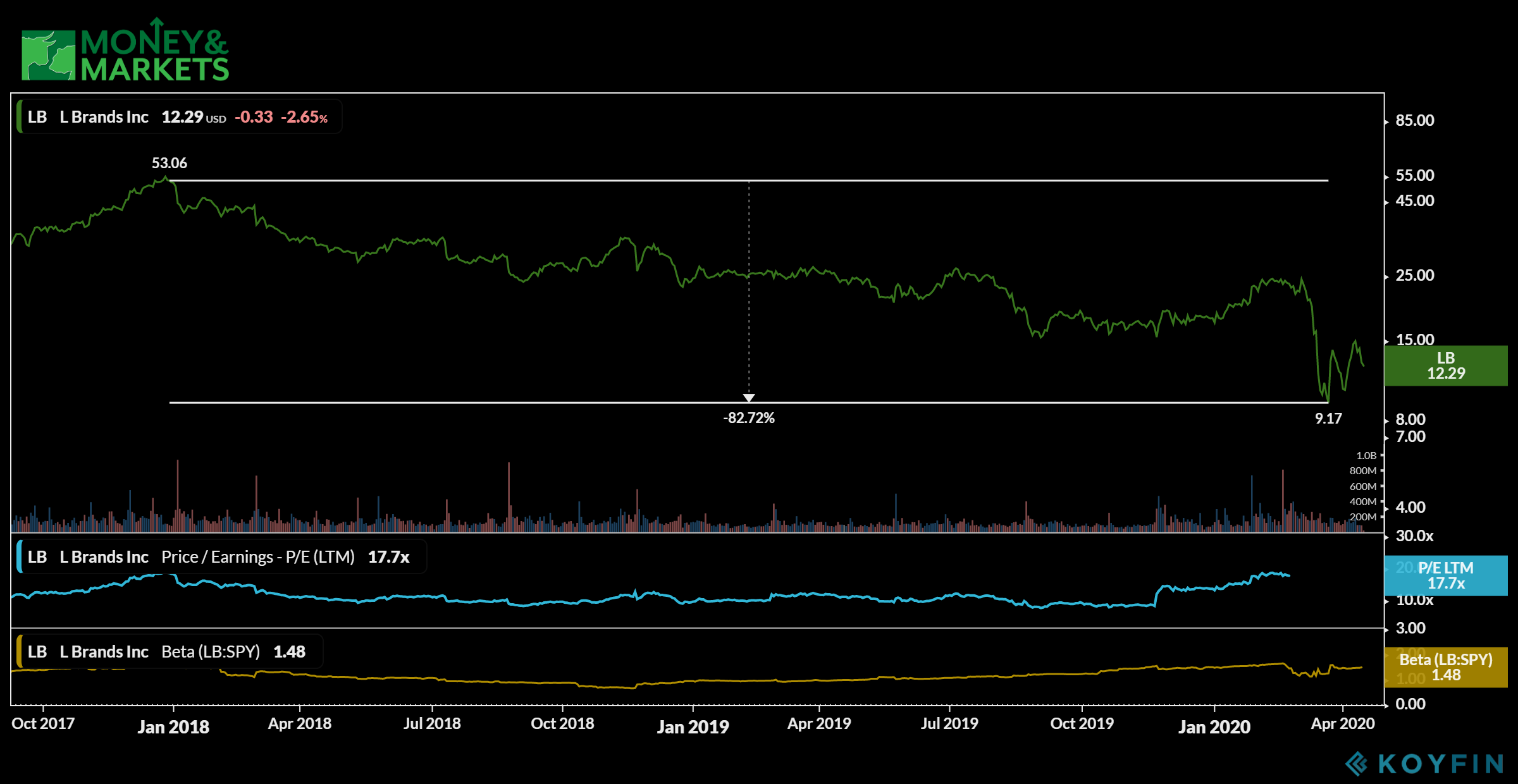

3. L Brands Inc.

Market Capitalization: $3.5 billion

Annual Sales (2019): $12.9 billion

Earnings Per Share: $2.28

60-Month Beta: 1.48

Annual Dividend Yield: 9.51%

Another retailer hit hard with a case of bad timing is L Brands Inc. (NYSE: LB).

The operator of Bath & Body Works and Victoria’s Secret was in the midst of selling off its lingerie business and spinning off Bath & Body Works into a separate entity.

Since December 2017, the company dropped more than 82% off its share price after it hit a low of $9 in March 2020.

So it was already falling and the coronavirus crash made it that much worse.

And, just like Nordstrom, the fact that the crash came at the same time as the selloff of Victoria’s Secret, doesn’t bode well.

In the last five years, the company has provided negative returns and it suffered from negative net annual income in 2019.

L Brands’ volatility is less than the others on the list, but still high at 1.48. Its price-to-earnings ratio is also a little high at 17.7.

The company does have a dividend yield of 9.51%, but that could be just an attraction to entice more buyers. It certainly isn’t because of revenue growth as its 5-year revenue growth is only 12%.

A lack of sustainable growth, even when the retail sector was good, is a big reason why L Brands Inc. is one of the three retail stocks to avoid at all costs.

So, here you have a list of companies that were pretty battered and bruised before the coronavirus took hold. Now, things are getting worse.

It’s going to take a long time for any of these three companies to get back to good health. They aren’t necessarily bad companies, just timing has not been in their favor.

That’s why they are the three retail stocks to avoid at all costs.