Zoom Video announced today it is acquiring startup encryption provider Keybase. It’s good news for the company, but investors should wait.

When Americans were first ordered to shelter in place and millions were directed to work from home, Zoom Video Communications (Nasdaq: ZM) was a hot commodity.

Individuals and companies rely on Zoom’s video communications platform to keep in touch with relatives and make communication and meetings between coworkers seamless.

Then “zoombombing” happened.

Now the company has tried to alleviate its security issues by acquiring startup encryption provider Keybase. Terms of the deal were not disclosed and Zoom Video shares rose 6.6% in midday trading on Thursday.

What the Purchase Means for Zoom Video Users

For one thing, buying a company with expertise is encrypting networks should give Zoom more credibility.

The biggest thing about “zoombombing” is that it illustrated just how vulnerable Zoom’s connections were to outside sources.

Meetings were easily hacked, allowing malicious activity like eavesdropping, using racial slurs and even posting pornographic images.

The Federal Bureau of Investigation even took notice of the problem.

By bringing encryption into its fold, Zoom is hoping to put users at ease about potential hacking.

“This acquisition marks a key step for Zoom as we attempt to accomplish the creation of a truly private video communications platform that can scale to hundreds of millions of participants, while also having the flexibility to support Zoom’s wide variety of uses,” Zoom CEO Eric Yuan wrote in a blog post announcing the deal.

So, in that regard, Zoom’s acquisition is a good thing.

What About For Investors?

This is where things get a bit more interesting.

Yes, a marriage of Zoom Video and Keybase should allow the former to lock down its platform, which is likely the reason the stock has shot up so much.

But, in the long term, fundamentals are working against Zoom.

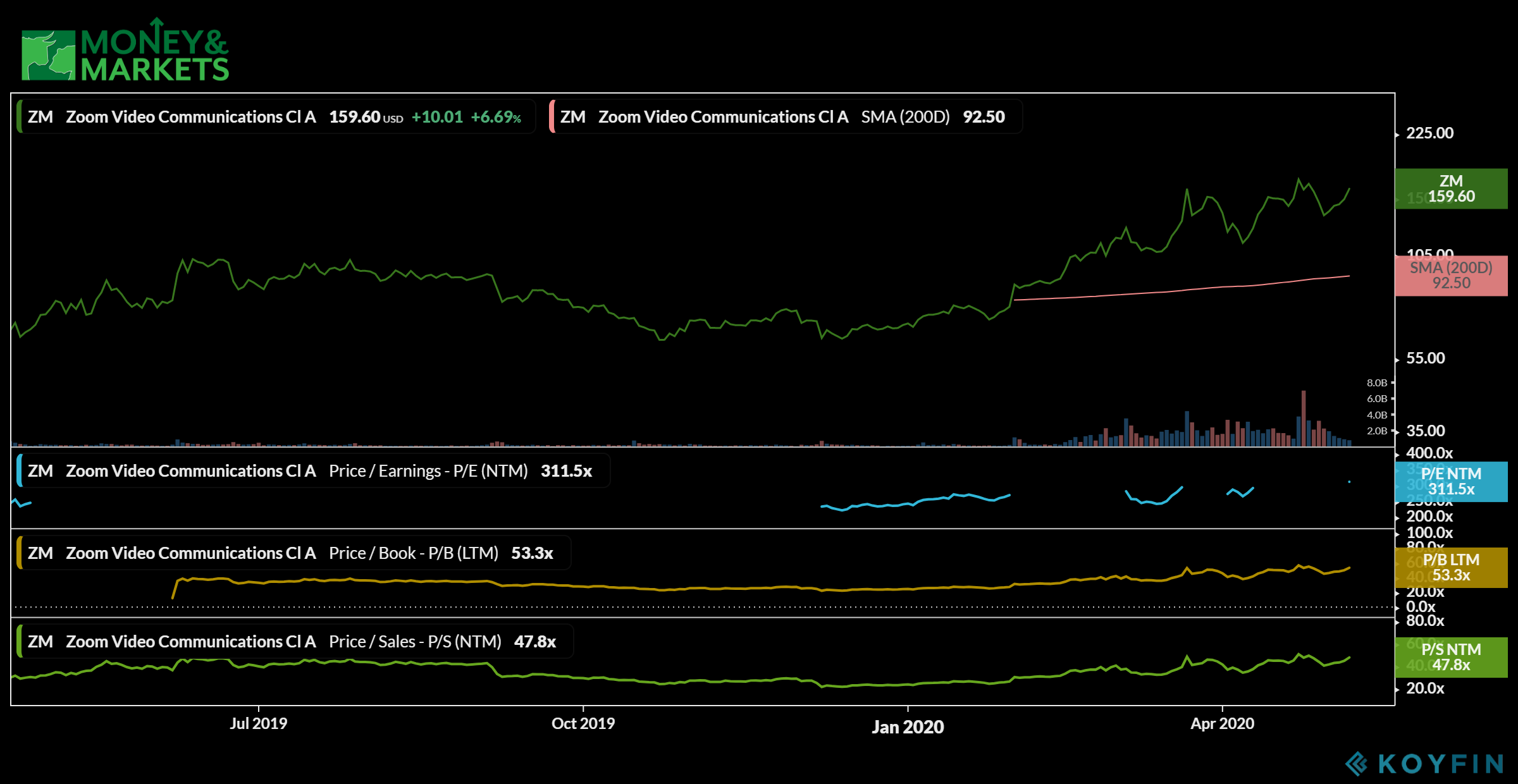

It’s currently trading more than $60 above its 200-day moving average, but the real story is when you look ahead.

For the next 12 months, Zoom is projected to trade with a price-to-earnings ratio of 312 — which is enormous and suggests the company is extremely overvalued.

What’s more, Zoom’s price to book stands at 53.5 and its price to sales for the next 12 months is 47.9. That further illustrates that the share price is inflated and likely to come down before long.

Zoom has been riding a high because of the coronavirus lockdown forcing social distancing and remote work.

If you got in on Zoom before the pandemic really took hold, you are looking at very solid gains. In that instance, I would hold your position until this bounce runs its course, then sell for profit.

But, if you are contemplating buying Zoom shares because of this recent announcement, I would wait. The fundamentals just don’t’ scream “buy” right now.

The stock is going to meet resistance at some point and likely start a downward trend. Buying now could mean losses.

So, if you’re in Zoom Video now, stay there for the time being. If not, it’s best to move on to something else.