The coronavirus pandemic is affecting all aspects of life and after months of stymied economic activity, your Social Security COLA (cost-of-living adjustment) is likely to be nonexistent in 2021 because of the ongoing pandemic.

The Senior Citizens League (TSCL) has been running the numbers, and its initial Social Security COLA projection for 2021 is 0% based on the fact that the economy has come to a standstill, and prices have been falling in certain consumer sectors.

TSCL Social Security Policy Analyst Mary Johnson said falling prices actually increased the program’s buying power by 3% in 2019, but it’s also had an adverse effect on the Social Security COLA.

“When there are lower prices, this is a signal of deflation, which means a lower cost-of-living adjustment is on the way,” Johnson said. “The recent unprecedented plunge in oil prices have all but wiped out the prospect of a Social Security cost-of-living adjustment for next year.”

Simply put: If there’s no inflation, there’s no increase in benefits. At least you can rest assured your benefits won’t go down.

The Social Security COLA was only 1.6% in 2020, and it has been 0% three times since 2010

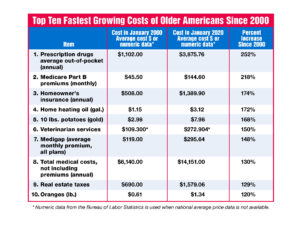

Even so, cost adjustments simply aren’t keeping up with prices for certain items older Americans are prone to buy. A TSCL study found that while benefits have increased by 53% since 2000, prices for items popular among retirees have risen by almost double that to 99.3%.

The No. 1 battle on the price front is medical costs. Almost 40% of respondents in a TSCL survey said they pay more than $750 per month on Medicare and other health care costs like prescription drugs.

Social Security’s average monthly benefit is $1,503 per month in 2020, so half that check is going toward one category of spending.

And the 1.6% Social Security COLA for 2020 only added about $24 to the average payment. That simply doesn’t cut it for a lot of Americans who rely on the benefits program.

The Social Security Administration uses data through the third quarter of a given year to calculate the Social Security COLA, so there is still time for that to rise. I wouldn’t count on it, though.

How to Plan for No Social Security COLA

With the economy stalled out as states try figure out the best way to reopen without triggering another outbreak of COVID-19, there’s a good chance prices won’t rise enough in the next five months to make up for a rough first half of 2020.

It’s probably best to go ahead and pretend the 0% Social Security COLA is a done deal.

Even if it comes in at a 1% increase, like an earlier projection from Kiplinger’s showed, that’s not going to make a huge difference in your monthly benefits so consider it gravy.

If you plan for 0%, you won’t be surprised when it comes to fruition. Anything higher than 0% will be a pleasant surprise.

Planning for 0% means you can start saving part of what you get now — if you can manage it — and create your own sort of Social Security COLA for 2021. Or if you rely more heavily on the program, at least you know what your benefits will look like through 2021 so you can more easily budget for the future.

If you haven’t hit retirement yet, or haven’t started claiming Social Security, this should serve as a bit of a warning for the state of the benefits program. It’s a great thing to have, and it can help bolster your retirement plans. But relying on it too heavily can be a dangerous prospect.

For years the Social Security COLA has not kept up with the rising costs for older Americans, particularly in regard to outrageous health care costs, so be prepared for more disappointment in 2021.

• You can find all of the latest and most important news about Social Security here on Money & Markets.