We’ve all seen photos like the one below: a Chinese downtown covered in smog.

Thick smog covers a city in China. But the country is doing something to combat the dismal haze.

Because of carbon emissions, a normally picturesque scene looks horrible.

From cars to businesses and residents, China has had to deal with a significant smog problem.

But the nation is taking steps to right the ship.

It’s looking to solar power to help cut down on emissions.

And that leads to a great investment opportunity for investors like us.

Using Money & Markets Chief Investment Strategist Adam O’Dell’s proprietary stock rating system, we found a company set to make itself … and investors … a lot of money because of China’s growth in solar. Best of all, it trades on U.S. exchanges.

I’ll tell you about that in a bit. But first, we should understand where the Chinese solar market is going and why it’s important — even to American investors.

The Chinese Market Leads in Solar

While solar companies in the U.S. are starting to make headway, growth in China is massive.

According to the National Renewable Energy Laboratory (NREL), the U.S. deployed 13 gigawatts of direct current solar power in 2019. In China, that number was more than double, at 30 gigawatts.

That Chinese expansion is moving rapidly.

Chinese Solar Power Demand to Skyrocket

That’s a 3,300% increase in solar demand in China from 2017 to 2050!

And one solar company will benefit from that huge growth … as will its investors.

This Chinese Company Is Poised for a Solar Boom

We used Adam’s proprietary stock rating system to find a great alternative-energy company with the potential to take off in a hurry.

Daqo New Energy Corp. (NYSE: DQ) manufactures and sells polysilicon to photovoltaic product manufacturers in China.

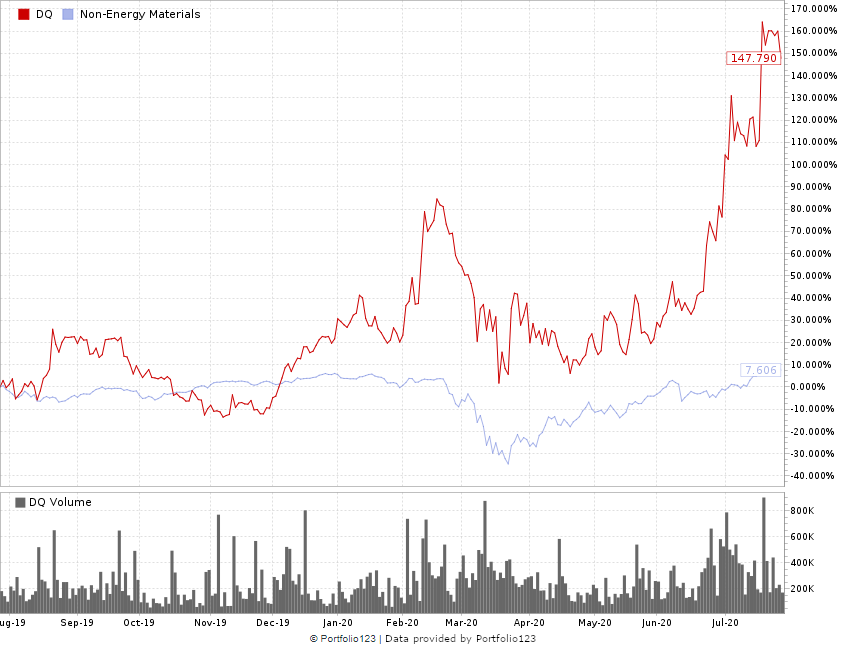

Daqo Beating its Sector Peers

These polysilicon crystals are used in solar panels you see on top of people’s houses.

Daqo produces the elements that are used to make solar panels, like these, that go on top of houses.

The benefit of using the product Daqo makes is that it’s considerably cheaper than the competition’s, making it a top-choice supplier

What’s more, overall growth in the solar industry is accelerating thanks to the rapid rate at which the technology’s cost is declining.

In 2014, the price of a kilogram of polysilicon was $22. Now, it’s about $7.17. That makes it much less expensive for companies to use Daqo’s products.

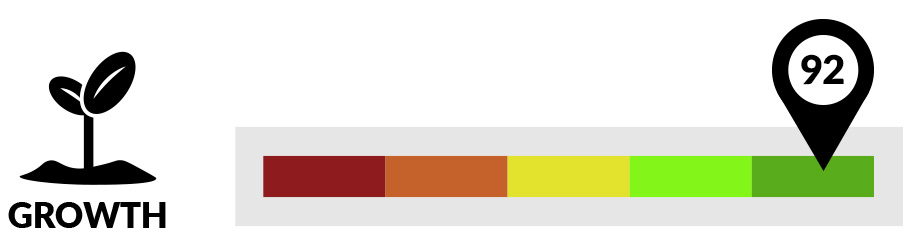

The company rates a 93 out of 100 overall, with its strongest single-factor ratings on growth, value and quality.

Here’s what we found about Daqo:

- Growth — DQ rated a 92 on growth — meaning only 8% of all stocks rated higher. That is led by a 98 rating in sales. (Its annual sales growth was an impressive 50%!) Daqo also rated better than 90% of all other stocks on net income.

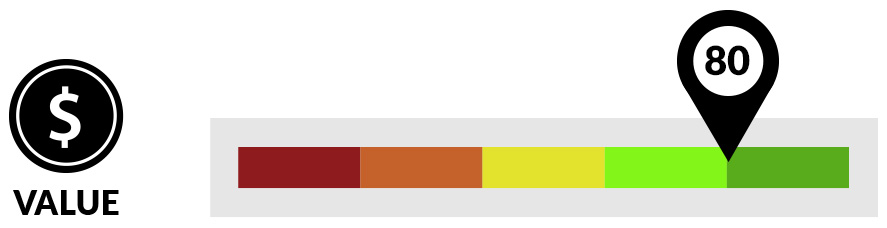

- Value — Daqo proves a company’s stock can be high-growth and high-value. It rated an 80 on value — only 20% of all other stocks were higher. That rating is anchored by its price-to-earnings ratio (rated 77 out of 100) and its price-to-cash flow ratio (75 out of 100).

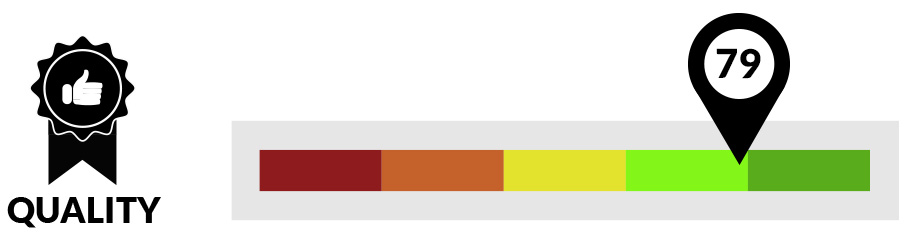

- Quality — The company rated a 79 overall on quality — meaning it’s better than 79% of all other stocks. That’s in large part due to its return on assets, equity and investment (rated better than 92% of all other stocks). Its profit margins rated better than 87% of all other stocks.

Here’s What You Should Do

The solar industry is starting to make inroads in the U.S., but it’s really taking off in China.

As the country pares back its reliance on fossil fuels and attempts to reduce its smog, China will lean into solar energy.

Because Daqo provides a necessary component to produce solar panels cheaply and scaled, the company will be the go-to to help meet demand.

It’s a growing company with strong value and solid quality.

Toss in the growth of the industry, and Daqo is the right play for investors to realize massive profits in the coming years.