Right now, U.S. debt exceeds the size of the nation’s economy. According to the Congressional Budget Office, total government debt is 100.1% of GDP.

This level of debt is long associated with financial crises.

Famously, among economists, Kenneth Rogoff and Carmen Reinhart warned that problems develop when debt exceeds 90% — crises can develop and defaults are possible.

This analysis ignores something mortgage bankers consider — the level of debt isn’t as important as the borrower’s ability to make the payments.

When applying for a mortgage, the debt amount is almost always more than 100% of income. The lender looks at the amount of the payment rather than the amount of the loan. Of course, the two relate, but qualifying for the loan is determined by the ability to repay it.

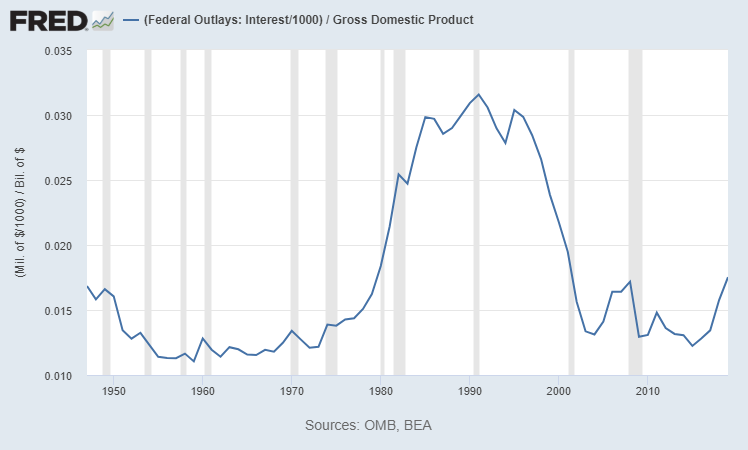

From that perspective, the U.S. government is in good shape. The chart below shows interest payments as a percent of GDP. The trend is down since interest rates peaked in the 1980s. Lower rates make the debt more affordable even as the amount of U.S. debt rises.

U.S. Debt Interest Compared to GDP

Source: Federal Reserve.

U.S. Debt Is Affordable

Last year, the federal government paid about $344 billion a year in interest. This represents less than 1.7% of GDP. That’s about 5% of what the government spends.

As long as interest payments are manageable, there isn’t a crisis. This is true for governments, just as it is for mortgage borrowers.

But governments have an advantage over consumers.

While consumers can face repayment problems if their income falls in a crisis, governments can print more money when faced with a crisis.

Printing money can lead to inflation, but that might not be a problem for the U.S. in the 2020s. Since the Federal Reserve holds much of the debt, it can simply forgive some obligations.

So, although the federal debt is high, it shouldn’t matter to policymakers or investors.

Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at the New York Institute of Finance. Mr. Carr is also the former editor of the CMT Association newsletter, Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.