There’s a country with no flag, no capital and no seat at the United Nations. It has no government, no army, and no national airline.

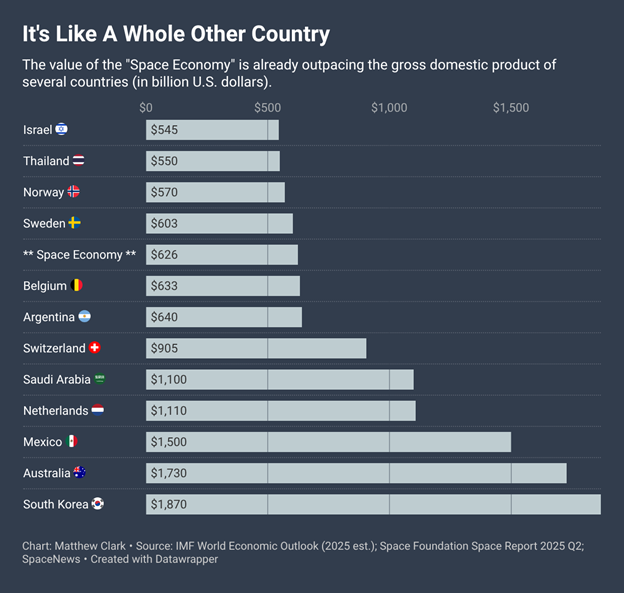

Yet it generates $626 billion in economic output, is growing at roughly 9% a year, and if it were a sovereign nation, it would rank as the 19th-largest economy in the world. That country is the space economy.

And this week, with SpaceX pricing its blockbuster IPO at $135 a share and set to begin trading on Friday under the ticker SPCX, the sector is suddenly back on investors’ radars.

But while the SpaceX IPO may be the loudest story in the room, it’s not the most important one.

You see, the real story isn’t a single company. It’s the emergence of an entirely new economic frontier.

Let’s zoom out.

A G20-Adjacent Economy Nobody’s Talking About

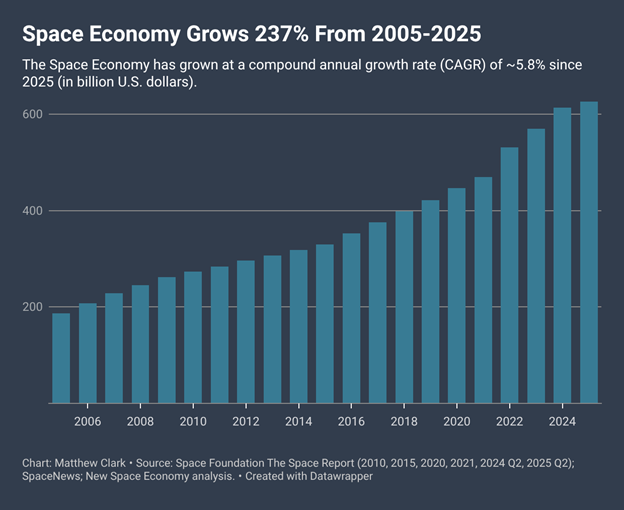

The global space economy hit $626 billion in 2025, according to the Space Foundation’s most recent Space Report.

That puts it comfortably above Israel, Norway and Sweden — all respectable, investable economies with their own index funds and analyst coverage.

Yet most retail portfolios have exactly zero dedicated space exposure, unless you count Boeing (which, given recent years, maybe you shouldn’t).

The number that matters more than the size is the growth rate.

The space economy is expanding at roughly 9% per year — more than three times the pace of the U.S. economy and faster than any G7 country.

At that rate, it will cross $1 trillion by 2032. That’s not a moonshot projection; it’s a straight-line extrapolation of what’s already happening.

What Is the Space Economy, Actually?

Here’s where most coverage goes wrong: it treats “space economy” as a synonym for “rockets.”

It isn’t.

