Before I moved to sunny South Florida, I lived in Greenville, South Carolina, for about five years.

Driving through downtown or along the Interstate 85 corridor, there was never a shortage of cranes and construction vehicles working on a new office building, mixed-use building or apartment complex.

Nestled between Charlotte and Atlanta, the progress of construction contrasted with lovely Paris Mountain in the background was a sight to behold.

Take a look at downtown Greenville:

Downtown Greenville keeps growing.

It’s the home to BMW Manufacturing Co. — the German carmaker’s U.S. manufacturing facility — and the North American headquarters for French tire manufacturer Michelin.

Greenville is also home to hundreds of supply chain companies working with BMW.

Employees of those companies need housing — and there’s a constant need for new commercial construction for offices and manufacturing.

I found a trend that illustrates that Greenville, and plenty of cities like it, will keep growing … and need even more new construction.

Using Chief Investment Strategist Adam O’Dell’s six-factor Green Zone Ratings system, I found a construction stock that will capitalize on this trend and beat the market 3X over the next 12 months.

First, you need to understand the trend.

A New Construction Boom on the Horizon

From 2011 to 2015, the value of new construction in the U.S. ballooned from $788.3 billion to $1.1 trillion — a 41% increase in just four years.

But over the last three years (from 2018 to 2020), new construction value has tapered off.

I don’t think that will last.

The FMI Corporation — a construction and engineering research firm — suggested that the value of new construction in the U.S. could reach more than $1.4 trillion by 2023.

That’s an 83% increase from 2011.

U.S. New Construction to Jump 83% by 2023

Using Adam’s six-factor Green Zone Ratings system, I’ve found a construction stock play that can outperform the rest of the market by 3X in the next 12 months.

Construction Stocks: More Than Hammer and Nails

Construction is more than just a hammer, nails and big-equipment.

You often need power, fire alarms and internet infrastructure in place.

This is where IES Holdings Inc. (Nasdaq: IESC) enters the fold.

The Houston-based company provides electrical and mechanical design as well as construction services for corporate, educational, residential construction and much more.

It’s been in business since 1997 and has locations all over the United States … including Greenville.

In 2019, the company had one of its best years with sales of more than $1.1 billion — an increase of 22% from 2018.

IESC’s construction stock has a five-year annual sales growth rate of 16%, and its trailing 12-month sales total $1.15 billion.

IESC Shares Skyrocket 158% Since March

In addition to its massive climb since March, IESC shares have grown more than 76% in the last 12 months — compared to just 6% average growth for other stocks in the facilities and construction services industry.

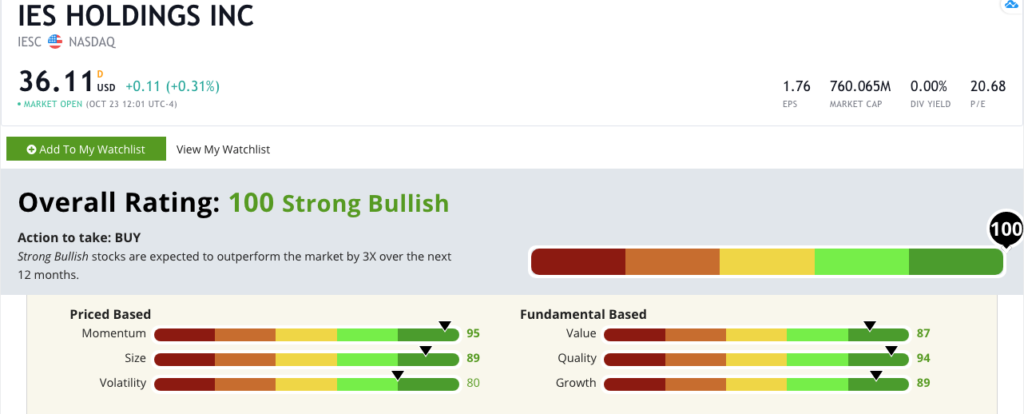

IESC Is in the Green Zone

We can look at Adam’s six-factor Green Zone Ratings system to see that IESC ranks high in all six factors — momentum, size, volatility, value, quality and growth.

Its overall ranking is 100 out of 100 … meaning we are “strong bullish” on the construction stock.

IESC Holdings’ Green Zone Rating on October 26, 2020.

Here’s a deeper dive into the company’s rankings:

- Momentum: The company scores a 95 on Momentum. Adam is a strong believer in the Momentum Principle (buy high … sell higher.) To read his recent article on momentum investing, click here.

- Size: With a market cap of just $760 million, IESC ranks an 89 on Size.

- Volatility: IESC is less prone to wild market moves, earning it a rank of 80 on Volatility.

- Value: IESC earns an 87 on Value. The company’s price-to ratios (sales, cash flow and book) are either below or in line with the rest of the construction industry.

- Quality: The company is a high-quality stock, rating a 94. High-quality stocks tend to outperform low-quality ones.

- Growth: IESC shows a ton of promise to grow even more. It has strong earnings per share ($1.76), and its net income continues to grow. The company earns an 89 on Growth.

What You Should Do With the IESC Construction Stock

With an overall rating of 100, IESC is a company we are “strong bullish” on.

We see this construction stock outperforming the overall market by 3X over the next 12 months.

The bottom line: The construction industry will grow even more in the next three years.

IESC will benefit from that growth — and it provides a valuable service beyond just construction.

Its shares are testing new highs, making now the perfect opportunity to get in and realize those large gains.

That’s all I have for this week’s Green Zone stock.

Until next time…

Safe trading,

Matt Clark

Research Analyst, Money & Markets

Matt Clark is the research analyst for Money & Markets. He’s the host of our podcast, The Bull & The Bear, as well as the Marijuana Market Update. Before joining the team, he spent 25 years as an investigative journalist and editor — covering everything from politics to business.