Picture a Wall Street analyst in late March, staring at a screen full of red.

Tariff noise, rate uncertainty, a market that couldn’t find its footing.

The natural instinct?

Pull back. Trim the buy ratings. Wait and see.

Three months later, a funny thing happened: most of them didn’t.

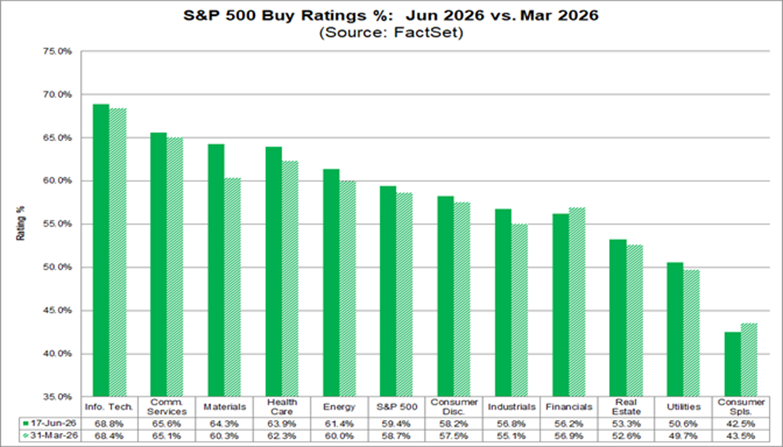

According to FactSet data as of June 17, analyst buy ratings across the S&P 500 Index have quietly crept higher since the end of the first quarter — rising from 58.7% to 59.4% for the index overall.

That might sound like a rounding error, but the sector breakdown tells a more interesting story heading into earnings season.

Materials made the most dramatic move, jumping nearly four full percentage points to 64.3%, suggesting analysts see something in the commodity and industrial supply chain trade that the broader market may be underpricing.

Tech and Communication Services held their spots at the top of the conviction table — 68.9% and 65.6%, respectively — which means the AI-driven growth thesis hasn’t lost many believers on the Street.

The outlier worth watching: Consumer Staples.

Buy ratings there actually fell, from 43.5% to 42.5%, leaving the sector as the clear skeptic’s corner of the market.

When defensive names can’t even hold analyst enthusiasm, it’s usually a signal that the consensus expects the economy to stay resilient enough that nobody needs a hiding place.

For investors parsing second-quarter earnings reports over the next few weeks, these ratings are a useful backdrop.

Sectors with rising analyst conviction — materials, industrials, health care — may be where beats carry the most upside surprise.

Sectors where enthusiasm is thin or fading? The bar for disappointment just got lower.

Before I get into next week’s earnings, let me revisit an earnings call I made not long ago…

ACN Beats Earnings Estimates

Two weeks ago, I highlighted Accenture PLC (ACN) as a company that beat analysts’ earnings forecasts.

Well, that is just what happened.

The tech company reported diluted earnings per share (EPS) of $3.80… well above the $3.72 analysts projected.

Here’s what I said about the company’s prospects of beating estimates:

And yet there’s a reasonable case that it still undersells what’s coming.

Here’s why: Accenture has quietly become the tollbooth on enterprise AI adoption. Fortune 500 companies aren’t building their own AI infrastructure from scratch — they’re paying Accenture to do it for them.

The firm has been funneling billions into AI-related services, and that pipeline keeps growing. In the company’s last report, it cited more than $3 billion in AI bookings for the fiscal year.

That number has likely only grown.

Well, that number… along with top-line revenue and EPS… did grow.

Accenture reported quarterly revenues of $18.7 billion, down from estimates but up 9% year over year.

The company expanded its operating margin by 20 basis points and its operating income by 6%… all very healthy figures.

Since its quarterly report, ACN shares are up nearly 1%, no doubt due to strong earnings.

Now, let’s look at potentially “bullish” earnings for next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their EPS from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are two companies that made this week’s list:

Of the two names flagged for next week, I’m keeping an eye on MSC Industrial Direct (MSM). The system rates it solidly in bullish territory, and there’s a real story behind why this one might have more in the tank than the “smart money” is giving it credit for.

MSM is a distributor of metalworking tools, fasteners and maintenance supplies — the kind of unglamorous industrial business that tends to move in lockstep with the health of American manufacturing.

And here’s the thing: American manufacturing has been quietly getting its act together. Reshoring is no longer just a talking point — it’s showing up in factory orders and capital spending data.

When plants are humming, companies like MSM see higher volume, more frequent reorders and better pricing power.

The EPS estimate jumps from $0.76 last quarter to $1.27 — a significant lift.

That’s the kind of boost that could easily miss if the macro softens, but it could also prove conservative if industrial activity holds firmer than expected.

MSM has a history of operational discipline, and management has been investing in its e-commerce platform to drive efficiency and customer stickiness.

The setup isn’t flashy, but that’s the point.

In an earnings season where everyone’s watching the Big Tech names, a quiet beat from an industrial distributor trading on realistic expectations can be a pleasant surprise.

As we approach the end of the quarterly earnings season, our system has not identified any potentially “bearish” earnings for next week.

So, that’s all from me.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets