As someone with self-diagnosed social anxiety, splitting the bill used to be nightmare fuel for me.

I can’t tell you how often I fronted the bill because I didn’t want to hassle the server by splitting checks.

It’s not that I didn’t enjoy treating my friends to dinner now and again.

But my social anxiety was starting to break my bank.

When Venmo came around, an acquisition of PayPal in 2013, I was more than relieved.

And so were my credit cards. (But hey, I got rewards for eating at restaurants.)

I remember thinking this was an invaluable product that would make PayPal untouchable in its industry.

But that may not be the case according to its Stock Power Ratings.

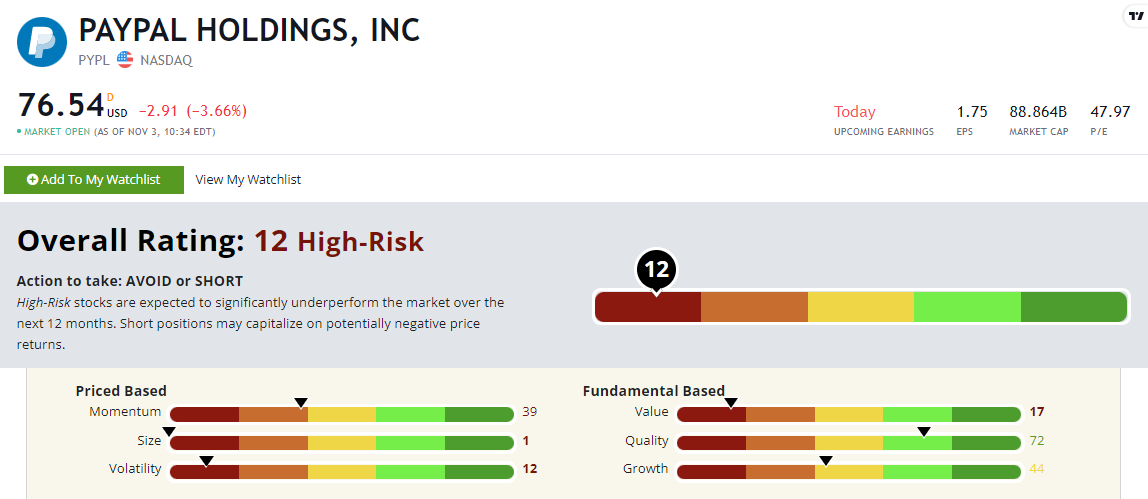

PayPal Holdings Inc. (Nasdaq: PYPL) rates a “High-Risk” 12 out of 100 on our proprietary Stock Power Ratings system.

A recent crackdown on misinformation led to a severe drop in PayPal’s stock.

Let’s get into that before we dive into PYPL’s stock rating.

PayPal’s October Price Drop

The first few weeks of October were tough on PayPal.

On Monday, October 10, PYPL stock dropped 6% because of a failed policy update.

PayPal rolled out a new policy that would fine users up to $2,500 for “sending, positing or publication of any messages, content or material” promoting or spreading misinformation.

The policy saw backlash from many, including PayPal’s former President David Marcus and even consumers, who called for action through the #BoycottPayPal viral hashtag.

The company immediately rolled back its policy and told the media that the update “went out in error that included incorrect information.”

It might have been too little too late for the consumer.

Because the stock still hasn’t fully recovered.

Let’s take a closer look at PayPal’s stock ratings.

Paypal’s Stock Power Ratings & Atrocious Value

Compared to its industry peers, PayPal is overvalued.

I’ll get to value in a second, but first, let’s look at its overall score.

PYPL’s Stock Power Ratings in November 2022.

PayPal rates an overall “High-Risk” 12 out of 100 on our system.

It ranks red on 4 out of our 6 factors. Its volatility (12) and size (1) scores are something to note.

For a massive company with a market cap of $89.8 billion, the stock’s trading pattern has been rocky for shareholders in recent months.

But let’s zoom in on value compared to its industry neighbors.

We can understand PYPL’s value by comparing it to its industry:

- Its price-to-earnings ratio is 44.18, compared to the specialty payments industry average of 13.84.

- The company’s price-to-book ratio comes in at 4.48 … the industry averages 1.69.

- And lastly, its price-to-cash flow ratio was reported to be around 26.34, while the industry average is 8.18.

As you can see, industry averages are much lower than PYPL’s.

That tells us PYPL is overvalued compared to its specialty finance peers.

This earns it a 17 on our value factor.

The Bottom Line

PayPal scores a “High-Risk” 12 out of 100 on our Stock Power Ratings system.

Our system has much more in store for you!

To get one highly rated stock you should consider investing in or some more to avoid — check out Matt Clark’s Stock Power Daily.

Monday through Friday, he gives you one stock to buy or avoid on our system and tells you why.

All for free!