Every earnings season has one number that looks almost too good to be true. This quarter, it’s coming from the energy sector.

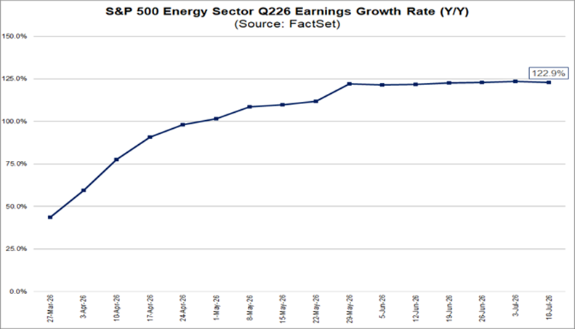

Analysts expect energy companies to post 122.9% year-over-year (YOY) earnings growth in second-quarter 2026 — by far the fattest growth rate of any of the S&P 500 Index’s 11 sectors.

What caught my attention wasn’t just the size of the estimate. It was how we got here.

Back on March 31, Wall Street was expecting earnings growth in the neighborhood of 48%.

Then the estimate kept climbing… week after week… until it more than doubled.

That’s the opposite of what usually happens.

Analysts typically spend most of a quarter quietly trimming their forecasts. This time, they were scrambling to raise them.

The reason is simple: oil.

WTI crude averaged $92.55 in the second quarter, about 45% above the $63.68 from a year earlier.

When you’re an oil-weighted producer, that kind of YOY swing drops almost straight to the bottom line. Refiners, with expected earnings growth of 231%, and the integrated majors, at 160%, are doing much of the heavy lifting. So far, everything looks incredibly bullish. Here’s where my system starts flashing yellow.

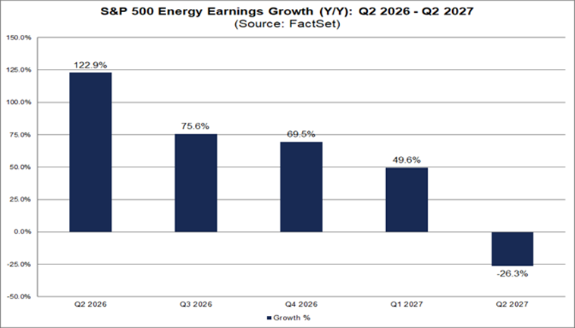

That triple-digit growth rate is in the rearview mirror. It’s built on a price that no longer exists, as crude has already dropped to around $70 a barrel.

And once you look beyond this quarter, the story changes quickly.

Consensus estimates call for earnings growth of 122.9% this quarter, then 75.6%, then 69.5%, then 49.6%. By second-quarter 2027, it turns outright negative at -26.3%.

Easy comparisons eventually become hard ones, and the same base effect that supercharged earnings growth this quarter begins working against the sector next year.

That is the whole tension I’m thinking about as earnings season begins.

The headline says energy is the market’s hottest earnings story. The forward estimates suggest it’s also a story that’s already beginning to cool. Peak earnings growth and peak investor enthusiasm often arrive at roughly the same moment.

So as we work through next week’s earnings calendar, that’s the lens I’ll be using: separating the companies riding the wave from the ones building something that survives the tide going out.

Now, let’s get into the bullish and bearish calls.

“Bullish” Earnings to Watch

These stocks are expected to beat their earnings per share (EPS) from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are 10 companies that made this week’s list:

Ten names on next week’s calendar cleared my bar for bullish earnings potential, but three are especially worth your attention.

The two loudest are turnaround stories.

Dow Inc. (DOW) is projected to swing from a $0.74 loss last quarter to a $1.26 profit, and Intel Corp. (INTC) does the same thing in miniature — from a $0.73 loss to a $0.21 gain.

Those aren’t beats; they’re direction changes, and direction changes are when the market re-rates a stock rather than just nudging it.

However, going from red to barely black is the easy part of any comeback. What I’ll actually be listening for is what management says about the next quarter, not this one.

The third is International Business Machines Corp. (IBM), and it’s the cleanest of the bunch — $2.91 estimated against $1.28 last quarter, more than a double, with no loss-to-profit asterisk attached.

Here’s how I’d look at all three, though.

A big projected jump is a promise, not a receipt.

Next week is about which of these companies actually cash it — and, just as important, which ones sound like they can do it again.

That’s the difference between a stock that pops on Thursday and one you can still own in the fall.

Now, let’s look at the potentially “bearish” earnings calls for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are 10 companies that passed this screen:

EQT Corp. (EQT) ties back to where we started. It’s the largest natural gas producer in the country, and it’s staring at $0.42, down from $2.36 last quarter.

Remember the note from the open — oil had a great quarter, but Henry Hub sat around $3.20, squeezing the gas-weighted names all the way through it. This is what that squeeze looks like when it reaches the earnings line.

Nothing is broken about the company; it’s just standing on the wrong commodity.

Alphabet Inc. (GOOGL) is the marquee name, and the drop is real — $2.87 estimated compared with $5.11 last quarter.

On a business this size, a swing that size is worth reading carefully rather than reacting to. The question next week isn’t whether the number is down; it’s why heavier capital spending on AI infrastructure can dent near-term EPS even as the underlying business is perfectly healthy.

Falling earnings and a failing business are not the same thing, and this is exactly the name where that distinction matters.

GE Vernova Inc. (GEV) is the eye-popper — $3.19 estimated against $17.44 last quarter — but a drop that violent almost always means last quarter carried something lumpy and one-time.

I’d read this one as a reset to a normal run rate rather than a collapse.

Remember, that is the whole point of the bearish list. The job next week isn’t to flinch at a smaller number, it’s to figure out which shrinking earnings are a warning and which are just weather.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, What My System Says Today