Bonds are considered less risky than stocks.

This means, for example, that bonds issued by a bankrupt company like Hertz are less risky than the stock of the company.

In the case of Hertz, bondholders expect to get paid about $0.33 on the dollar after bankruptcy.

Shares of the company, on the other hand, will likely be worthless.

While the bonds are safer, investors still face a large loss. Since bonds are often owned by pension funds, losses of almost 70% threaten benefits.

To avoid large losses, bondholders created insurance markets for bonds. They can buy derivatives known as credit default swaps (CDS) that allow them to shift the risk of a large loss to a hedge fund or other aggressive investor.

As insurance, CDS markets serve an important purpose. But traders can get carried away. The mortgage CDS market was the center of the financial crisis in 2008.

Regulators have taken steps to ensure CDS are used responsibly. Now these markets are less speculative, and CDS traders shouldn’t trigger another financial crisis.

That means these markets are arguably more informative. Prices accurately reflect the risk of default rather than the risk a leveraged hedge fund will go bankrupt.

Are Bonds Signaling the Dollar’s Doom?

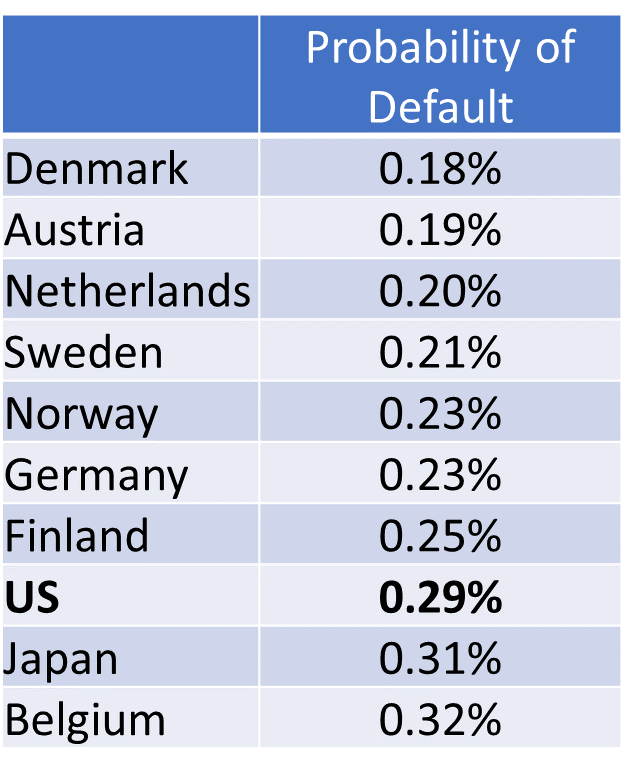

In sovereign debt markets, based on the price of the CDS, we can calculate the probability of default for any individual country. The chart below shows that traders believe seven countries are safer than the United States.

Source: WorldGovernmentBonds.com

And this has important long-term implications for the U.S. dollar.

Investors are equally, if not more, comfortable with debt issued in Danish krone, Swedish krona or euros. So the dollar could one day lose its role in international finance. A basket of currencies, or even the euro, could easily replace the dollar.

Watch this trend. If more countries show lower default risk than the U.S., the dollar will lose its special place in the global economy.

In the long run, the dollar appears to be doomed.

• Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at New York Institute of Finance. Mr. Carr also is the former editor of the CMT Association newsletter Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.