The coronavirus crash has rocked financial markets — and retirement accounts across the country — but there may be a silver lining within the investing strategy known as dollar-cost averaging.

Many people may not have retirement contributions on their minds as the coronavirus pandemic creates uncertainty for the future of the U.S. economy, but if you are fortunate enough to have cash on hand, you can make that money work harder once the markets recover — and they will.

Stocks in the U.S. are experiencing an incredibly fast crash right now. In fact, the S&P 500’s 30% sell-off since mid-February was the fastest ever — beating the pace set during the Great Depression. While it hasn’t been a fun ride for investors or anyone with money in the markets or stock-heavy retirement accounts, it does provide an opportunity to put your money to work to take advantage of dollar-cost averaging during a market crash like this one.

How Dollar-Cost Averaging Works

Dollar-cost averaging is a simple concept where you invest an equal amount of money into a particular market or asset in regular intervals. It basically allows you buy more shares of an asset when prices are low and fewer shares when prices rise.

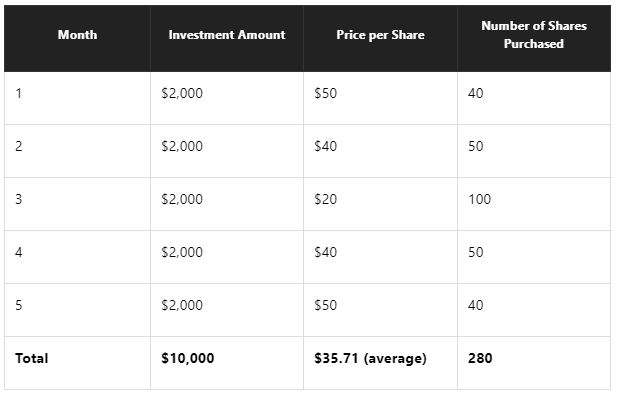

Using this strategy essentially guarantees you will pay less per share over a certain period of time by putting your money in a little bit at a time. Let’s take a look at this example from The Motley Fool. An investor decides to put $10,000 into a company over five months by purchasing $2,000 worth of shares on the first of every month. Here’s a chart breaking down the trades:

Chart Credit: The Motley Fool

Averaging the price of shares from each trading day ($50, $40, $20, $40 and $50) comes out to $40. When you divide the total amount invested by the number of shares purchased over the five months you come out to $35.71, which is a good chunk of savings that allowed more shares to be purchased.

While it would’ve been great to spend the entire $10,000 when shares were only $20, outside of blind luck, it’s virtually impossible to time the market like that without some insider knowledge, even if you’re a professional trader. Dollar-cost averaging allows you to get more bang for your buck over time.

Of course, shares will eventually go up, which means less shares will be added to your portfolio down the road. Remember, though, that the average price per share in your portfolio will always be lower over time.

Dollar-cost averaging takes a lot of stress out of timing the market as well because you are sticking to spending a set amount of money in certain intervals. Of course, some of those purchases will feel better than others, but investing is a game of emotions and dollar-cost averaging removes some of that emotion from the equation — having a plan and sticking to it is what the most prudent investors do.

You are probably already using dollar-cost averaging, too, if you are enrolled in a 401(k) plan. These types of accounts take out a certain percentage of your paycheck to invest in set intervals. If you have an IRA you can talk to your financial institution about making automatic contributions from your bank account as well.

Saving for retirement may not be on your mind after the recent market crash, but using an investing strategy like dollar-cost averaging could lead to great results down the road. Putting any amount to work now — no matter how small — means you’re setting yourself up for more peace of mind in your golden years.