It turns out that gaming on a personal computer is an expensive hobby. My 11-year-old son recently proposed that I buy him a high-end gaming PC to fuel his Fortnite addiction.

The price tag?

$4,000.

Clearly, that’s not happening. I’m writing this on a Microsoft Surface that costs less than $800. For crying out loud, I’ve owned cars that cost less than $4,000.

I’ll buy him a gaming PC. It’s going to cost a lot less than $4,000, and we’re going to build it ourselves. It will be an educational experience for both of us.

In any event, I have computers on the mind, and this brings me to leading CPU chipmaker Intel Corporation (Nasdaq: INTC).

Intel is best known for producing the “brains” of personal computers. But it does a lot more than that. Intel also has a thriving server business. And its equipment is used in cloud computing, artificial intelligence and autonomous driving. Those are three of the biggest trends to invest in today.

Let’s see how Intel shakes out on our Green Zone Ratings model.

Intel’s Green Zone Rating

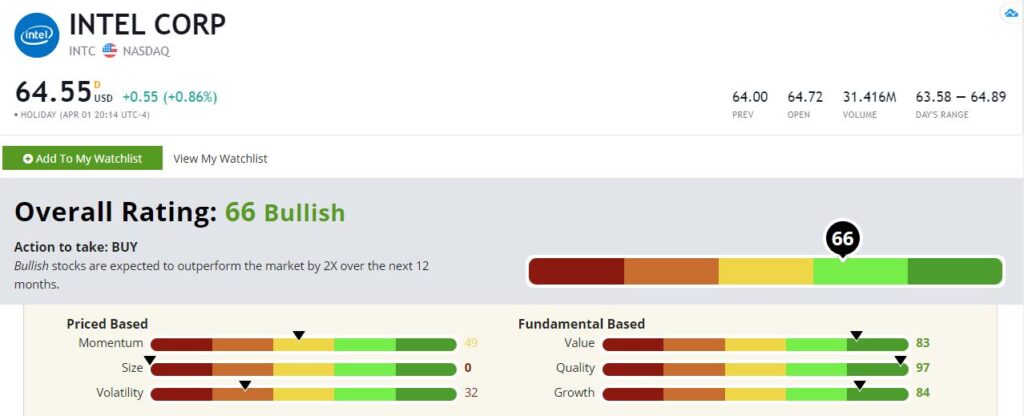

It rates a 66 overall, which puts it in “Bullish” territory in our model.

Intel Corp.’s Green Zone Rating on April 2, 2021.

Based on Adam’s historical research, Bullish stocks are expected to outperform the market by two times over the following 12 months. But let’s dig a little deeper to see what’s driving that rating.

Quality — INTC kills it on quality. The stock rates a 97 out of 100. This is not at all surprising considering that Intel is the name in traditional CPUs. Intel has no real direct competitors at this point. Its biggest strategic rival is graphics processing unit (GPU) maker Nvidia Corp. (Nasdaq: NVDA), whose chips are used extensively in cryptocurrency mining and artificial intelligence. Intel’s strong leadership allows it to charge a premium over rivals, which boosts its margins and its returns on equity, assets and investment.

Growth — While Intel might not be quite the growth dynamo Nvidia is, it’s no slouch. Intel rates an 84 out of 100 on growth. Intel’s traditional PC chip business has been strong and logged its fifth consecutive year of record revenue last year, and its data center business isn’t far behind. Data center revenues were up 11% last year. Management expects growth to be a little more modest this year as its buyers digest some of their recent expansion. But data center growth won’t be slowing for long, and Intel will be there to supply them.

Value — In a market in which the top tech stocks are very expensive, Intel is a stand-out on value. It rates an 83 here. Intel is considered by many investors to be “old tech” and lacks the sex appeal of newer offerings in social media and fintech. But, let’s face it. Intel chips are the engines that make most of these newer tech darlings go. Intel trades for just 13 times earnings and sports a dividend yield just north of 2%.

Momentum — Intel rates in the middle of the pack on momentum at 49. It tracks the market based on our criteria. Ordinarily, I’d like to see a higher rating on this metric, but being middle-of-the-pack in a raging bull market is not a bad thing.

Volatility — Despite being a long-established company and the undisputed leader in its industry, Intel rates low based on volatility at 32. Remember, a low score here means that the stock is volatile relative to the broader market. It’s just the nature of this beast. Semiconductors are a volatile, cyclical industry.

Size — Intel is a massive company, and its score rounds down to zero here. Intel is a fantastic company … but we won’t be getting a small-cap bounce here.

Bottom line: Intel is one of the great growth stories of the past half century. The digital age was largely made possible by Intel’s hardware. It’s a mature company today, but it still has attractive growth prospects in front of it due to its growing data center business.

P.S. Intel was one of the biggest stocks of the 1990s as it rose more than 8,000% in 10 years during the internet stock boom. Chief investment strategist Adam O’Dell is now targeting a stock trend that he believes has the potential to be bigger than the internet: genomics.

He believes DNA technology is mankind’s next great leap forward. And he’s targeting this mega trend through his Top 4 DNA buy recommendations. To find out more about this tech that he calls “Imperium,” click here.

To safe profits,

Charles Sizemore

Editor, Green Zone Fortunes

Charles Sizemore is the editor of Green Zone Fortunes and specializes in income and retirement topics. Charles is a regular on The Bull & The Bear podcast. He is also a frequent guest on CNBC, Bloomberg and Fox Business.