Launch services — the part Elon dominates, the part with the landing boosters and the dramatic livestreams — accounts for a small fraction of total space revenue. The bulk is satellites: communications, GPS, broadband, and increasingly, Earth observation.

Seventy-eight percent of space economy revenue is commercial. And within that sphere, the dominant business model isn’t launching things, it’s what those things do once they’re up there.

Starlink charged $10.4 billion in subscription revenue in 2025. Planet Labs is selling daily satellite imagery to hedge funds, insurers and agricultural companies. Spire Global is beaming weather and maritime data to clients who couldn’t care less about rockets.

This matters enormously for investors.

The launch economy is commoditizing fast — SpaceX has cut the cost per kilogram to orbit by 95% over the last decade, which is great for everyone who wants to put something in space and brutal for everyone who wants to charge a premium to get it there.

The value is moving up the stack, to applications and data. The infrastructure gets cheap; the intelligence on top of it gets expensive.

The Defense Angle Nobody’s Pricing In

Government spending is the other underappreciated part of this story.

Defense now accounts for 54% of all government space budgets globally, and it’s growing faster than civil programs.

Ukraine was a before-and-after moment: satellite comms (Starlink) and satellite imagery (Planet, Maxar) proved decisive in ways that have since been studied, copied and budgeted for by every major military on the planet.

The result is that defense primes with heavy space divisions — Lockheed Martin, Northrop Grumman, L3Harris — now have a revenue floor that most investors are not modeling correctly.

Space accounts for more than 15% of Lockheed’s annual revenue, and Lockheed Martin (LMT) trades at roughly 17X forward earnings, below the S&P 500 Index average, with a $160 billion backlog.

That’s not a sexy pitch. But it’s a real one.

So What Do You Actually Buy?

This is where it gets interesting, and where the SpaceX IPO frenzy creates its own kind of noise.

Everyone is going to chase SPCX this week.

Morningstar already put out a report calling it priced at nearly twice fair value. That may or may not be right. But it does raise a more useful question: if you believe in the space economy thesis, is the rocket company the right way to play it?

History suggests otherwise.

When bandwidth got cheap in the late 1990s, the ISPs didn’t win — Alphabet (GOOGL), Amazon (AMZN) and Netflix (NFLX) did. Cheap launch is the new cheap bandwidth.

The companies building on top of the infrastructure — the data services, the analytics, the direct-to-device connectivity players — may be where the durable value accrues.

Three ways to get exposure that aren’t just buying SPCX at a 94X sales multiple:

- ETFs for broad exposure: The Tema Space Innovators ETF (NASA) and the ARK Space Exploration ETF (ARKX) offer diversified exposure without single-stock risk. Not glamorous, but effective.

- Pure-play data: Planet Labs (PL) and Spire Global (SPIR) both operate under a data-as-a-service model. Spire is up 145% year to date and projects 50% revenue growth. Planet is the quietest $600M ARR business in tech.

- Defense primes with space divisions: LMT and Northrop Grumman (NOC) are boring in the best possible way — cheap multiples, massive backlogs and a government anchor customer that just decided space is a strategic priority.

And that’s just the tip of the iceberg.

SpaceX goes public this week, and the financial media will cover little else.

That’s fine. It’s a historic moment. But history is full of investors who bought the famous name at the peak and missed the quieter companies that built the real wealth.

The space economy is $626 billion and growing.

It doesn’t have a capital city, but it does have a ticker symbol. Several, actually.

The question is which ones you own before everyone else starts paying attention.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets

P.S. Intel helped power the PC revolution. Cisco helped build the internet. In both cases, some of the biggest winners weren’t the household names everyone talked about, but the critical suppliers working behind the scenes.

And What My System Says Today editor Adam O’Dell believes the SpaceX era could create a similar opportunity today — and he’s identified the company he thinks is best positioned to benefit.

So, on Thursday, June 11, he’s going LIVE to reveal the little-known company sitting at the center of this story — and why Wall Street is still missing it.