With this week’s coronavirus-driven rout having shaken awake previously slumbering euro-dollar markets, the spotlight is back on the “short volatility” trades that some regulators fear could trigger a blowup on world markets.

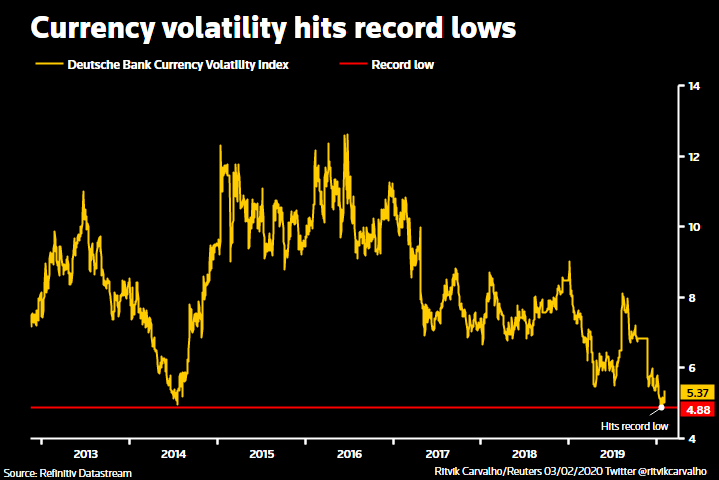

The world’s most traded currency pair, comprising a quarter of global forex volumes, has become increasingly becalmed in recent years, and volatility gauges embedded in euro-dollar options tumbled in January to historic sub-4% lows from 7.3% a year earlier.

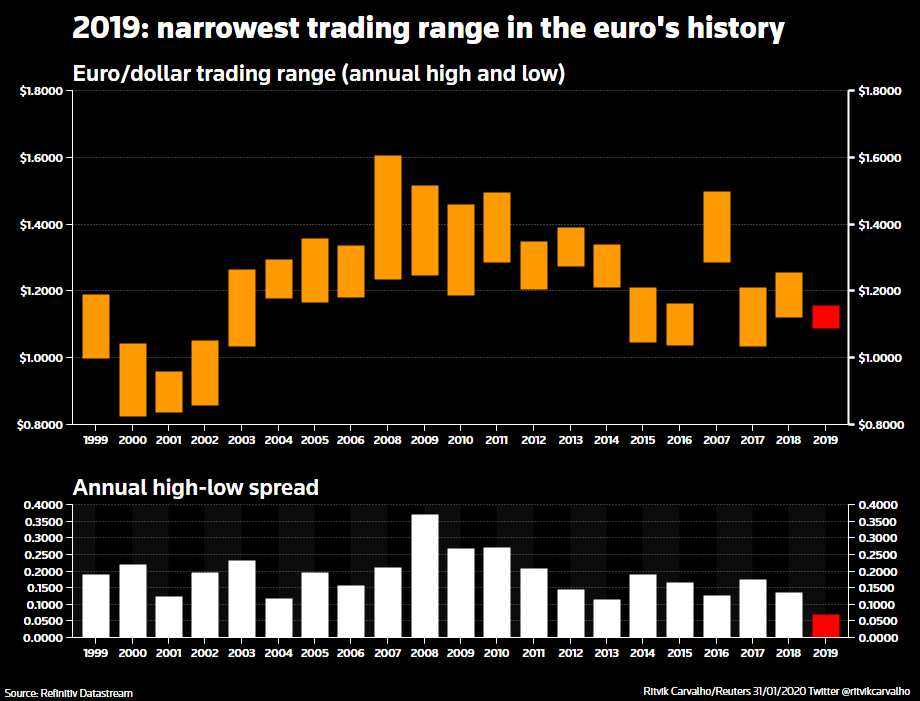

The pair’s trading range last year — $1.15 to $1.09 — was the narrowest in the euro’s two-decade history, to the displeasure of currency traders who can wring out more profits in volatile markets, often by selling hedging products to clients.

