Nearly seven million U.S. households have investable assets exceeding $1 million, and about 29 percent of Americans think they’ll be a millionaire by retirement time according to GoBankingRates.com.

USA Today content partner The Motley Fool broke down how to achieve your financial retirement goals in a recent article.

Per USA Today, the first step is obvious — start saving today.

Start Saving for Retirement as Early as Possible

When it comes to building wealth, compounding will be a major weapon in your arsenal — so take advantage of it early on. Compounding, in its simplest form, means earning interest on top of interest, and it’s what allows savers to turn smaller amounts of money into larger sums over time.

The following table illustrates how compounding can work to your advantage:

Essentially, saving about $500 per month over a 40-year period equates to $240,000 out of pocket. You will wind up with five times that amount after applying a 7 percent average annual return.

How do we get there? By investing our gains year after year and continuing to save at a consistent rate. But, as stated above, the longer your compounding window, the more wealth you stand to accumulate. Case in point: Cutting your savings window by only five years shrinks your gains from about $960,000 down to $619,000 — still impressive but nowhere close to the former.

Invest Wisely

Obviously, the higher your returns on investment, the more wealth you’ll accumulate. But if you’re looking to grow your growth in the best manner possible, you’ll have to be somewhat aggressive in your investments.

This means putting a sizable chunk of your assets into stocks, which have historically delivered much higher returns than bonds.

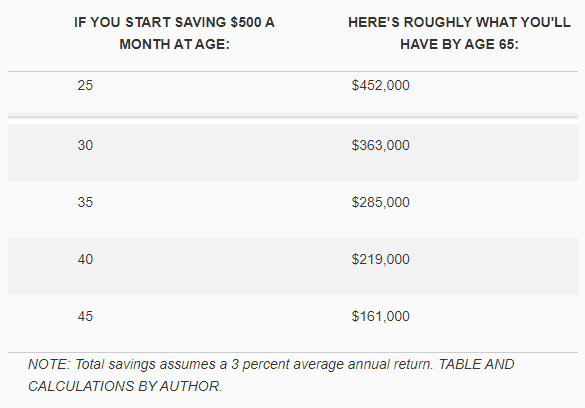

In the example above, we applied a 7 percent average yearly return to our investments. Well, that’s the sort of return you can expect with a stock-heavy portfolio. In fact, that 7 percent is actually a couple of percentage points below the stock market’s historical average. On the other hand, if you were to go heavy on bonds, you’d probably wind up with something closer to a 3 percent average annual return. And here’s what the above table would look like as a result:

Essentially, passing up aggressive returns means missing out on a lot of money, so you can’t play it too safe.

Essentially, passing up aggressive returns means missing out on a lot of money, so you can’t play it too safe.

Make Smart Spending Choices

Another fairly obvious tip is to make wise choices when spending because you can’t invest if you don’t have cash.

In both examples above, our calculations work with a $500 monthly savings target, but if you spend down each paycheck you receive, you won’t get anywhere close. On the other hand, if you make a point of living well below your means, you’ll have an easier time setting money aside on a regular basis.

The best thing you can do is create a budget to see where your money is being spent. Having a budget will help you pinpoint wasteful spending and places you can cut back. Even if you’re an average earner, you can make it to a million dollars by retirement if you prepare properly, save your money, invest it wisely and make smart spending choices.