Their mood may have been improved by a rise in euro-dollar implied volatility to back above 6%, the highest in nearly six months.

Currency volatility hits record lows.

But there’s some trepidation too as memories stir of the ‘Volmageddon’ crisis of February 2018 when the short equity volatility trade imploded, sending investors scrambling to recoup losses and triggering a huge Wall Street selloff.

With regard to positioning linked to currency markets, any sharp rise in volatility would hit those who have shorted vol by selling options, as well as those who bought more risky assets, betting exchange rate swings would decline or stay stable.

“It makes us more nervous because it is indicative of a build-up of positioning,” said a central bank official who spoke to Reuters on condition of anonymity, referring to investors buying risky financial assets.

RIPPLE EFFECT?

The worry is that the extended low-vol backdrop ups the risk of a blowout that ripples across all the sectors that benefited from FX calm.

The official said no plan of action was in place, but that central banks were monitoring the potential implications of a vol spike, adding: “When these things unwind, they do so in a sharp manner – up the stairs and down the elevator.”

The issue is clearly on regulators’ minds.

One senior FX trader who sits on a major central bank’s foreign exchange committee said it was the number one topic at a recent meeting of industry and policy executives.

The Bank of England and European Central Bank declined comment. The New York Federal Reserve did not return calls and emails seeking comment.

So opaque is the currency trading world that no concrete data exists on positioning, but the dealer said “a lot of people” were short volatility, with the consensus view that low vol was here to stay thanks to low interest rates worldwide.

“We want volatility to increase but what we don’t want is a shock. I don’t think anyone wants a shock,” the person added.

Narrowest trading range in the euro’s history.

Measures of currency activity have been falling since the 2008 financial crisis, as central bank liquidity taps have gushed, inflation fallen and policies moved more or less in lockstep.

To a layman, extended currency calm may sound like a good idea. But it can tempt market makers, including hedge funds, to lever up and buy riskier, less liquid securities, a trend noted in the International Monetary Fund’s financial stability report.

The issue also highlights how loosely regulated the $6.6 trillion-a-day forex market is. Unlike in equity markets, there are few ways to accurately measure positioning whether in spot currency markets or derivatives.

“We don’t know, in the context of a global recession and associated market selloff, how resilient the fund industry will be,” Tobias Adrian, director of the IMF’s monetary and capital markets department, told Reuters, warning of a “potentially destabilizing” situation.

“Our policy advisory is that regulators should monitor potential risk and that they should take actions preemptively in order to protect financial stability,” he added.

The Bank of International Settlements too, writing just after Volmageddon, likened short vol strategies to “collecting pennies in front of a steamroller”.

YEN ROUT A FORETASTE

The rush into short-vol is partly because traders, deprived of money-making opportunities, turned to selling currency options which earned them a small premium.

Such trades can yield handsome profits – for instance, shorting euro to buy equal weights of the dollar, rouble and Brazilian real would have made 11.5% in 2018/2019, Refinitiv data shows.

Essentially a short bet on euro volatility, that trade would have generated a Sharpe ratio of 2.5, versus 1.7 in 2015-2016 when vol was in the double-digits. Sharpe ratio refers to returns earned above risk-free rates after adjusting for volatility.

But if the picture turns, the impact can be gigantic.

The 2018 Volmageddon was blamed on punters betting on lower equity volatility through short positions in VIX futures, akin to buying options aimed at shorting FX vol.

Mizuho analysts reckon the 1.3% yen rout on Feb 19 this year may have stemmed from investors buying back some short dollar positions as volatility grew higher.

Traders are still relatively relaxed about the risk of a near-term volatility surge, however, especially given past such warnings have fallen flat. Relatively stable economic growth and stagnant inflation metrics mean low volatility is normal, the IMF’s Adrian argued.

And finally, those who favor selling vol are confident central banks will step in to smooth out any market turmoil, with markets already betting the Fed and other central banks will cut interest rates in response to the coronavirus.

© Copyright Thomson Reuters 2020.